- Low-alumina pellets remain competitive, deals closed

- East coast-based sellers keep focus on domestic market

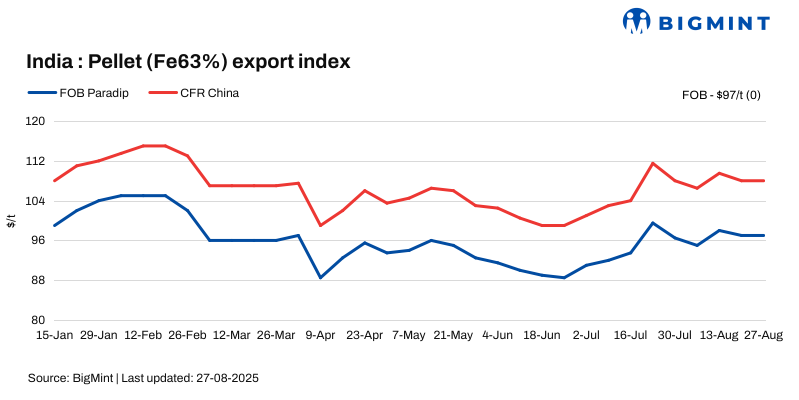

Indian pellet export prices remained range-bound w-o-w, with no fresh deals concluded from the eastern coast, as market dynamics stayed weak. While buyers actively sought low-alumina pellets at competitive levels, a wide bid-offer gap, estimated at around $10-15/tonne (t), stalled trade activity.

Price update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index (FOB east coast) fell by $1/t w-o-w to $97/t on 27 August 2025 against 20 August.

Pellet exporters quoted offers of over $120-125/t CFR for deals to China, which were much higher than prevailing bids. Meanwhile, some sellers did not offer material pellets due to weak pricing.

Market commentary

An east coast-based supplier said, “At current export levels, it is simply not viable to sell. The raw material cost is high, and we are receiving better margins in the domestic market.”

Domestic demand has strengthened in recent weeks, supported by bulk tenders and steady consumption from sponge iron and steel producers. This has diverted volumes away from export channels.

Market participants highlighted that east coast-based suppliers were reluctant to compromise on prices. Another pellet producer noted, “Overseas buyers are quoting very low bids, which does not align with our asking price. Unless the bid-offer disparity narrows, exports from this region will remain limited.”

While eastern coast activity stayed muted, some deals were heard from other regions. A west India-based supplier concluded a pellet (Fe63.5%, 1.5% alumina) export deal of 80,000 t for September loading. In addition, a south India-based producer floated a tender for 50,000 t of pellets (Fe63%, 1.5-2% alumina), indicating that regions with access to low-alumina feedstock were still competitive in the global market.

A few bulk tenders were also concluded in the domestic market, which kept trade sentiments upbeat for pellet suppliers selling to local buyers.

An international trader informed BigMint, “We anticipate more export deals from western and southern India, where pricing is better aligned with overseas demand. But for the east coast, unless domestic prices weaken or raw material costs ease, sellers will prefer catering to local buyers.”

Domestic v/s export realisations gap

Domestic prices exceeded export offers by around INR 1,750/t ($20/t), largely stable w-o-w. Pellet (Fe 63%) prices in Odisha’s Barbil were recorded at INR 8,250/t ($94/t) exw, unchanged w-o-w. Meanwhile, the ex-plant realisations in exports from Barbil were at INR 6,500/t ($74/t) exw.

Rationale

- No confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was not taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for the detailed methodology.

- Fourteen (14) indicative prices were received, and ten (10) were considered for the calculation of the index and given 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices hold firm w-o-w: The benchmark iron ore fines index inched up by $1/t w-o-w to $102/t CFR China on 26 August. The rise was mainly driven by China’s move to ease housing rules in Shanghai from 26 August, though trades were still slow. Optimism also came from expectations of potential US Fed rate cuts in October 2025.

DCE iron ore futures drop d-o-d: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract opened at RMB 775.5/t ($108/t) on 27 August, showing a downtrend of RMB 3.5/t ($1/t) d-o-d.

Outlook

According to BigMint’s analysis, the outlook remains cautious, with participants expecting the eastern coastal market to remain quiet in the near term.

Leave a Reply