- Asia-Pacific Panamax freights rise on surge in fixing

- Monsoon impacts port operations, cargo handling

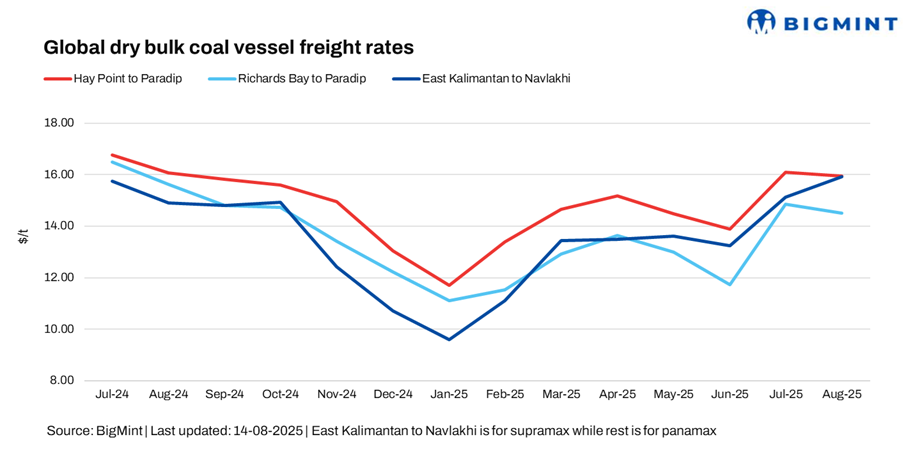

Dry bulk coal freights to India rose w-o-w, with Panamax rates gaining on the Australia and South Africa routes, while Supramax rates on the Indonesia-India corridor remained firm.

Coal demand from operators in the Pacific remained decent, and minimal fresh cargoes entered the market. Only a few shipments were cleared overnight, resulting in softer requirements. Trading activity during Asian hours was overall sluggish, sources told BigMint.

Additionally, persistent rainfall across parts of India continued to dampen thermal coal demand, leading to slower vessel booking activity. Most market participants stayed on the sidelines, waiting for a correction in offers.

Portside thermal coal inventories in India dropped by 4% w-o-w to 13.70 million tonnes (mnt) in week 32 of 2025, from 14.27 mnt the previous week. The drop was led by lower vessel discharge at major eastern and western ports, though a few southern and eastern ports recorded moderate gains on better handling.

“Asia-Pacific Panamax freight rates edged higher this week following a surge in fixing, with freight derivatives gaining during Asian trading hours and bunker prices posting a slight d-o-d increase,” a source informed BigMint.

Another source said, “A burst of short-term interest drove paper prices up, with September posting the sharpest rise. The forward curve remained in backwardation, as gains in distant contracts were fuelled more by optimism than by tangible increases in physical activity.”

However, both charterers and shipowners remained firm on their positions, with neither side willing to concede. This kept the bid-offer spread wide, hindering trade execution for most of the Asian trading session.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India increased by $0.1/dry metric tonne (dmt) w-o-w, with BigMint’s latest assessment placing the Hay Point-Paradip route at $16/dmt. Monsoon rains continued to impact several regions of India, disrupting port operations, delaying cargo handling, and tightening vessel turnaround times. The weather-related interruptions led to congestion at select ports, limited loading/discharging windows, and affected freights – particularly for coastal movements. Indian market sentiment was also weighed down by a festive-week slowdown in trade channels, sources informed.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route dropped by $1/dmt w-o-w to $15/dmt. This week’s increase was fueled by the clearance of backlogged vessels at RBCT as congestion eased, coupled with higher nominations from Indian buyers, specailly sponge iron players as prices remained supportive throuhout the week and a few Atlantic-bound cargoes.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route rose by $0.03/dmt w-o-w to $15.93/dmt. However, shipments in this period were dampened by subdued demand from key buyers, China and India.

Market highlights

- Baltic dry bulk index exhibits mixed trend w-o-w: The Baltic Exchange’s main dry bulk sea freight index for Panamax vessels came under pressure, even as demand stayed decent across the segment, with smaller vessels bucking the trend. The Panamax index decreased by 65 points w-o-w to 1,594. However, the Supramax index increased significantly by 68 points w-o-w to 1,336.

- DCE coking coal futures increase w-o-w: Coking coal futures on the Dalian Commodity Exchange (DCE) increased by RMB 4/t ($1/t) w-o-w to RMB 138/t ($19/t) on 14 August 2025. DCE coking coal futures rose on supply concerns triggered by upcoming government inspections of coal mines across major producing provinces, which fuelled fears of production curbs. Market sentiment was further supported by policy signals on capacity cuts, temporary output halts in Shanxi for environmental checks, and a sharp drawdown in mine and plant inventories. Strong restocking demand from coke producers and robust pig iron output added to the upward momentum.

Outlook

In the near term, dry bulk coal freight rates are expected to either remain rangebound or soften a bit, as muted Asian demand and ample vessel availability weigh on market momentum. While South Africa may sustain export flows on firm Atlantic demand and improved logistics, Australia and Indonesia could face headwinds from weak buying interest and port delays.

At the same time, declining restocking at Indian ports may lend some support, but high domestic output in China and India is likely to cap import volumes, keeping freight upside in check.

Leave a Reply