- Active fixtures at higher levels lead to hike in freights

- Baltic index recovery, rising spot & future prices support offers

Dry bulk iron ore freight rates rose significantly across key global routes this week, driven by stronger freight derivatives (FFAs) and higher bunker costs. Market sentiment improved as fixtures gained momentum, with several concluded at higher levels. Additionally, vessel diversions toward grain shipments during the peak agricultural season further tightened supply and supported the rally. As one market source told BigMint, “There’s no shortage, but a surge in cargoes. With the grain season picking up from mid-September to October, the market looks healthy.”

Sources expect the strong momentum to persist, following active trading in the Pacific basin during the 20-26 August period, particularly on the Australia-China route. Toward the end of the week, offer levels strengthened further, with shipowners maintaining the upper hand and resisting fixtures at lower rates.

In the Pacific basin, iron ore demand from operators and traders stayed strong, with fresh cargo inquiries adding to tonnage requirements and lifting short-term sentiment. Major Western Australian miners – BHP, FMG, and Rio Tinto – were also reported to be actively seeking vessels.

Atlantic basin activity was subdued on 25 August due to the UK Bank Holiday, sources said. However, with Pacific basin rates surging, Atlantic market participants followed suit, lifting offer levels as exchanges in the region firmed further.

However, most Capesize cargo enquiries on both the Australia-China and Brazil-China routes were concentrated on September loadings, indicating stronger forward interest but relatively limited near-term demand.

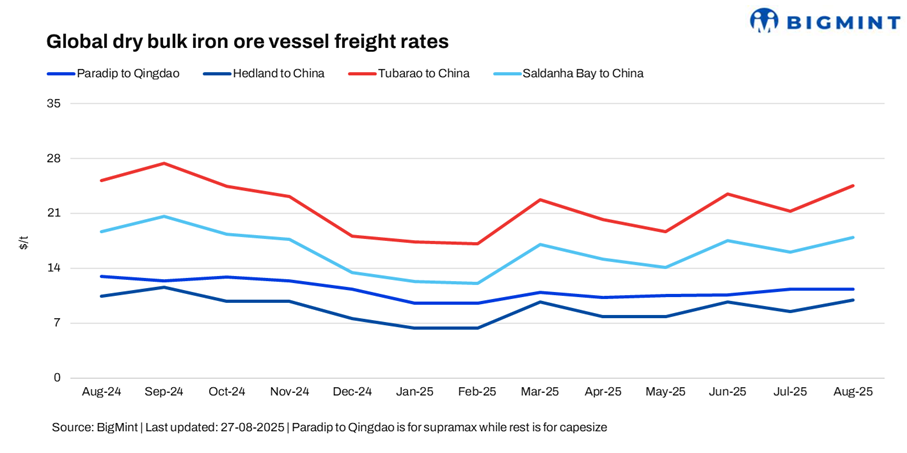

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China inched inched up by $0.25/dry metric tonne (dmt) w-o-w to $11.25/dmt. Demand held steady, with a few export deals for low-grade fines reported, though buyers largely restricted purchases to immediate requirements. Ongoing monsoon rains, however, continued to disrupt mining and dispatch operations, making exports less feasible.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China increased by $1.4/dmt w-o-w to $10.70/dmt. Capesize offers on the Australia–China route started the week at around $9/dmt but steadily climbed to nearly $10.7/dmt as the week progressed, with fixtures concluded at these higher levels.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments also witnessed a hike of $0.5/dmt w-o-w, settling at $25/dmt. On the Tubarao–Qingdao route, only two fixtures were reported this week – the first at a low $22.5/dmt early in the week, followed by a second at a significantly higher level of around $25/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao rose sharply by $1.27/dmt w-o-w, settling at $18.25/dmt. However, no vessel activity was reported on the route, with one source noting, “The South African market remained subdued, with no trades concluded.”

Market highlights

- Baltic index heads north: Baltic Exchanges main dry bulk sea freight index rose sharply w-o-w on 26 August as vessel rates strengthen across the segments. The overall index increased around 77 points to 2,041, with the Capesize index increasing by around 8 points to 3,031. Additionally, the Supramax segment also supported the overall index, rising significantly by 68 points w-o-w to 1,437. Spot iron ore activity appears to be driving spot gains this week with Chinese demand from both Australia and Brazil lifting the market higher, BigMint understands.

- Crude oil futures rise w-o-w: Brent crude oil futures rose this week as geopolitical tensions and supply concerns outweighed softer demand signals. Market sentiment was lifted by disruptions to key energy infrastructure, uncertainty around trade policies, and the possibility of tighter supply from major producers, which collectively supported prices despite a still-fragile demand outlook. Reflecting the stronger sentiment, Brent crude futures increased to $68.80/bbl on 26 August 2025.

- China’s iron ore spot prices stay supported w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $102/tonne (t) CFR China on 26 August, a marginal increase of $1/t w-o-w. The increase was largely supported by China’s decision to ease housing regulations in Shanghai from 26 August 2025, although trading activity remained sluggish. Additional optimism stemmed from expectations of a potential US Fed rate cut in October 2025.

- DCE iron ore futures up w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2025 contract witnessed uptrend w-o-w by RMB 8/t ($1/t)to RMB 777/t ($109/t) on 27 August. DCE iron ore futures gained this week as sentiment improved on China’s move to ease housing rules in Shanghai, raising hopes of stronger downstream steel demand. Expectations of policy support, including a potential US Fed rate cut in October, added to optimism. At the same time, firm spot demand from Chinese mills, along with limited short-term supply disruptions, reinforced buying interest, pushing futures higher despite relatively subdued physical trade.

Outlook

Dry bulk iron ore freight rates remain uncertain in the near term amid ample vessel availability and cautious buying by Chinese steel mills, who remain focused on immediate needs. While steady Australian shipments and recovering Brazilian exports risk oversupplying the market, the upcoming grain season starting mid-September may draw vessels into agricultural trades, tightening tonnage and lending partial support. Even so, sentiment remains cautious, with risks attached to the downside if Chinese demand fails to pick up further.

Leave a Reply