- BF rebar trade prices fall by INR 600/t w-o-w

- HRC market weakens on dull trade sentiment

- Market slows down amid monsoon disruptions, festive holidays

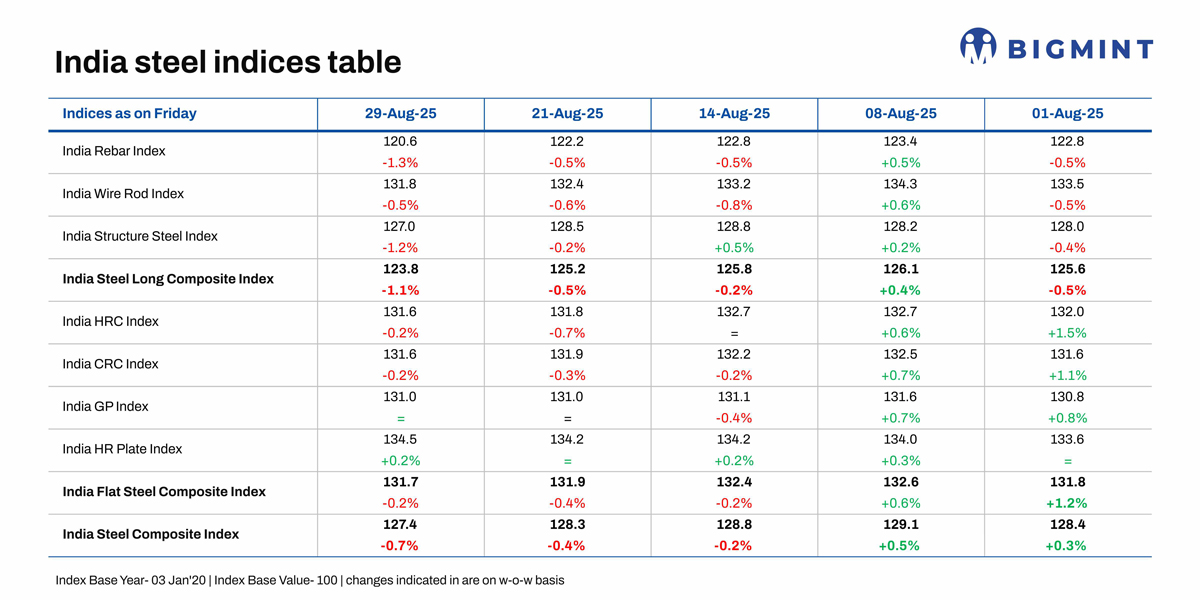

Morning Brief: BigMint’s India steel composite index, which mirrors price movements in the domestic market, continued to dip w-o-w in late-August 2025 reaching close to five-year lows. The index, assessed at 127.4 points, reached the lowest point since early December 2020 during the pandemic – a 56-month low.

The composite index fell 0.7% w-o-w on 29 August as market conditions weakened amid heavy monsoon downpour in different regions of the country and logistics disruptions weighing on trade sentiment. While the flats index edged down by 0.2% w-o-w, remaining largely stable amid strengthening Chinese and Asian steel prices, the longs sub-index fell sharply by 1.1% w-o-w.

Highlights of price movements

BF rebar prices soften: Trade-level BF rebar prices decreased by INR 600/tonne (t) ($7/t) w-o-w to INR 47,300/t ($538/t) exy-Mumbai, as per BigMint’s assessment on 29 August. Prices are exclusive of GST at 18%. The reason, of course, was weak demand.

In the projects segment, prices dropped to INR 46,000-47,000/t ($523-535/t) FOR Mumbai. Market activity was muted, as buyers stayed cautious during the monsoon season and the Ganesh Chaturthi festive week. Construction momentum dampened due to logistical challenges, leading to project delays and subdued procurement.

IF rebar trade prices decline w-o-w: IF rebar prices dropped by INR 900/t ($10/t) w-o-w to INR 44,800/t ($510/t) exw-Mumbai on 29 August. Prices declined w-o-w across key Indian markets amid subdued trading activities. Manufacturers reduced their list prices and offered discounts to liquidate material. There was no major buying interest during the week, with inventory assessed at more than 12 days across regions.

HRC market weakens on dull trade sentiment: BigMint’s benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) fell by INR 300/t ($3/t) w-o-w to INR 49,700/t ($567/t) on 26 August against INR 50,000/t ($570/t) on 19 August. On the other hand, CRC (IS513, Gr O, 0.9 mm/CTL) prices held stable w-o-w at INR 57,000/t ($650/t), as assessed on 26 August. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Monsoon and festive holidays impacted trade activity, with prices remaining rangebound in the trade segment. Market participants also cited labour shortages across key regions as further weighing on sentiments and delaying restocking decisions.

A source said, “Ample stock availability in the trade market, supported by sufficient inventory levels, has reduced the urgency to buy fresh material which has kept demand subdued.”

Outlook

Market participants are waiting for mills’ price announcements for September, which are likely this week. Buyers are cautious in making purchases amid weak market sentiments. The impact of steep US tariffs on the different sectors of the economy and India’s export prospects remain in serious doubt. This has obviously impacted market sentiments.

Trade activity is expected to remain sluggish until the end of monsoon. Moreover, sufficient inventory levels in the trade market, coupled with muted restocking appetite, will keep demand restrained in the short term. However, steelmaking raw materials prices have been firm for quite a while, especially domestic iron ore prices. This is expected to stop steel prices from falling further.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply