- Global coal exports rise to 18.63 mnt, highest in 4 weeks

- US shipments nearly double, SA rebounds strongly

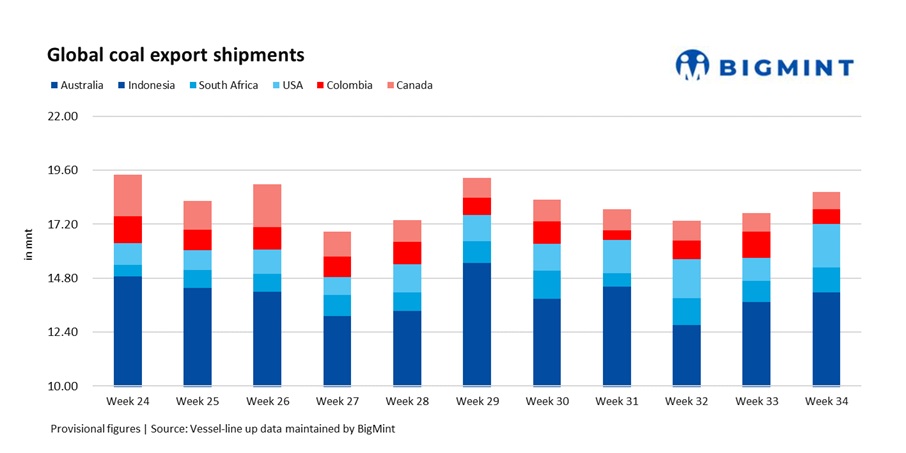

Global seaborne coal exports climbed 5.2% w-o-w to 18.63 million tonnes (mnt) in Week 34 (16-22 Aug), compared with 17.71 mnt in Week 33 (9-15 Aug), according to BigMint’s vessel line-up data.

The rise was largely supported by a rebound in seaborne activity after a subdued first half of August 2025. Stronger shipments from the USA and Australia, aided by smoother port clearances and consistent demand from Asian and European buyers, played a key role in driving the increase.

This helped offset declines from Indonesia, Canada, and Colombia, where weather disruptions, softer demand, and logistical hurdles weighed on shipments. Overall, Week 34 reflected a more balanced supply outlook, though regional differences in demand and freight conditions continued to influence export flows.

Country-wise trends

Indonesia: Exports from Indonesia slipped marginally by 2.6% w-o-w to 7.12 mnt in week 34, as compared to 7.31 mnt in the week before.

On the demand side, buying interest from China (1.65 mnt) and India (1.22 mnt) followed by Philippines (0.77 mnt) & South Korea (0.62 mnt) remained steady. Market participants noted that vessel delays at key coal terminals, combined with cautious buying from Indian utilities amid high stockpiles, contributed to the softer numbers.

Although volumes remain relatively strong compared to earlier in the quarter, the current weakness underlines the seasonal slowdown that often characterises Indonesian shipments during the peak monsoon period.

Australia: Australian coal exports rose sharply by nearly 10% w-o-w to 7.05 mnt. The recovery was led by higher shipments from Newcastle (2.96 mnt) and (Gladstone 1.50 mnt), followed by DBCT (1.20 mnt) reversing the weather-related disruptions that had slowed down loading activity in the previous weeks.

Buyers across Japan (2.08 mnt), China (0.93 mnt and South Korea 0.61 mnt, showed steady interest in both thermal and metallurgical coal, helping sustain flows despite cautious sentiment in the global freight market. Sources noted that Australian exporters benefited from improved vessel availability, which eased congestion at load ports.

USA: The U.S. recorded the sharpest w-o-w increase of around 86% in Week 34, with coal exports nearly doubling to 1.93 mnt. The rise was largely driven by stronger loadings at East Coast terminals, led by Norfolk (0.73 mnt), while Baltimore and Mobile each contributed 0.48 mnt.

On the demand side, India emerged as the largest buyer at 0.66 mnt, followed by the Netherlands (0.23 mnt) and Brazil (0.22 mnt). Market sources noted that firmer transatlantic flows, coupled with easing logistical bottlenecks, enabled more vessels to sail during the week.

South Africa: South African exports picked up by 17.2% w-o-w to 1.10 mnt, supported by gradual improvements in railings to Richards Bay Coal Terminal (RBCT).

Loadings at RBCT reached 1.10 mnt, with India emerging as the largest buyer at 0.59 mnt, followed by the Netherlands at 0.16 mnt. While overall volumes remain subdued compared to earlier this year, steady offtake from Indian sponge iron producers and European utilities provided some cushion to demand.

However, sources indicated that sustained growth would require consistent rail performance, as bottlenecks in the past have frequently capped South Africa’s export potential.

Canada: Canadian coal exports fell by 7.4% w-o-w to 0.77 mnt in Week 34, weighed down by weather-related disruptions and a limited vessel line-up at the Port of Vancouver. Loadings were distributed across key terminals, with Vancouver handling 0.32 mnt, Roberts Bank 0.31 mnt, and Prince Rupert 0.13 mnt.

On the demand side, China emerged as the main buyer at 0.37 mnt, followed by South Korea at 0.26 mnt and Japan at 0.14 mnt. However, overall appetite from Northeast Asia remained soft, as buyers continued to favor Australian cargoes for their shorter voyage times and relatively stable freight rates.

Looking ahead, Canadian coal exports are expected to remain range-bound in the near term, as ongoing port congestion and subdued seaborne demand continue to limit any meaningful upside.

Colombia: Exports from Colombia fell steeply by 43.6% w-o-w to 0.66 mnt, reversing the strong performance seen in the previous week.

On the supply side, shipments from Puerto Nuevo fell significantly to 0.60 mnt, highlighting reduced terminal activity. In addition, intermittent logistical constraints at Colombian terminals further weighed on exports.

Freight trends: Dry bulk coal freights to India held largely steady w-o-w across key routes from Australia, South Africa, and Indonesia, despite muted fixture activity.

Limited cargo volumes, weak Asian buying appetite, and persistent port disruptions kept vessel demand subdued. A wide bid-offer spread, with both shipowners and charterers sticking to firm positions, further hindered trade activity.

Outlook

In the near term, global coal exports are expected to remain range-bound, with South Africa sustaining improved flows, while Australia and Indonesia may face headwinds from weather delays and muted buying interest. Freight levels are likely to stay steady to softer, as vessel oversupply and sluggish trade activity weigh on market sentiment.

Leave a Reply