- Production remains mixed; only AM/NS logs uptick

- Safeguard duty boosts finished prices in Q1FY’26

- Lower prices in Q2FY’26 expected to impact profits

Morning Brief: Indian tier-1 mills had a mixed start to the fiscal year, with a q-o-q decline in sales volumes in Q1FY’26 (April-June 2025). However, there was cause for cheer, with all except SAIL recording a healthy uptick in their EBITDA per tonne.

Meanwhile, production showed uneven trends, with most primary steelmakers witnessing a mild decline q-o-q.

The q-o-q decline in sales is in line with prevailing trends. Generally, the January-March quarter sees heightened activity, as both steel producers and consumers rush to achieve annual targets, following which momentum wanes.

However, the rise in EBITDA despite softer sales demonstrates the positive impact of the provisional safeguard duty and declining imports, which led to a surge in finished product prices.

BigMint analyses how tier-1 mills performed across various metrics in Q1FY’26.

Production remains mixed bag; only AM/NS records rise

The production enthusiasm seen in Q4FY’25 softened evidently, with JSW, Tata Steel, and JSP recording lower volumes q-o-q.

JSW Steel (standalone) was as the leading producer in Q1FY’26, with 5.70 million tonnes (mnt). The 6% decline q-o-q was due to planned maintenance shutdowns, which led to lower capacity utilisation at 87% this quarter against 93% in the previous one.

Tata Steel’s output fell 4% q-o-q to 5.24 mnt, impacted by, again, maintenance shutdowns in Jamshedpur (relining of the G blast furnace) and Neelachal Ispat Nigam Limited (NINL).

Both JSW and Tata Steel witnessed marginal variations y-o-y.

SAIL churned out 5.1 mnt, stable q-o-q. However, y-o-y, there was a strong 9% growth.

Meanwhile, only AMNS was able to lift its production by 8% q-o-q, though volumes dipped 2% y-o-y.

JSP recorded a slight 1% dip q-o-q to 2.09 mnt, while volumes increased 2% y-o-y. The company commissioned a 0.20 million tonnes per annum (MTPA) continuous galvanising line (CGL-1) at Angul, while the commissioning of India’s 2nd-largest 5,499-m3 blast furnace is in its final stage, with first hot metal tapping expected in Q2FY’26.

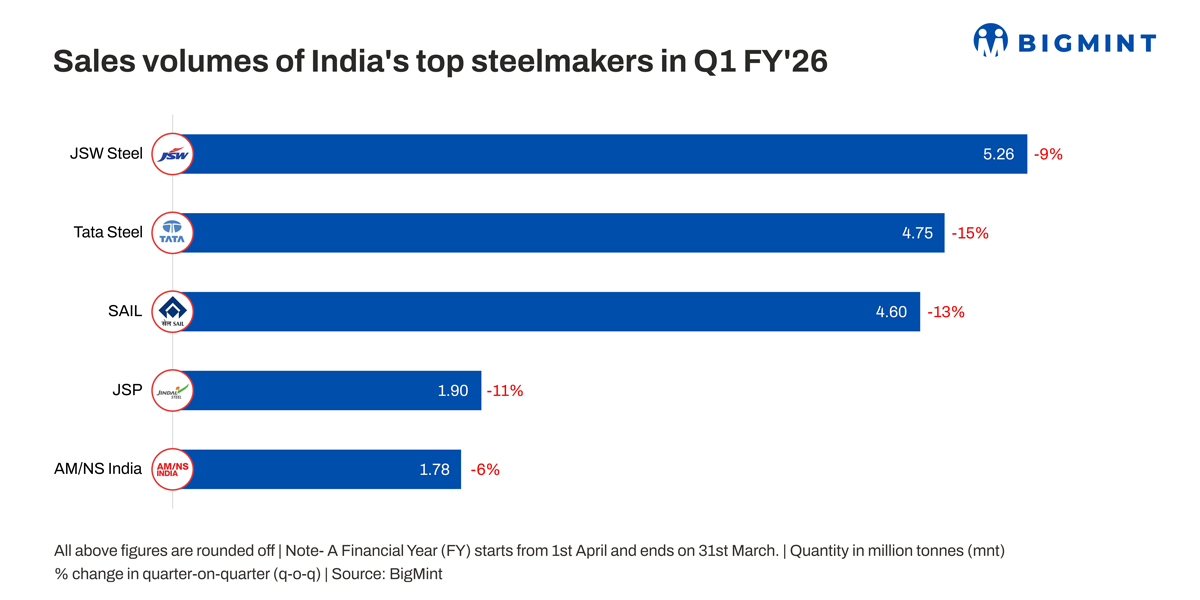

Sales decline across board amid weak demand signals

Throughout the first quarter, lacklustre steel demand plagued Indian steelmakers, leading to sales eroding by 6-15% q-o-q.

Following the safeguard duty recommendation and supply shortages in Q4FY’25, prices had shot up, but as Q1FY’26 arrived, the rush to meet targets faded.

Consequently, buyers showed a lack of interest, unwilling to raise their production costs by procuring material at the prevailing levels. Pre-monsoon showers and the early onset of the rainy season also impacted end-user demand, especially in the construction sector.

JSW Steel’s sales fell 9% from the previous quarter, despite a 3% rise from a year earlier.

Tata Steel saw a 15% q-o-q decline in sales, the sharpest among the five top producers, which led to a marginal build-up of inventory. The company’s sales were also down 4% y-o-y. Exports, however, bucked the trend, rising 12% q-o-q to 0.37 mnt.

SAIL recorded a 13% q-o-q drop, though volumes surged 15% y-o-y. The state-owned steelmaker attributed the q-o-q decline to typical seasonal weakness and inventory reduction by its distributors.

Meanwhile, AM/NS India’s shipments fell 6% q-o-q and y-o-y. JSP’s volumes were down 11% q-o-q and 9% y-o-y.

EBITDA rises amid strong gains in finished steel prices

A bright spot was that lower sales did not translate into reduced profitability. Buoyed by the safeguard duty, a steeper rise in finished prices than input costs bolstered the margins of all steelmakers except SAIL.

Notably, blast furnace (BF)-route rebar and hot-rolled coil (HRC) prices were higher by 7% and INR 4% q-o-q, while iron ore and coking coal rose a minor 2%. However, it is to be noted that although average finished product prices in Q1FY’26 were higher than Q4FY’25, values began to ease gradually amid price resistance and inventory build-up.

JSW Steel’s EBITDA/t surged 21% q-o-q and 26% y-o-y. Indian operations benefitted from a q-o-q drop in coking coal costs, though this was partially offset by higher fuel consumption due to shutdowns. Iron ore costs were steady q-o-q.

Tata Steel’s EBITDA/t increased by 18% q-o-q and 10% y-o-y. Realisations increased by INR 2,600/t, helping to counteract the q-o-q drop in sales volume. Coking coal costs were said to be $10/t lower on a consumption basis in India.

SAIL’s EBITDA/t eroded by a sharp 26% q-o-q and 13% y-o-y. SAIL cited inventory valuation loss and lower price realisations as the primary reasons for the lower margins q-o-q.

JSP witnessed a significant climb of 35% q-o-q and 16% y-o-y. The blended average selling price (ASP) rose q-o-q, driven by higher steel prices and a mild increase in the share of flats in the sales mix.

Outlook

Despite the short-term headwinds, all major mills are actively pursuing aggressive expansion plans. AMNS considers India to be the fastest-growing major steel market, with demand favourably supported by infrastructure investment. JSW projects demand growth of 8-10% in FY’26.

However, pricing may come to be a sore spot in Q2FY’26, which could impact profitability. JSP expects domestic steel prices to drop by 5-7% q-o-q in Q2FY’26. Even JSW expects realisations to soften in Q2 but aims to offset part of the impact through cost efficiencies and higher sales volumes. SAIL too believes that the monsoon impact will lead to q-o-q price corrections, though expectations are that July’s slide will be offset by a recovery in August and September.

Leave a Reply