- Traders cautious as portside activity remains subdued

- South African coal import offers still high

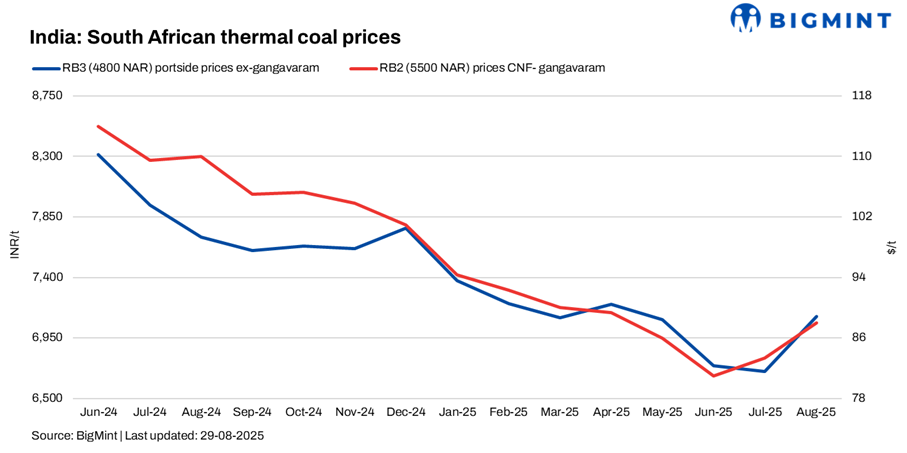

South African RB2 and RB3 thermal coal prices at Gangavaram held stable w-o-w at INR 8,300/t and INR 7,200/t, respectively. At some eastern ports, offers eased by INR 100-200/t as sellers lowered quotes in response to weak demand. However, lower inventories and higher import prices kept the market stable.

Around 12,000 t RB2 deal was heard at INR 8,000/t ex-Paradip, while another 7,000 t of RB2 traded ex-Krishnapatnam at INR 8,325/t. Uncertain offers and low inventory levels with Indian trading houses kept overall activity muted.

Portside inventories fall w-o-w

India’s portside thermal coal inventories fell marginally by 0.6% w-o-w to 13.78 mnt in Week 34, compared with 13.86 mnt in Week 33.

Sponge iron market weakens further

BigMint’s C-DRI index (ex-Rourkela) slipped INR 300/t w-o-w to INR 25,600/t. Raipur, Bellary, and Jharsuguda saw a decline of INR 50-100/t, while Ramgarh recorded a rise of INR 100/t. Buyer participation was limited, with most purchases confined to immediate needs.

Export offers remain mixed

South African RB2 export offers stayed stable w-o-w at $74/t FOB, while RB3 edged down $1/t to $61/t, reflecting muted Indian buying despite steady overseas sentiment. As per the traders in India, they are getting delivered existing shipment, new bookings are very limited as offers are still high.

Domestic coal prices rise w-o-w

Domestic coal prices moved higher this week, supported by lower inventories. BigMint assessed 5,000 GCV at INR 5,700/t ex-Bilaspur, up INR 450 w-o-w, while 4,500 GCV climbed INR 300 to INR 4,800/t. Prices gained momentum as tight stock levels kept supply constrained. Recent SECL auctions also recorded higher bids, reflecting firm buying interest despite limited participation from sponge sector players.

Outlook

South African coal offers may remain volatile in the near term, with limited trade and cautious buying.

Leave a Reply