- Finished flat exports edge up 2%, billets surge

- Declining prices boosts offtake by EU buyers

- Steel exports decline by 20% y-o-y in 7MCY’25

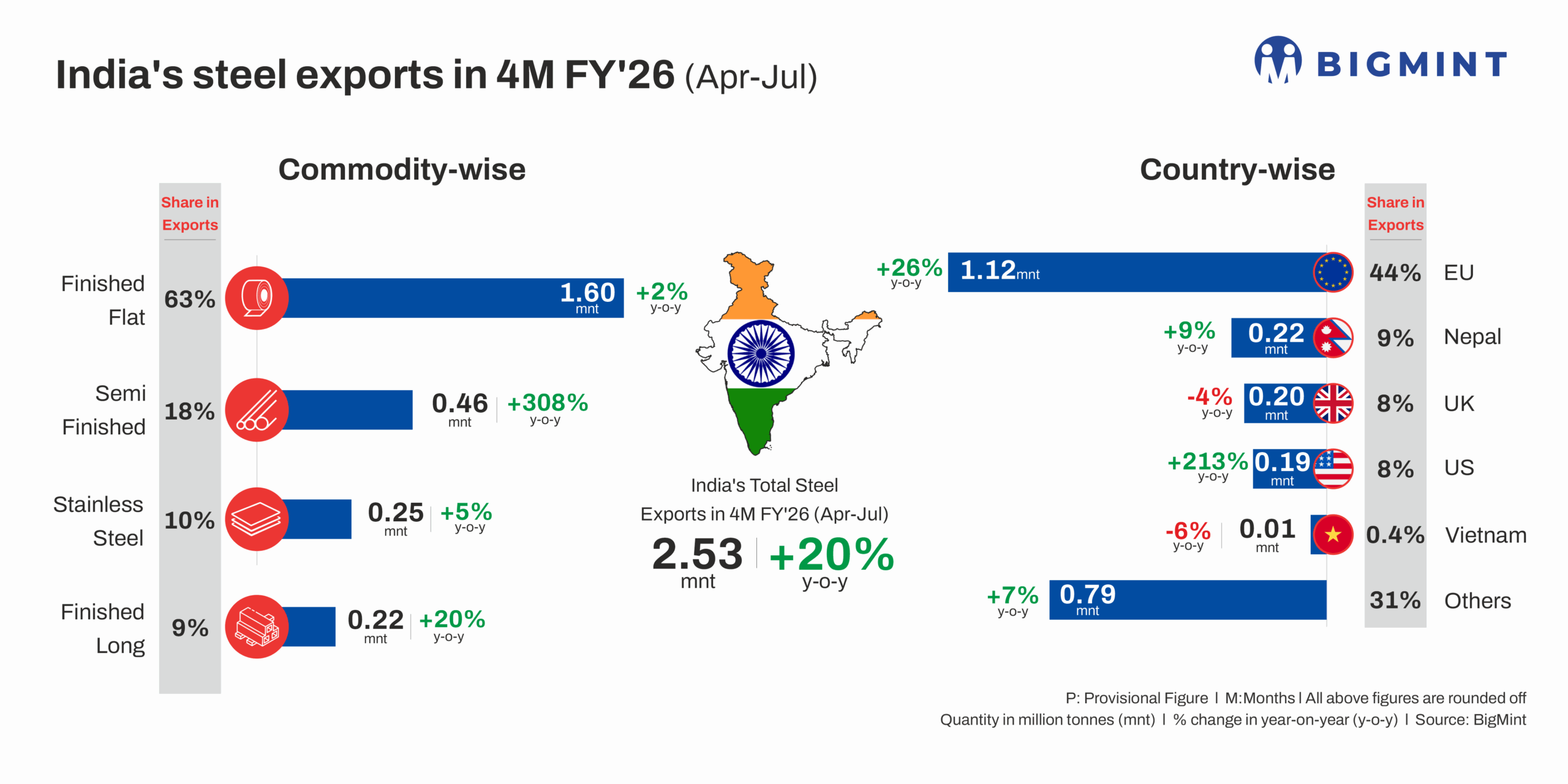

Morning Brief: India steel exports (including stainless steel) grew 20% y-o-y in the first four months of FY’26 (4MFY’26) to 2.53 million tonnes (mnt), as per data compiled by BigMint. This provides concrete signals of a recovery in India’s export momentum, which has been lagging in recent times due to mounting shipments from China, weakening global steel consumption, and unbeatable pricing from competitors.

Country-wise exports

The EU, India’s largest market, witnessed a 26% y-o-y surge in volumes to 1.12 mnt in 4MFY’26. This was precipitated by higher intake of hot-rolled coils (HRCs)/plates (+34%), cold-rolled coils (+68%), and pipes and tubes (29%).

Nepal followed with a 9% uptick to 0.22 mnt, with volumes bolstered by a significant increase in imports of galvanised steel and wire rods.

Exports to Turkiye, although on a small scale, nearly quadrupled to around 72,000 tonnes (t). Turkiye procured substantial shipments of billets from India this year against nil in 4MFY’25.

The growth in these regions was offset, to a certain degree, by a 79% drop in overall volumes to Saudi Arabia. Pipes and tubes exports to Saudi Arabia plummeted by a massive 90% in 4MFY’26.

Commodity-wise exports

Finished flats (carbon steel) exports edged up by 2% y-o-y to 1.60 mnt, largely due to a considerable 56% rise in CRC shipments to 259,000. Pipes and tubes witnessed a moderate 7% increase to 505,000 t, with the UAE, US, and EU seeing major hikes.

Pipes and tubes exports surpassed HRC/plate shipments, with the latter falling 8% to 457,000 t. HRC/plate exports to the EU increased 34%, but this came at the expense of near nil shipments to the UK. Exports to Nepal declined by 7% and to the UAE by 16%.

Meanwhile, galvanised steel exports eroded by 12%.

Semi-finished shipments quadrupled to 0.46 mnt because of increased procurement by the UK and Turkiye, among others.

Finished longs exports climbed up by 20% y-o-y to 0.22 mnt and stainless steel by 5% to 0.25 mnt in 4MFY’26.

Competitive pricing drives higher procurement by EU

Despite reports of weak demand and cautious sentiment in the market, EU buyers likely ramped up their purchases from India due to a decline in prices.

HRC export offers to the EU resumed in March, after India was exempted from the provisional anti-dumping duties. While offers increased in March and April (averaging around $590/t FOB main port, India and $640/t CFR Antwerp), they fell in June ($565/t FOB, $615/t CFR) and July ($541/t FOB, $591/t CFR). At the same time, offers from domestic mills were slightly higher, amid elevated energy costs, which kept production costs on the upper side.

The competitive pricing could have contributed to opportunistic purchases by EU importers.

Exports drop 20% in 7MCY’25

However, a shadow still persists if CY’25 volumes are considered. Exports in 7MCY’25 amounted to 4.3 mnt compared to 5.3 mnt in the year-ago period, a sharp reduction of 19%. During 7MCY’25, Indian exporters intermittently offered material such as hot-rolled coils (HRCs) in key international markets (the EU and the Middle East, for example) due to subdued demand from the region. Consequently, finished flat exports plunged by 33% y-o-y to 2.8 mnt. This led to a fading presence in the global seaborne landscape.

Outlook

India’s export momentum seems to be under threat, even though recent data suggests a moderate rebound. Chinese steel exports keep rising, despite expectations of a moderation. Additionally, Indonesia and Saudi Arabia are proving to be mighty competitors due to their attractive pricing. This is likely to constrict India’s growth.

While exports to the EU picked up recently, headwinds continue, with the ongoing summer holidays expected to weigh on trade. Cautious buying may continue amid regulatory uncertainty.

India’s steel industry is also on tenterhooks due to the CBAM, set to be fully operational by 2026. However, the upside is that given EU-based mills are grappling with elevated power costs and carbon prices, the CBAM could make Indian steelmakers better positioned to export low-emissions steel to the EU in the short-to-mid-term.

Additionally, in mid-August, Indian mills resumed HRC export offers to the Middle East, due to a sharp rise in Chinese prices to $515/t CFR UAE. This might lead to a pick-up in volumes, though currently, demand seems tepid due to the ongoing summer.

Leave a Reply