- Australian shipments rebound

- Near-term outlook uncertain

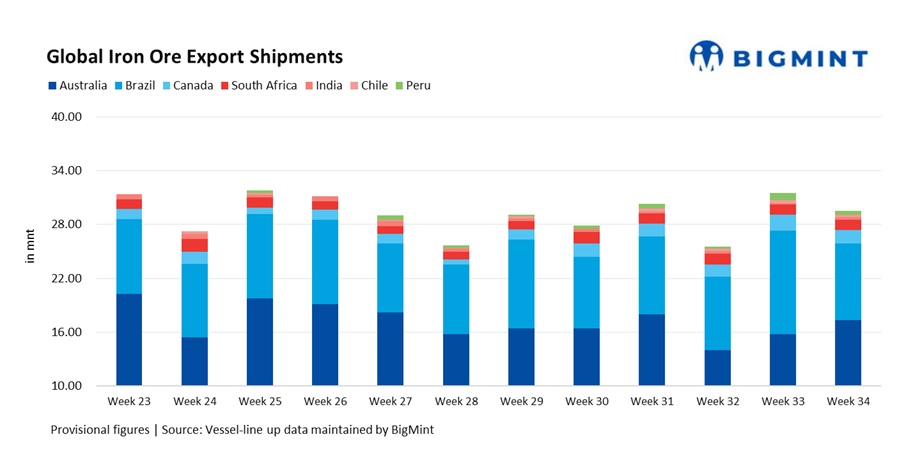

Global iron ore exports declined w-o-w in week 34 (16-22 August) of 2025, slipping by 6.3% to 29.50 million tonnes (mnt) compared with 31.47 mnt in week 33 (9-15 August). The fall marked a loss of momentum after two consecutive weeks of gains, reflecting uneven supply trends across major origins.

The decline was led by a sharp drop in Brazilian shipments (-26% w-o-w) as loadings eased after last week’s surge. Canadian (-18.9%) and Peruvian (-51.3%) flows also weakened, pulling down the weekly total. By contrast, Australia posted a solid recovery (+10.1%) as vessel activity picked up at major ports, while India doubled its export levels, though volumes remained modest on the global scale.

The softer supply picture came amid persistent demand-side concerns, with Chinese steel margins still fragile and procurement largely limited to short-term restocking. Market participants noted that traders remained cautious, especially as seaborne freights moved lower, reducing arbitrage incentives for long-haul shipments.

Country-wise exports

Australia, the world’s largest iron ore supplier, posted a notable recovery in week 34, with shipments climbing 10.1% w-o-w to 17.35 mnt from 15.76 mnt in week 33.

The rebound was driven by increased vessel activity at key Pilbara ports, led by Port Hedland (9.88 mnt) and Dampier (3.15 mnt). Major miners restored loading schedules after earlier weather-related slowdowns, with Rio Tinto contributing 7.17 mnt, BHP 4.48 mnt, and FMG 4.30 mnt.

On the demand side, China absorbed the bulk of Australian cargoes at 14.34 mnt, while smaller volumes moved to Japan (1.25 mnt) and South Korea (1.22 mnt), reflecting steady but subdued regional buying. Overall, Australia’s recovery reaffirmed its role as the backbone of Pacific basin supply, providing much-needed stability at a time when exports from Brazil, Canada, and Peru softened.

Brazil’s shipments slumped by 26% to 8.55 mnt in Week 34 from 11.56 mnt in the prior week, reversing the sharp rebound seen earlier.

Loadings eased across key terminals, including Ponta da Madeira (3.40 mnt), Itaguai (2.17 mnt), and Tubarao (1.93 mnt), as operations normalised following an aggressive push in Week 33.

Vale, Brazil’s top exporter, shipped 4.04 mnt in Week 34, scaling back volumes after ramping up aggressively in the prior week once maintenance and weather-related disruptions had cleared.

Chinese buyers remained the dominant destination, taking in 3.80 mnt of Brazilian cargoes, attracted by the higher-grade ores. However, the longer voyage distance and rising freight costs kept some traders cautious. The pullback underscored the volatility of Brazil’s shipment patterns, which often fluctuate in line with operational schedules and shifting market conditions.

Canada’s iron ore exports declined by nearly 19% in Week 34, slipping to 1.45 mnt from 1.78 mnt a week earlier, as loadings slowed across key terminals.

Port Cartier handled 0.57 mnt, Milne Inlet 0.47 mnt, and Sept-Iles 0.41 mnt, reflecting the impact of seasonal navigation challenges and weather-related risks that often disrupt Canadian shipments.

On the demand side, Europe remained the primary destination, with Spain (0.51 mnt) and the Netherlands (0.31 mnt) among the largest buyers. While Canada’s volumes are modest compared with major exporters such as Australia and Brazil, its reputation for supplying high-grade ore ensures steady demand and adds valuable diversification to Atlantic market supply chains.

South Africa’s iron ore exports registered a modest uptick in Week 34, rising 5.9% w-o-w to 1.19 mnt from 1.13 mnt in the prior week. Shipments through the country’s primary hub, Saldanha Bay, improved slightly to 1.03 mnt.

China remained the largest destination, taking 0.37 mnt, followed by South Korea at 0.35 mnt, alongside smaller flows to European buyers. While South Africa serves as a valuable supplementary source for global buyers seeking to diversify away from the Australia-Brazil duopoly, its recurring operational inefficiencies limit the reliability of its supply.

India’s iron ore exports also picked up in Week 34, rising to 0.28 mnt from 0.12 mnt in the previous week, as improved dispatches supported stronger flows despite ongoing monsoon-related disruptions.

The bulk of shipments was directed to China 0.12 mnt, where Indian low to mid-grade ores continue to find buyers as a cost-effective alternative during periods of heightened demand.

While the week’s rebound underscores India’s ability to respond quickly to short-term market opportunities, its role in global seaborne trade remains largely supplementary. Export volumes are highly variable, shaped by domestic mining activity, policy dynamics, and the shifting appetite of Chinese mills, with sustained growth constrained by competition from major global suppliers.

Chile’s iron ore exports declined 15% w-o-w in Week 34, easing to 0.29 mnt from 0.34 mnt a week earlier. Shipments from Totoralillo (0.20 mnt) and Mejillones (0.09 mnt) held steady but failed to match the stronger levels seen in the previous week.

Although Chile remains a relatively minor player in global seaborne supply, its ores offer a consistent supplementary option for Asian buyers seeking diversification. However, limited production capacity and logistical constraints continue to cap Chile’s export potential, keeping its contribution modest compared with the major origins.

Peru registered one of the sharpest declines in Week 34, with shipments tumbling to 0.38 mnt from 0.79 mnt in the previous week. The drop was driven by reduced loadings at San Nicolas port (0.35 mnt), highlighting the country’s susceptibility to operational shifts at a single major hub.

While Peru remains a relatively small contributor to global iron ore trade, its ability to scale up exports intermittently adds a degree of flexibility to the seaborne market.

Dry bulk iron ore freight rates drop w-o-w on bearish market sentiments

Dry bulk iron ore freight rates weakened across major global routes, weighed down by muted market activity, reduced chartering demand, and fewer fixtures.

Capesize rates came under pressure as bearish sentiment persisted in both the Pacific and Atlantic basins, with limited fresh cargoes eroding confidence among participants. The lack of significant drivers in either basin meant there were few bright spots to offset the downtrend, leaving rates vulnerable to further declines.

Supramax freights on the India-China route also softened, with monsoon disruptions curbing exports and discouraging fresh demand. Overall, sentiment in the freight market remained fragile, reflecting subdued Chinese iron ore appetite and weak steel sector fundamentals.

Outlook

Looking ahead, export momentum may remain uneven as Brazil’s loadings normalise while Australia sustains higher activity. Demand risks remain tilted to the downside, with weak Chinese steel margins and cautious procurement limiting near-term buying appetite. Freight rates are likely to stay under pressure unless cargo volumes improve meaningfully, while seasonal weather disruptions in South America and India could further influence supply flows in the coming weeks.

Leave a Reply