- Some tier-1 mills cut list prices, others offer discounts

- IF-rebar prices edge lower amid need-based demand

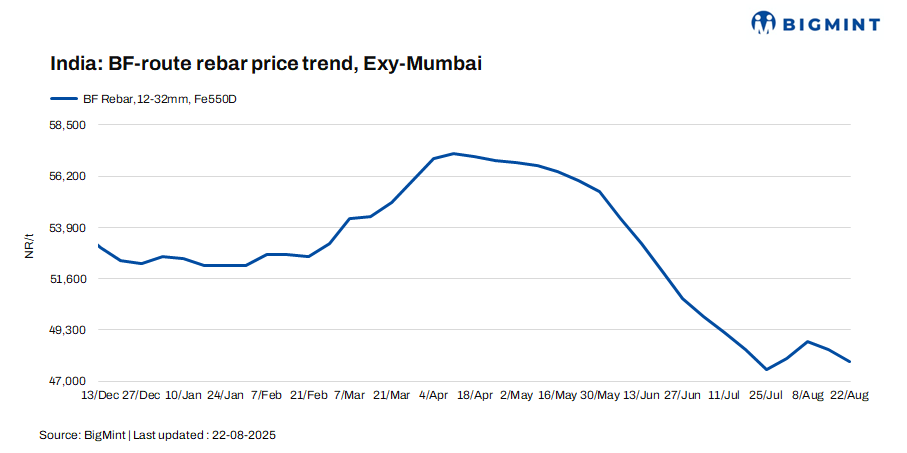

India’s trade-level blast furnace (BF) rebar prices declined w-o-w across major domestic markets amid a demand slowdown due to rains.

Some primary mills reduced rebar list prices by INR 1,000/t ($12/t), while the others offered discounts due to slow lifting of material.

Trade-level BF rebar prices dropped by INR 500/tonne (t) ($6/t) w-o-w to INR 47,900/t ($548/t) exy-Mumbai, as per BigMint’s assessment on 22 August 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices fell w-o-w to INR 46,500-47,500/t ($532-543/t) FOR Mumbai amid need-based procurement due to heavy rains in major parts of the country. Logistics bottlenecks also emerged, impacting the supply chain.

Rebar inventories with primary mills dropped slightly to 4.75-4.8 lakh t in end-Aug 2025, as per market sources.

Update on projects

- DBL-RBL JV received an INR 1,503.63 crore letter of acceptance (LOA) from the Gurugram Metro Rail Limited (GMRL) for constructing 27 stations and viaducts on the Gurugram Metro Corridor, with project completion slated in 30 months.

- Dilip Buildcon Limited, through the DBL-Ramky consortium, emerged as the L-1 bidder for the Rajasthan Water Grid Project worth INR 2,952 crore under a Hybrid Annuity Model, with a 27-month completion timeline.

- KEC International Limited secured new orders worth INR 1,402 crore across businesses such as Transmission and Distribution (T&D), high-rise residential projects, and orders for the supply of various types of cables and conductors in India and the overseas market.

- Rail Vikas Nigam Limited (RVNL) received an LOA from IRCON International for signalling, telecom, and interlocking works across 10 new stations, six Intermediate Block Signalling (IBS) systems, and the Gevra-Pendra section, enhancing railway infrastructure.

Factors behind market dynamics

1. IF rebar prices edge down w-o-w: Induction furnace (IF) rebar prices witnessed a marginal drop this week across key Indian markets. Trade prices dropped w-o-w across major markets amid need-based buying due to the effect of the monsoon. Manufacturers reduced their list prices and offered discounts to release material. Inventory levels ranged within 10-12 days across regions. IF rebar prices edged down by INR 100/t ($1/t) w-o-w to INR 45,700/t ($523/t) exw-Mumbai as on 22 August 2025.

The BF-IF rebar price gap narrowed w-o-w to around INR 2,000-2,500/t ($23-29/t) in Mumbai. IF rebars hold a dominant 65-70% market share in India.

2. Raw material prices show mixed trends w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,500/t ($63/t) ex-mines on 16 August 2025. Iron ore prices in Odisha remained firm this week, with trades concluded largely on an as-needed basis by steelmakers. Market participants attributed the price stability to limited production and sustained inquiries from buyers, even as material scarcity continued due to persistent rainfall and disruptions in rake movement.

Australian premium hard coking coal (PHCC) prices rose by $3/t w-o-w to $202/t CNF Paradip.

Outlook

BF-rebar trade prices are likely to face further downward pressure in the coming days, driven by sluggish demand during the ongoing monsoon season.

Leave a Reply