- MCX zinc rises on 10% fall in LME stocks

- HZL eyes uranium, rare earth expansion

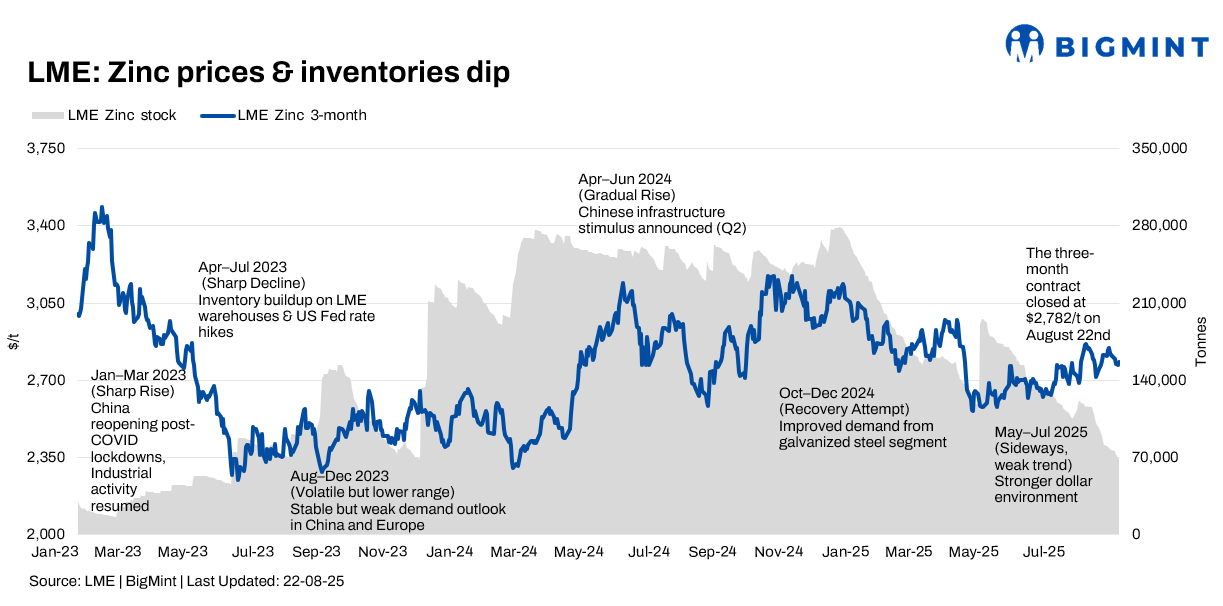

The London Metal Exchange (LME) zinc market experienced downward pressure during Week 33 (18-22 August 2025), influenced by broader global economic concerns. However, this downtrend was partly cushioned by continued destocking of LME inventories, resulting in a volatile trading environment.

Price trends

LME zinc cash-settlement prices trended downward, opening the week at $2,787/tonne (t) on 18 August and closing lower at $2,762/t on 21 August. By 22 August, prices had recovered to $2,772/t. This overall decline of $15/t reflects the market’s reaction to persistent oversupply concerns and uncertain global economic data.

The three-month LME zinc contract mirrored this pattern, starting at $2,796/t on 18 August and closing at $2,769/t on 21 August.

The downtrend was primarily driven by investor concerns about the US economic outlook, following hawkish signals from the US Federal Reserve indicating a cautious approach to interest rate cuts.

LME zinc inventories continued their declining trend during the week, falling 10% to 68,075 t on 22 August from 75,850 t on 18 August. This continued destocking indicates a tightening global supply of readily available zinc and helped prevent a more significant price decline.

MCX zinc trends (18-22 August)

MCX zinc prices experienced a volatile week, reflecting mixed sentiment despite downward pressure in global markets. On 18 August, zinc futures settled at INR 265,800/t, driven lower by bearish global sentiment and slackening domestic demand. However, prices rose to INR 267,000/t on 22 August.

The increase was likely supported by tightening LME inventories and a slight recovery in global sentiment towards the end of the week. Analysts noted that trimming of positions by market participants, due to weak demand, exerted downward pressure throughout the week, even amid the modest recovery.

SHFE zinc trend

SHFE zinc prices remained under pressure during Week 33, largely influenced by weak domestic fundamentals and persistent oversupply concerns. The most-traded SHFE zinc 2510 contract saw a slight rebound at the end of the week, closing up at RMB 22,300/t on 22 August, but the overall trend remained weak. The fluctuation was influenced by expectations ahead of Fed Chair Jerome Powell’s Jackson Hole speech, but oversupply and tepid domestic demand capped gains.

HZL eyes uranium, critical minerals expansion

Hindustan Zinc Ltd. (HZL) is evaluating uranium mining opportunities, contingent on policy approval for private sector participation. CEO Arun Misra confirmed the company’s plans to bid for uranium blocks in alignment with India’s nuclear expansion programme. HZL has also secured its first rare earth block in Uttar Pradesh, targeting neodymium production within 5-6 years while pursuing lithium, antimony, germanium, copper, and graphite opportunities via global partnerships.

Nexa resumes Cerro Pasco operations

Nexa Resources restarted operations at its Cerro Pasco Complex in Peru after protests subsided. The one-week halt resulted in a production loss of 1,200 t zinc, which the company expects to recover within a month. Production guidance for 2025 remains unchanged, with El Porvenir and Atacocha mines expected to deliver stable zinc and lead volumes.

Outlook

The near-term zinc outlook remains cautious. While falling LME inventories are lending support, persistent oversupply concerns and weak macroeconomic indicators are expected to keep prices volatile. Market participants will closely track Chinese demand trends and broader global economic signals for further direction.

Leave a Reply