- Scrap prices under pressure due to ample arrivals

- Finished steel trade slow amid dull downstream sector

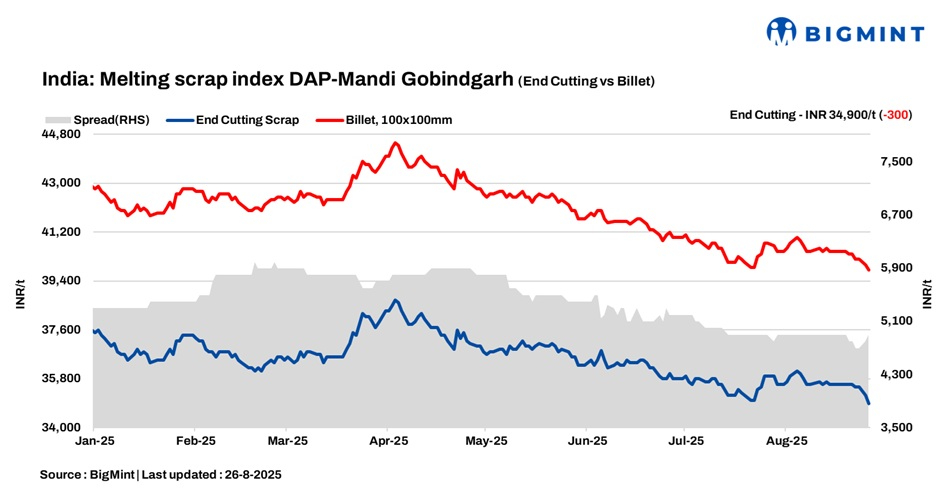

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, decreased by INR 300/tonne (t) d-o-d to INR 34,900/t DAP on 26 August 2025. The Mandi scrap market is reeling under pressure as prices plunged by INR 600/t in just two working days.

The steel market in Mandi Gobindgarh continued its downward trend in the last week of August, weighed down by persistent sluggishness in the finished steel segment. Despite seasonal expectations of a pick-up, no major trades were reported over recent weeks, reflecting continued weak demand from end-user industries.

Heavy monsoon rains further slowed market activity, limiting transportation and disrupting trading momentum across the region.

Domestic, imported scrap market scenario

Scrap suppliers are facing mounting pressure to reduce offers, as steady arrivals from neighbouring states have led to an oversupplied market. Mills, facing limited finished steel orders and ample scrap availability, are leveraging the situation to negotiate lower purchase prices.

Local scrap remains easily accessible, further reducing the need for mills to consider higher-priced imports.

Imported scrap has become uncompetitive in the current environment. The recent strengthening of the US dollar against the Indian rupee has widened the landed cost gap, making overseas offers unattractive for domestic buyers.

With local supply abundant and finished and semi-finished steel markets offering little support, the overall sentiment in the scrap and steel trade remains subdued.

Raw materials scenario

Sponge iron (CDRI) prices in Mandi Gobindgarh fell by INR 100/t d-o-d, assessed at INR 30,100/t DAP on 26 August. On a weekly basis, prices have remained largely stable, with only minor fluctuations observed amid balanced supply-demand dynamics.

Steel grade pig iron prices in Ludhiana were unchanged d-o-d at INR 35,600/t. Prices have remained stable over the past several sessions, supported by steady offtake from local mills.

Steel market trends

Prices of semi-finished steel in Mandi Gobindgarh fell by INR 200/t d-o-d, settling at INR 39,700/t DAP on 26 August. Over the past three weeks, semi-finished prices have dropped by around INR 1,300/t, driven by weak demand and cautious buying from downstream units.

Steel ingot prices across major production hubs also declined by INR 150-400/t, reflecting continued subdued trade activity and limited purchasing interest.

The finished steel market tracked the same downward trajectory. Rebar (Fe500) prices in Mandi Gobindgarh declined by INR 200/t to INR 44,800/t ex-works. Across three weeks, prices have fallen by INR 1,100/t, with mills reporting slow offtake and inventory build-up.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $333-$335/t, which equates to approximately INR 31,571/t (including freight). HMS (80:20) prices in Mumbai fell by INR 300/t to INR 30,800/t DAP today. Indicative prices of shredded from Europe stood at $365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,700/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply