- Manufacturing growth rate at 2-year low, PMI remains in the red

- Crude steel output drops over 3% in Jan-Jul’25, exports up 11%

- Economic recovery hinges on amicable trade resolutions with US

Morning Brief: China’s economy exhibited signs of slowdown in July 2025 as factory output and retail sales slowed and housing prices dropped further, according to data released by the National Bureau of Statistics (NBS). Uncertainty over tariffs on exports to the US is still looming over the world’s second-largest economy. The US has extended a pause on a hike in import duties following a 90-day pause that began in May.

Annual growth in industrial output slowed to 5.7% in July from 6.8% in June, according to NBS, an eight-month low. Investments in factory equipment and other fixed assets increased a meagre 1.6% in January-July. Exports were a bright spot but economists believe that slowing of industrial growth shows that the positive effect of higher exports may already be tapering off.

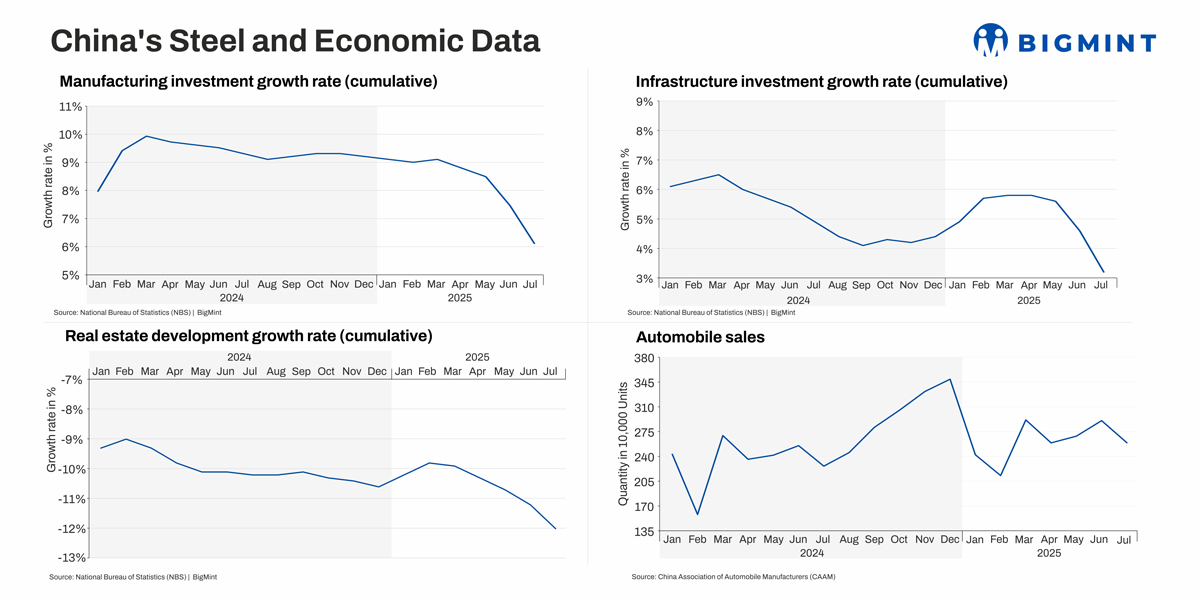

Manufacturing investment growth at 2-year low

The sharp slowdown in the manufacturing investment growth is notable. The growth rate tumbled to just 6.2% in July from over 9% in March. The growth rate fell to a 22-month low in July. China’s official Manufacturing Purchasing Managers’ Index for July was 49.3, clearly showing contraction. The PMI has been low since April when the trade war with the US broke out.

Moreover, China has been battling extensive flooding from torrential seasonal rains that have disrupted business activity in many parts of the country. That apart, relocation of export orders to countries with lower tariffs such as Vietnam has emerged as a challenge for Chinese producers.

Property investments plunge

The infrastructure investment growth rate also slowed down significantly in July. Retail sales, fixed asset investment, and value added of industry growth all reached the lowest levels of the year. Property investments plunged 12% in the first seven months of the year, with residential housing investment dropping nearly 11%.

Crude steel output drops

China’s crude steel production in January-July’25 was over 594 million tonnes (mnt), a decrease of 3.1% y-o-y. Production in July dropped 4% y-o-y to 79.66 mnt. World Steel Association (WSA) data show that China’s steel consumption fell 3.5% y-o-y in 2024 due to the prolonged downturn in the real estate sector. Real estate investments in H1CY’25 dropped 7.2% y-o-y.

The construction sector accounts for around 55% of Chinese steel demand in comparison with the advanced economies, according to the Organization for Economic Co-operation and Development (OECD). This overreliance on the construction sector weighs heavy on domestic steel demand in China.

The 4.5% decline in cement production which reached 958 mnt in 7MCY’25 is also a direct fallout of the crisis in the property sector.

However, pig iron production in the first seven months of CY’25 dropped 1.3% y-o-y, much lower than the rate of decline in crude steel output, indicating that the EAF sector in China is also finding it challenging to increase production and capacity utilisation.

Steel exports rise sharply

At nearly 68 mnt in 7MCY’25, China’s steel exports witnessed a sharp uptick of over 11% y-o-y. China’s direct steel exports to the US are nominal yet the impact of tariffs on the downstream sectors is bound to affect steel demand. China increased steel exports to countries in Southeast Asia, Africa and South America in order to diversify steel supplies globally and counter the impact of tariffs.

At the same time, mounting tariff walls and anti-dumping duties in Asia is forcing Chinese suppliers to seek to circumvent trade barriers and levies by increasing exports of semi-finished steel to third countries for further processing and exports.

Steel imports, on the other hand, decreased by over 15% y-o-y in 7MCY’25 on continued weakness in domestic demand which is expected to decline by around 2% y-o-y in CY’25.

Iron ore imports remain resilient

China’s iron ore imports dropped 2.3% y-o-y, much lower than the rate of decline in crude steel production. China accounts for around 75% of global seaborne iron ore trade. A high level of imports has led to a build-up in China’s portside inventory, which has remained high and kept prices in check.

Coal production surges, imports drop 13%

Domestic coal production increased 4% y-o-y in CY’25. Record-high domestic coal production and weaker coal-fired power generation in China have resulted in declining demand for thermal coal imports into the world’s biggest coal market, with the trend emerging earlier this year, after imports reached 500 mnt in CY’24. Due to low domestic coal prices, weaker demand, and high coal inventories at ports, China’s imports declined 13% y-o-y in 7MCY’25.

According to Carbon Brief, the growth in clean power generation, some 270 terawatt hours (TWh) excluding hydro, significantly outpaced demand growth of 170 TWh in the first half of the year. Solar capacity additions set new records at 212 GW in H1CY’25. But coal-power capacity could surge by as much as 80-100 GW this year, potentially setting a new annual record, even as coal-fired electricity generation declines.

Auto output surges in off-season

China’s automobile production reached 2,591,000 units in July, up 13.3% y-o-y, while sales hit 2,593,000 units, up 14.7% y-o-y, according to China Association of Automobile Manufacturers (CAAM) data. This is the strongest July performance on record. Monthly figures reflected a seasonal dip of 7.3% and 10.70% respectively from June due to summer maintenance shutdowns and traditional off-season demand.

Cumulative January-July production increased 12.7% y-o-y to over 18.2 million units. Notably, while demand for conventional oil-based passenger and commercial vehicles are waning, new energy vehicles (NEVs) are filling the vacuum. From January to July, NEV output reached 8.232 million units and sales 8.22 million, rising by 39.2% and 38.5% y-o-y, respectively, with NEV sales accounting for 45% of the total vehicle market.

Factors to watch out for:

- Broader macroeconomic recovery hinges on amicable resolution of tariff dispute with the US.

- Crude steel output, especially from the high-emissions intensive and polluting units, expected to decrease by 30-50 mnt y-o-y in CY’25, with total output expected to fall below 1 billion tonnes for the first time since the pandemic.

- Chinese steel exports to face growing pressure from anti-dumping, safeguard duties in Asia and beyond over and above the impact of US tariffs. Stringent VAT compliance in H2CY’25 may just bring steel exports lower.

Leave a Reply