- Adani Enterprises’ new copper smelter applies for LME listing

- Antofagasta’s stronger output boosts global supply reliability

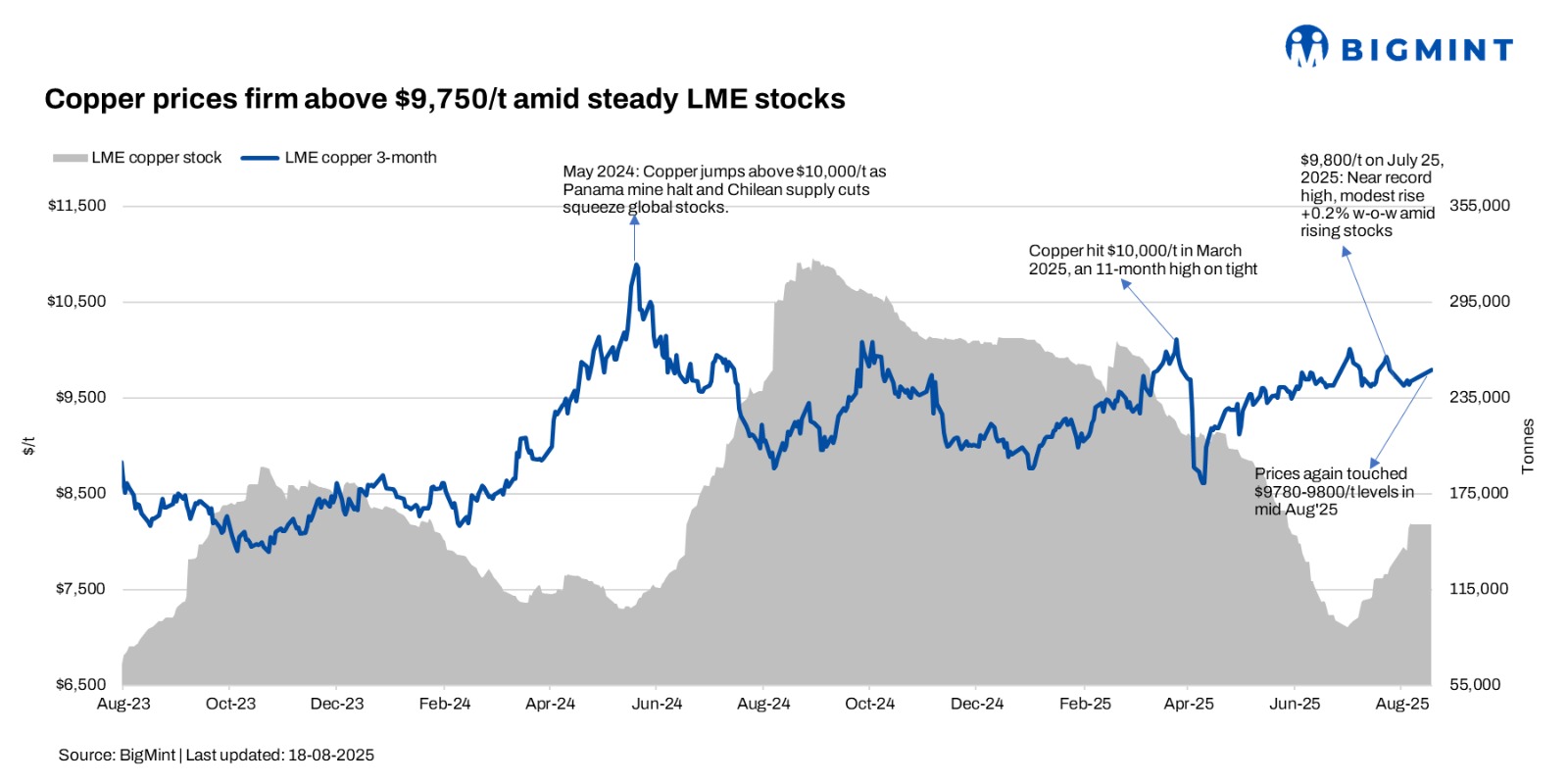

Copper prices on the London Metal Exchange (LME) edged slightly higher w-o-w, with the 3-month contract closing at $9,780/tonne (t) on 15 August 2025, from $9,720/t on 11 August 2025. Supporting these prices is a notable stabilisation in LME copper stocks, which remained largely unchanged throughout the same period. Inventories were at 155,700 t on 11 August and 155,800 t by 15 August, hinting at steady physical market conditions.

On the supply front, Adani Enterprises’ new 500,000-t Kutch Copper smelter in India is preparing to enter the market and has applied to become an LME-listed brand. While the smelter is expected to reduce India’s reliance on imports in the medium term, its ramp-up phase means the global market is not yet experiencing a flood of new refined copper.

Meanwhile, in Latin America, Antofagasta’s stronger output has added confidence in supply reliability, with the company reporting a 17% rise in copper sales volumes in H1CY’25. Yet, much of this increase has already been absorbed by steady demand from Asia, particularly China, where infrastructure and manufacturing stimulus continue to support copper consumption.

Glencore’s Mount Isa copper smelter, with a capacity of roughly 300,000 t per year, is under severe pressure. It is deemed economically unviable due to crashing global smelting charges – driven by subsidised capacities in China and Indonesia – and elevated operating costs. Closure discussions and appeals for governmental support add an element of supply uncertainty in the medium term.

State-owned mining giant Codelco posted a substantial 17% y-o-y increase in copper output for June 2025, reaching 120,200 t. This uptick was driven in part by the partial resumption of operations at the El Teniente mine following a fatal incident earlier in the month.

Outlook

LME copper prices are expected to stay supported in the near term, with forecasts of around $9,100-9,350/t in H2CY’25, underpinned by still-tight physical availability and low inventories that recently recovered only modestly to around 108,700 t from a two-year low of ~105,000 t. JP Morgan projects softer levels as trade policy risks, including US tariff measures, weigh on sentiment. Overall, the combination of constrained stock levels and macro uncertainty suggests copper will remain range-bound, with short-term strength tempered by policy and demand headwinds.

Leave a Reply