- US scrap prices slip as global demand softens

- Turkish mills cautious as rebar sales remain weak

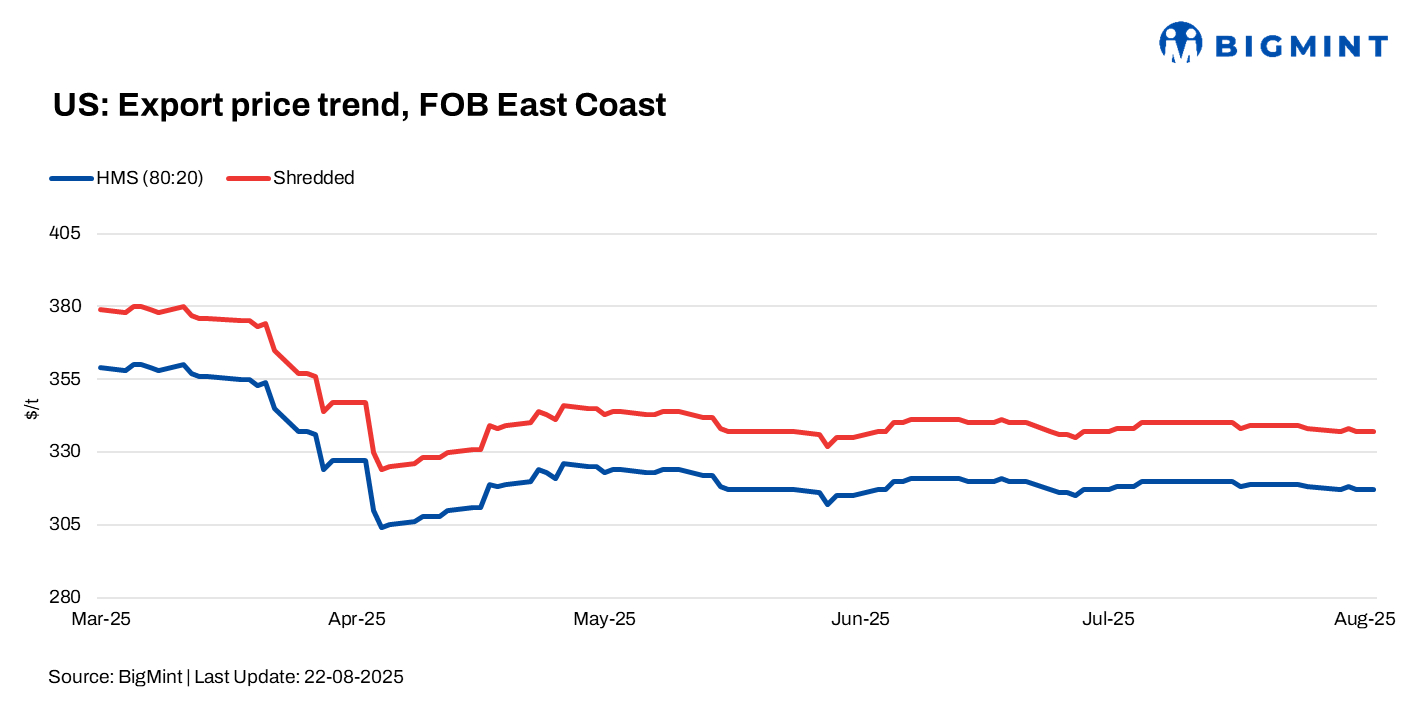

US ferrous scrap export prices softened last week, weighed down by weak buying interest from key importers. While FOB values slipped on the East Coast, trade activity across Turkiye, Bangladesh and Vietnam showed a mixed trend, with mills largely holding back from fresh bookings.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $317/t, down by $2/t w-o-w.

- Shredded – $337/t, down by $2/t w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – down by $1/t w-o-w at $346/t.

- Vietnam – up by $3/t w-o-w at $333/t.

- Bangladesh – down by $1/t w-o-w at $352/t.

Updates on key importers

Turkiye: Turkiye’s deep-sea scrap market held largely stable w-o-w as mills showed limited buying interest. Weak domestic and export rebar and wire rod sales, along with cautious market sentiment ahead of September shipments, kept fresh bookings subdued.

Factors shaping Turkish scrap demand

- Weak domestic and export rebar and wire rod sales

- Higher collection and freight costs, plus euro-dollar fluctuations

Despite steady billet demand providing some support, mills stayed cautious, awaiting clearer price direction and potential movements for September shipments.

Bangladesh: Demand for US-origin scrap remained muted over the past week as heavy rains disrupted construction activity and curbed finished steel consumption. Mills avoided large-scale bookings, opting instead to monitor demand conditions closely.

With weak end-user demand persisting, buying interest for US-origin scrap is likely to stay limited in the near term, keeping import prices under pressure.

Vietnam: Vietnam’s demand for US-origin scrap stayed limited, with offers rising to $340-350/t CFR, but bids held at $325-330/t as weak construction activity and heavy rains kept buyer interest subdued.

Despite a slight pickup in demand, competition from rising billet and finished product supplies is expected to cap any major improvement in higher-grade scrap consumption.

Outlook

Overall, US-origin scrap demand across key Asian markets is expected to stay cautious in the near term, with weak downstream steel consumption and seasonal factors curbing buying momentum. Some support may emerge from billet demand and limited supply, but broader market sentiment remains soft.

Leave a Reply