- Sponge iron prices gain by INR 200/t d-o-d

- Semis, finished steel tags continue to slide

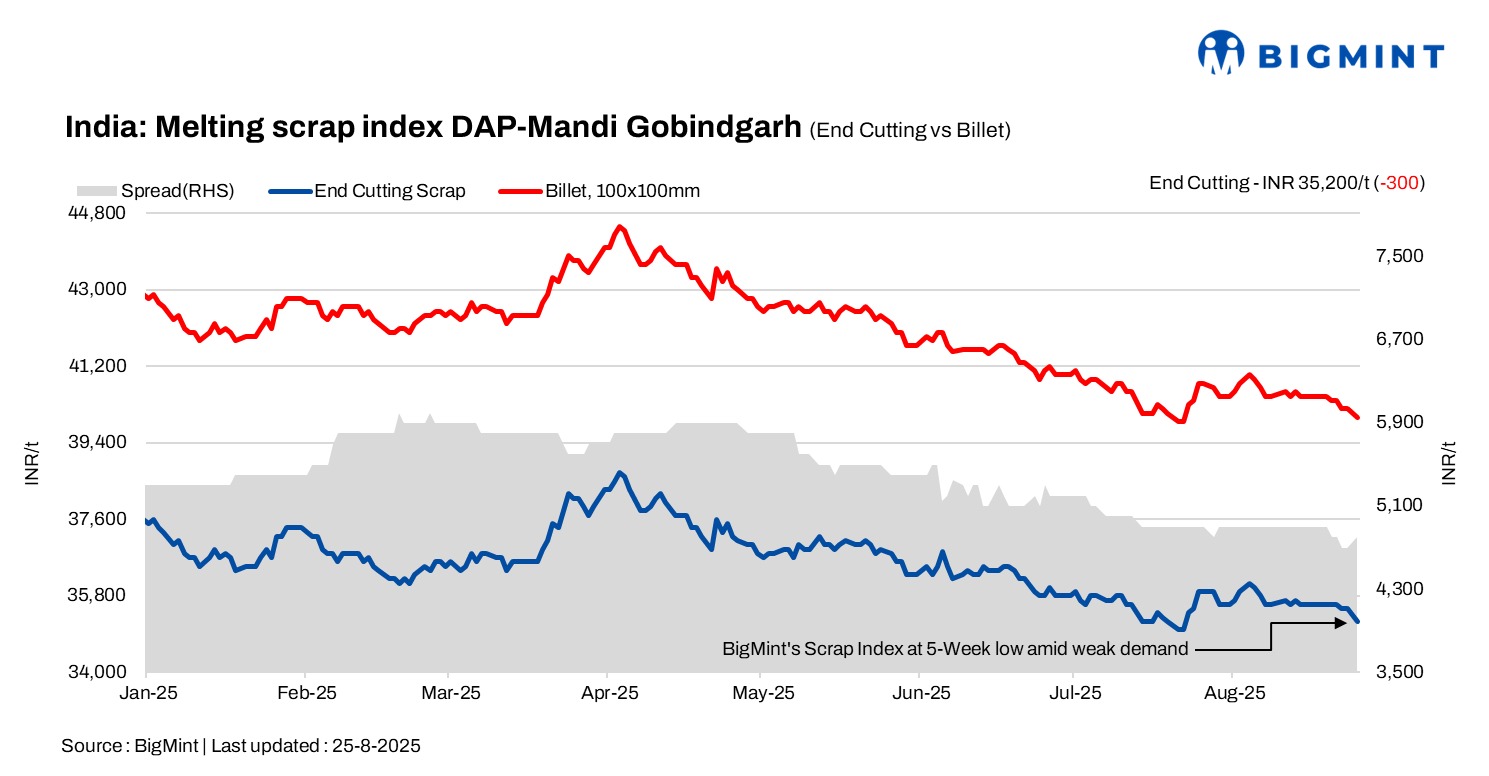

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, decreased by INR 300/tonne (t) d-o-d to INR 35,200/t DAP on 25 August 2025. Today, Mandi’s scrap prices hit a five-week low, attributed to limited buying interest and persistently weak demand for steel in the region. The last time the index touched this level was on 22 July 2025.

Market participants noted that heavy rainfall has disrupted trade activities, resulting in sluggish scrap purchasing and ongoing liquidity challenges. Despite these headwinds, there is no reported shortage of scrap in the Mandi market.

According to a local scrap stockiest, domestic scrap prices in Mandi have remained range-bound over the past two weeks. Local mills have refrained from making significant bookings of imported scrap, signalling a continued reliance on domestic suppliers. Scrap inflow from neighbouring states remains steady, but muted demand for finished steel and ample inventory levels are prompting mills to further lower their purchasing prices. The prevailing slow market conditions continue to exert downward pressure on both scrap trading activity and prices.

Raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh increased by INR 200/t d-o-d, reaching INR 30,200/t DAP. However, this recovery brings prices back to levels last seen three weeks ago, reflecting ongoing volatility in the market.

Steel grade pig iron prices in Ludhiana remained steady d-o-d, assessed at INR 35,600/t.

Steel market trends

In the semi-finished segment, prices of semi-finished steel in Mandi Gobindgarh dropped by INR 300/t, settling at INR 40,000/t DAP on a d-o-d basis. Similarly, steel ingot prices across key production hubs witnessed a fall of INR 50-400/t, further signalling subdued trading activity and a lack of buying momentum.

The finished steel market mirrored this downtrend. Rebar (Fe500) prices in Mandi slipped by INR 100/t, reaching INR 45,000/t ex-works, while HR strip (patra) recorded a price cut of INR 200/t, bringing prices down to INR 42,100/t ex-works.

Market insiders attribute the continued price corrections to sluggish construction activity, muted end-user demand, and cautious buying across distribution channels. With monsoon-related disruptions and limited infrastructure spending impacting offtake, industry participants are closely monitoring for any signs of a turnaround in the coming weeks.

Overview of Alang scrap market

On 25 August, melting scrap prices in Alang’s ship-breaking market dropped by INR 200/t, with HMS (80:20) now priced at INR 31,500/t ex-yard, according to BigMint. This decline comes amid sluggish demand for finished steel in the region, where both semi-finished and finished product prices fell by INR 100-200/t in the previous session. The reduced pace of scrap trading today has also prompted sellers to ease their offers to maintain liquidity.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $333-$335/t, which equates to approximately INR 31,528/t (including freight). HMS (80:20) prices in Mumbai fell by INR 300/t to INR 31,100/t DAP today. Indicative prices of shredded from Europe stood at $365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,650/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply