- Pet coke consumption drops 24% y-o-y

- Cement demand slowdown hits consumption

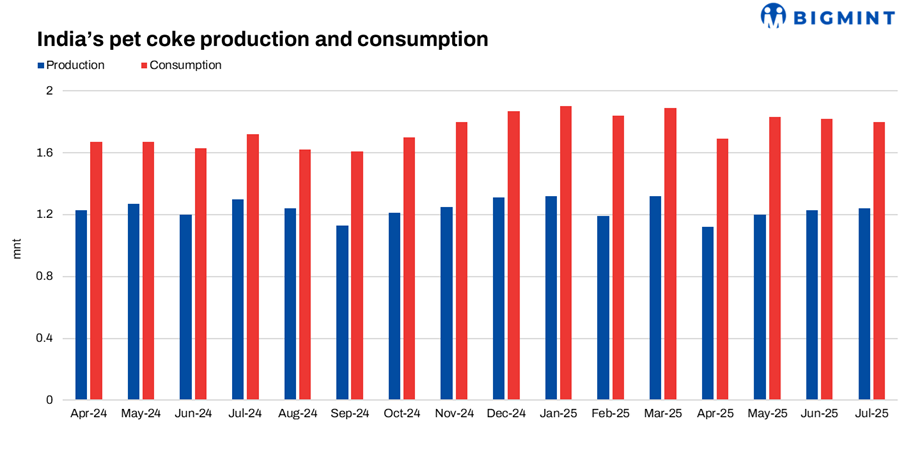

Production moderates y-o-y

India’s domestic production of petroleum coke in July 2025 stood at 1.24 mnt, down around 5% y-o-y from 1.30 mnt in July 2024. On a m-o-m basis, output edged up 1% from 1.23 mnt in June, reflecting steady refinery output.

Cumulatively, April-July 2025 production was 4.77 mnt, down 4% against 4.99 mnt in the same period last year. The moderation continues to highlight refiners’ product-mix preferences towards higher-value fuels like diesel, petrol, ATF, and gas, which remain decisive in delayed coking unit (DCU) operations.

In FY’25, India’s total pet coke output was 14.96 mnt, down from 15.05 mnt in FY’24, accounting for 5.27% of total petroleum product output of 280.45 mnt. In July’s production of 1.24 mnt made up 5.14% of India’s total petroleum product output of 24.04 mnt. Domestic production in July also covered 68.8% of consumption, with the balance met through imports.

Consumption contracts on large base

India’s pet coke consumption in July stood at 1.80 mnt, down 24% y-o-y from 2.37 mnt in July 2024. M-o-m, consumption slipped 1.3% against 1.83 mnt in June. Cumulative consumption in April–July was 6.98 mnt, down 6% from 7.43 mnt in the same period last year.

Consumption in July constituted 9.26% of India’s total petroleum product use of 19.43 mnt. On a cumulative April-July basis, pet coke accounted for 8.6% of total petroleum product consumption of 81.1 mnt.

The cement sector remained the largest consumer, though subdued infrastructure and construction activity during the monsoon weighed on offtake. Other demand came from lime kilns, gasification units, and aluminium industries, partly supported by calcined pet coke (CPC) availability from calciners.

Outlook

Pet coke demand is expected to remain subdued through the monsoon months, in line with weaker construction and cement activity. A recovery in consumption is likely post-monsoon, led by cement production ramp-up. Production trends will stay closely tied to refinery economics and their prioritisation of higher-value fuels, while imports will continue bridging the gap between demand and domestic output.

Leave a Reply