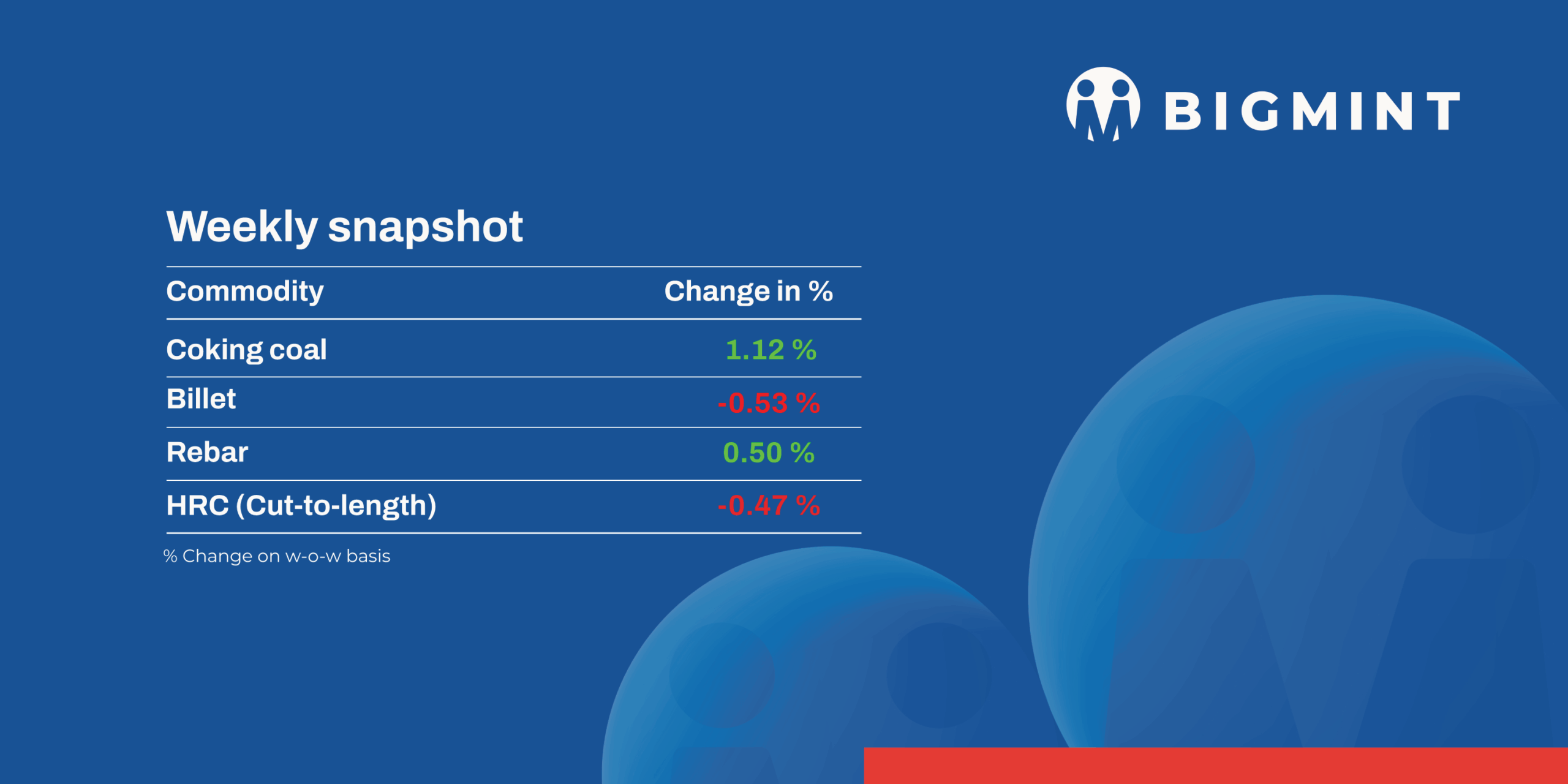

The domestic steel market saw negative trends in prices during week 33 ( 18-23 Aug, 2025). Semi-finished steel prices dropped in the range of INR 200-700/tonne (t).

Iron ore and pellet

- In OMC’s iron ore auction of 2.395 mnt (1.493 mnt fines and 0.902 mnt lumps) on 19 August, around 1.472 mnt (98.6%) of fines (Fe 51-65%) and 0.889 mnt lumps (Fe 60-65%)were booked at INR 2,650-5,550/t and 5,400-7,250/t, respectively-the fines received premiums of INR 50-700/t over base prices while lumps fetched upto 26% premium over the base prices. Fines bids (weighted average) rose by INR 300/t m-o-m while lumps remained largely stable. The miner increased base prices by INR 300/t and INR 350/t m-o-m for most fines and lumps lots, respectively.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, rose by INR 250/t ($3/t) w-o-w to INR 10,350/t ($118/t) DAP on 22 August. Raipur-based producers kept their offers for Fe 63% (+/-0.5%) to INR 10,100-10,300/t ($116-118/t) exw. Deals for around 100,000 t pellet were concluded in Raipur last week.

- NMDC Karnataka’s auctions saw 148,000-t iron ore booked. Lumps fetched premiums of up to 7%. From Donimalai on 19 Aug- 16,000-t lumps (10-40 mm, Fe 55%) and 16,000-t fines (Fe 56%) at INR 3,348/t and INR 2,994/t (INR 5/t premium), respectively. While

- Kumaraswamy auction on 20 Aug- 64,000-t lumps (10-40 mm, Fe 59.35-59.71%) at 4-7% premium against base price INR 4,300-4,404/t; 52,000-t fines (Fe 60.4-60.72%) at up to 4% premium against INR 3,883-3,960/t. Prices include royalty, DMF, and NMET.

- NMDC Chhattisgarh conducted an auction for 64,500 t iron ore from its Bacheli mines on 21 Aug. Around 12,900 t CLO (10-40 mm, Fe 67%) got sold at 9% premium against a base price of INR 6910/t, whereas rest 51,600 t (Fe 64%) fines remained unsold. Prices were on FOR basis, inclusive of royalty, DMF, and NMEDT charges.

Coal

- South African coal prices in India moved slightly higher this week, with RB2 assessed at INR 8,300/t exw-Gangavaram, up INR 50/t, while RB3 increased INR 100/t to INR 7,200/t. Eastern port RB2 offers were heard at INR 8,300-8,350/t, but buyers stayed cautious as high levels restricted trades.

- Domestic coal prices in India showed mixed trends this week. BigMint assessed 5000 GCV at INR 5,250/t exw-Bilaspur, up INR 250/t w-o-w, while 4500 GCV stayed unchanged at INR 4,500/t. The rise in 5000 GCV was mainly due to mining disruptions during the monsoon, while improving steel demand added support.

- BigMint’s premium hard coking coal (PHCC) index was assessed at $200/t CNF Paradip on 22 Aug, down $12/t w-o-w. Offers for Australian coal stood at $205–210/t, but bids stayed lower at $198–200/t, reflecting subdued demand. No deals were concluded in the window, with six firm datapoints forming the index.

- Met coke prices in India stayed steady this week, with BF-grade (25–90 mm) assessed at INR 29,000/t ex-Jajpur and INR 30,000/t ex-Gandhidham. Tight domestic supply and firm coking coal costs supported stability, as Australian premium HCC edged up $3/t w-o-w to $188/t.

Ferrous Scrap

- India’s imported scrap market stayed sluggish throughout the week, with holidays, weak construction demand, and a stronger dollar keeping mills cautious. HMS 80:20 offers near $340/t CFR failed to attract buying interest, A persistent bid–offer gap of $10-15/t restricted deals while shredded from UK/Europe held at $365-370/t CFR against lower bids of $355-360/t.

- High freight costs pushed Australian shredded cargoes toward Indonesia, while Pakistan’s removal of duty on HMS diverted material away from India, further limiting supply options.

Ferro alloys

- Silico Manganese:Indian silico manganese prices (60-14) were down by INR 500/t ($6/t) w-o-w to INR 70,600-70,660/t ($809-809/t) in the key regions of Durgapur, Raipur, and Vizag. Prices softened as buyers showed limited interest, adopting a cautious stance amid resistance to higher price levels.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices dropped slightly by INR 200/t ($2/t) w-o-w to INR 70,640/t ($809/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, dipped by INR 250/t ($3/t) at INR 70,700/t ($810/t) w-o-w.The slight dip in ferro manganese prices was driven by weak demand from steelmakers, stable supply levels, and limited spot market activity, leading to minor downward price adjustments across key regions.

- Ferro Silicon:Indian ferro silicon prices dropped by INR 750/t ($9/t) w-o-w to INR 92,750/t ($1,062/t) exw-Guwahati. Meanwhile, Bhutan’s offers dipped by INR 1,000/t ($11/t) to INR 93,500/t ($1,071/t) exw. The market remained subdued last week, marked by sluggish inquiries and bulk deals concluded at lower price levels.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices rose by INR 1,900 ($22/t) w-o-w to INR 103,500/t ($1,185/t) exw-Jajpur. Offers from sellers went up due to limited supplies in the market and good realisation in exports.

- Addiotionally, at OMC’s chrome ore auction on 19 Aug’25, 71,000 t was sold, with bids edging up by 1-2% (INR 50-449/t) m-o-m across most grades. Ferro chrome auction scheduled on 25 Aug’25.

Semi Finished

- Indian semi-finished steel prices showed downward trend as per BigMint’s assessment. Domestic billet prices in all key locations moved down by INR 200-700/t across regions. Major down seen in Chennai region by INR 700/t. Sponge iron prices witnessed mixed trend, almost all key locations moved down by INR 300-500/t and other region remain stable while only Bellary and Ramgarh were up INR 50-100/t.

- Indian DRI (Direct Reduced Iron) export offers increased by $1 stood at CPT Raxaul, at $333/t while, CPT Benapole offers seen increased by INR 4/t and stands at $342/t.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 10,000 t of steel-grade pig iron on 22 Aug’25, with the entire quantity booked at an average price of INR 32,000/t (by road). However, management approval is still pending. Bids fell by INR 400/t from the previous auction on 7 Aug for 10,000 t, in which the entire quantity was booked at an average of INR 32,400/t (by road).

Finished Long Steel

- IF-rebar:India’s IF route finish market activity remains subdued this week, as weak market sentiment and a decline in inquiries have led to sluggish order bookings. Purchases are largely confined to urgent needs, driven by volatility in raw material prices, particularly sponge iron and billet, and heavy monsoon rains. To boost sales and liquidate inventories, manufacturers are pressured to reduce offers. Inventory levels are reportedly at 10-12 days, and market players expect prices to remain under pressure in the near term due to muted construction activity during the ongoing monsoon season and upcoming festivities.

- On a weekly basis, in rebar steel prices witnessed plunged in the range of INR 100-1,000/t across the regions except in Raipur market where prices edged up by INR 200/t as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,700-40,100/t exw Raipur, INR 43,200-43,800/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 42,500-43,000/t exw Raipur.

Trade reference prices of wire rod hovering at INR 40,800-41,400/t ex Raipur. - BF-rebar: India’s trade-level blast furnace (BF) rebar prices declined w-o-w across major domestic markets amid demand slowdown due to rains across key Indian markets which dampened and weighed on the market sentiments.

- Trade-level BF rebar prices dropped by INR 500/t ($6/t) w-o-w to INR 47,900/t ($548/t) exy-Mumbai, as per BigMint’s assessment on 22 August 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices fell w-o-w to INR 46,500-47,500/t ($532-543/t) FOR Mumbai owing to need basis procurement amid heavy monsoons in major parts of the country, which led to logistics bottlenecks in the market impact the supply chain.

Flat Steel

- Trade-level prices of hot-rolled coils (HRCs) in India remained range-bound w-o-w to INR 49,500-51,200/t ($568-588/t). Moreover, cold-rolled coil (CRC) prices stayed stable w-o-w, ranging INR 55,200-59,100/t ($634-679/t).

- Domestic HRC prices remained stable this week as trading activity continued to be affected by monsoon rains in key markets. Demand was moderate but slightly weaker than last week, with buyers largely restricting purchases to immediate requirements.

- India’s bulk imports of HRCs touched 250,945 t as of 19 August, based on vessel line-up data. Around 234,796 t of additional cargo are expected by early-September.

- India’s bulk exports of HRCs touched 107,085 t as of 19 August, based on vessel line-up data from BigMint. Moreover, around 74,260 t of additional cargo is expected to be dispatched overseas.

- The Middle East’s (ME) imported hot-rolled coil (HRC) market saw a surge in competitive offers with Indian mills resuming exports coinciding with a rise in Chinese offers. Indian HRC export offers to the Middle East are ranging between $525-535/t CFR UAE, with a recent deal concluded at similar levels for around 25,000 tonnes (t) for September shipment to a UAE-based tube-maker and re-roller.

- BigMint’s India hot-rolled coil (HRC, S275) export index remained stable w-o-w at $555/t (FOB main port). This stability in prices can be attributed to the ongoing summer holidays as well as festive holidays in certain regions of Europe.

Leave a Reply