- Steel imports fall to 3.15 mnt in 4MFY’26

- Safeguard, anti-dumping measures curb imports

- Imported HRC from China, Japan costlier than domestic

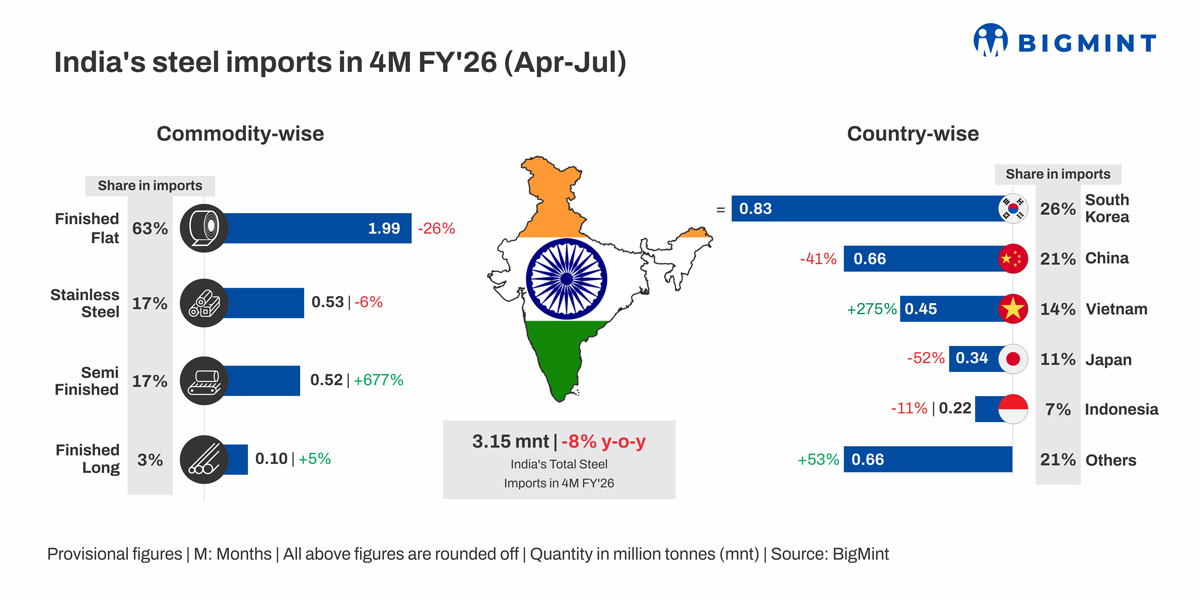

Morning Brief: Imports of steel into India, spanning both carbon and stainless steel products, reached 3.15 million tonnes (mnt) in April-July of the financial year 2025-2026 (FY’26), as per latest data available with BigMint. During the four-month period (4MFY’26) arrival of imported steel cargoes at Indian ports fell by 8% y-o-y compared with 3.43 mnt in the same period of FY’25.

Imports of finished flat steels, primarily plates and coils, reached nearly 2 mnt during 4MFY’26, which had a share of around 63% of total imports. Imports of finished flats fell sharply by 26% y-o-y. While imports of semis jumped y-o-y to over 0.5 mnt during the period, imports of long steel products increased marginally to 0.1 mnt. At 0.53 mnt, stainless steel imports dropped 6%.

Steel imports (including stainless steel) stood at 10.63 mnt in FY’25, up 9% from 9.75 mnt in FY’24, the highest volume recorded in nine years.

Country-wise imports

India’s steel imports from its free trade agreement (FTA) partners, as well as China, moderated considerably in 4MFY’26. Imports from South Korea, the top exporting country to India, remained stable at 0.83 mnt in 4MFY’26. However, imports from Japan tanked 52% y-o-y during the review period, while Chinese exports to India dropped over 40%.

Notably, imports from Vietnam surged significantly during the review period. India has recently concluded an anti-dumping investigation into imports of flat steel from Vietnam, which excludes stainless steel. A duty has subsequently been imposed on that country barring one or two mills.

Why did steel imports drop in 4MFY’26?

Trade protection measures: India’s Ministry of Commerce had announced a provisional 12% safeguard duty on flat steel imports in mid-April 2025, which has a threshold limit for HRC and CRC below which the duty would apply. Recently, the DGTR has proposed an 11-12% safeguard duty for three years on imports of alloy and non-alloy flat steel products. Stainless steel, however, is exempted.

This is the primary reason for steel imports edging down in 4MFY’26 compared with April-July FY’25. Moreover, the DGTR has recommended an anti-dumping duty of $121.5/t on imports of hot-rolled flat products of alloy or non-alloy steel from Vietnam, following the final findings of its investigation, for a period of five years.

Imported HRC costlier than domestic: A BigMint assessment in mid-August showed that the post-duty cost for Chinese HRC importers stood at $644/t, while it was $577/t for Japan, or INR 56,294/t and INR 50,469/t respectively (at prevailing base prices in mid-August). Adding another INR 2,000/t for port handling and miscellaneous charges, the final landed cost came to INR 58,294/t for Chinese HRC and INR 52,469/t for Japanese HRC.

Compared with the domestic HRC price of INR 50,000 /t (ex-Mumbai, excluding GST), Japanese imports were marginally costlier, while Chinese imports were certainly more expensive.

Tightening BIS regulations: The government is moving ahead to ensure stricter control and supervision of steel products and the raw materials used to produce them. In harmony with its policy of expanding the steel quality control orders under the Bureau of Indian Standards (BIS) in India, the government is making efforts to ensure stricter BIS compliance for imports of steel as well as steelmaking raw materials.

The government’s Steel Import Monitoring Scheme (SIMS portal), too, seeks to keep track and control over imports at a time when weak global demand and overcapacity in some countries pose the threat of dumping of inferior products on Indian shores.

Outlook

Steel imports have already moderated significantly in FY’26 and are expected to decline further with safeguard and anti-dumping measures in place.

However, imports of value-added, specials steels required by downstream players such as auto OEMs, the electrical and engineering sectors will continue to remain and import duty, in any form, will hike costs for the downstream players and render a large majority of them

uncompetitive.

That being the case, the domestic steel sector will have some respite going forward, although calls for a higher safeguard duty have already been heard. The stainless steel players, too, have called for a duty to restrict the continuous inflow of imports from Indonesia and China.

It remains to be seen how the government will react to that given the significant presence of a large MSME downstream sector in the stainless steel industry dependent on imports.

Leave a Reply