- Infra projects boost demand in China

- Softer US inflation data ignites optimism

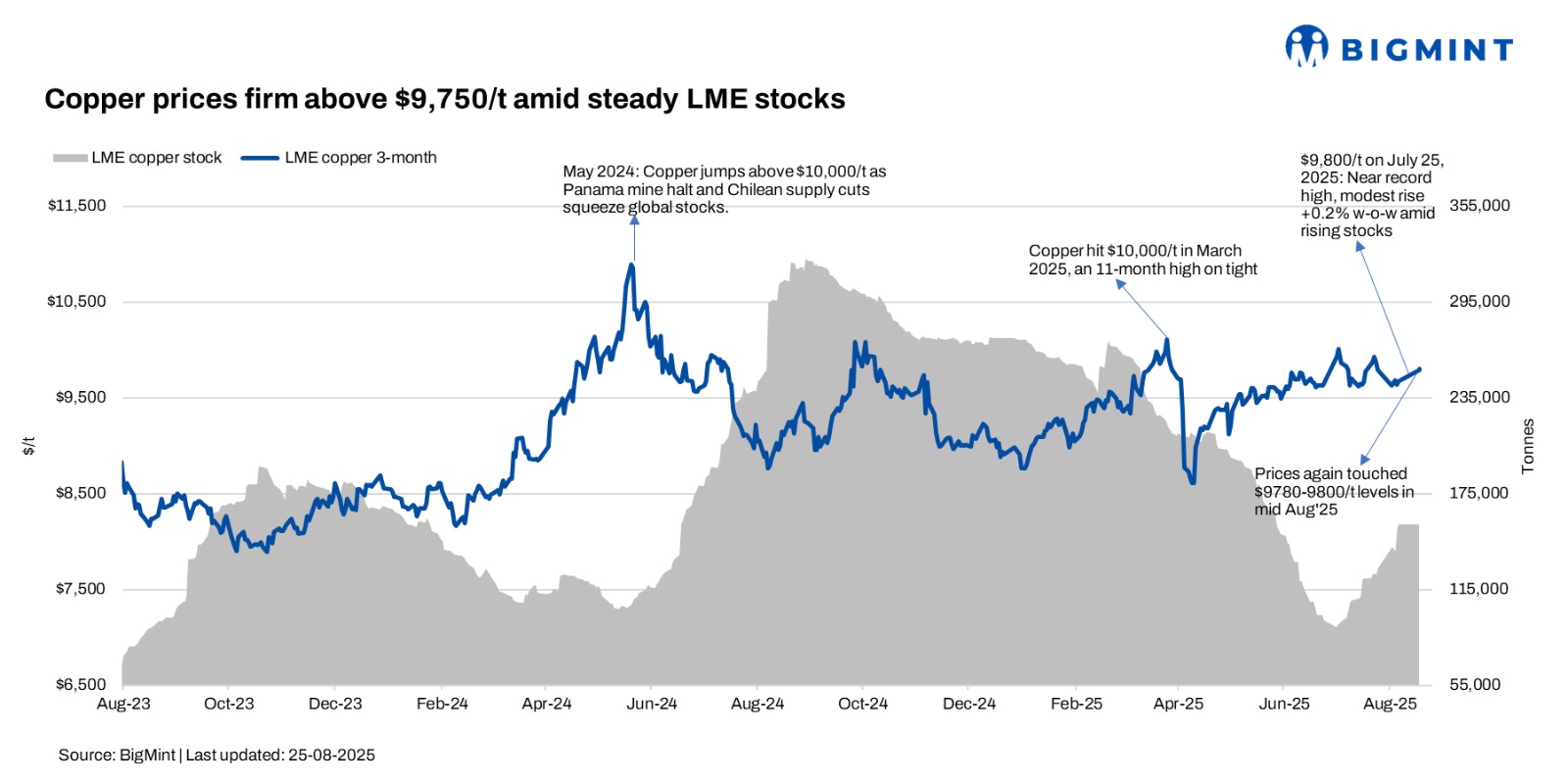

Copper prices on the London Metal Exchange (LME) moved slightly higher last week, supported by stronger demand from China, supply challenges in South America, and improving economic signals from the US and Europe. The benchmark 3-month copper contract closed at $9,810/t on 23 August, 2025, up $60/t from $9,750/t on 16 August.

LME inventories saw a small decline, slipping from 156,350 t on August 21 to 155,800 t on 23 August. While still higher than early-summer levels, the drawdown points to steady physical demand.

In China, the world’s top consumer, optimism came from a RMB 200 billion ($27 billion) infrastructure package aimed at power grids and transport projects. At the same time, China’s refined copper imports for July rose 8% year-on-year to 503,000 t, showing a rebound in demand.

On the supply side, spot treatment and refining charges (TC/RCs) in Asia dropped below $50/t / 5c/lb, compared with around $60/t in July. This signals tighter concentrate supply, with Chile reporting July copper production down 4% year-on-year due to weather and operational issues. Peru also faced similar challenges, adding to the squeeze.

Outside Asia, sentiment was supported by macro news. In the US, softer inflation data raised hopes that the Federal Reserve may ease its stance later this year, boosting risk appetite in commodities. In Europe, Germany’s manufacturing PMI showed a slight uptick, suggesting a stabilizing trend in industrial activity after months of contraction.

Together, firmer Chinese demand, supply tightness in Latin America, and improving signals from the U.S. and EU helped copper prices hold above $9,800/t. Analysts expect prices to stay in the $9,700–9,900/t range near term, with upside if inventories keep falling.

Leave a Reply