- Global iron ore exports plunge to over 1-month low

- Chinese buying slows amid compressed steel margins

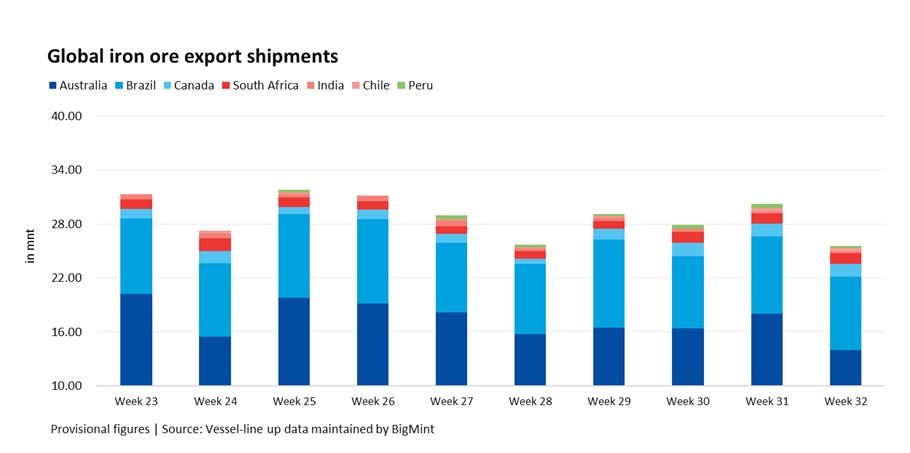

Global seaborne iron ore and pellet exports fell sharply by 15.6% w-o-w in Week 32, 2025 (2-8 August) to over a one-month low of 25.54 million tonnes (mnt) from 30.25 mnt in Week 31, according to vessel line-up data from BigMint.

The drop was led by a sharp contraction in shipments from Australia, alongside softer flows from Brazil, Canada, Chile, and Peru, even as South Africa and India recorded moderate gains. The decline came amid subdued Chinese buying, with most mills avoiding large-scale restocking given compressed steel margins and limited visibility on downstream demand.

Australia’s iron ore exports fell 22.4% to 13.99 mnt in Week 32 from 18.02 mnt in the previous week, marking the sharpest w-o-w decline.

All major miners witnessed reduced loadings, with Rio Tinto shipping 5.67 mnt, BHP 5.20 mnt, and Fortescue Metals Group (FMG) 2.74 mnt. China remained the dominant destination, taking 11.89 mnt, followed by Japan at 0.96 mnt and South Korea at 0.63 mnt.

Market participants pointed to weaker global steel demand, reduced steel output in China, and increased competition from Brazilian and African suppliers as key factors behind the slowdown in Chinese intake of Australian ore.

Brazil’s iron ore exports slipped 5.4% w-o-w to 8.17 mnt in Week 32 from 8.63 mnt. Intermittent rain and congestion at Tubarao Port slowed loadings, weighing on exports.

According to data maintained with BigMint, Brazil exported 41.1 mnt of iron ore (including pellets) in July 2025, surpassing the previous monthly record of 39.65 mnt set in December 2023. This milestone underscores Brazil’s position as the world’s second-largest iron ore exporter after Australia and reflects significant shifts in the global market.

Chinese mills remained the largest buyers, taking 3.90 mnt in Week 32, although their intake eased compared to the previous week due to earlier restocking activity.

Canada’s iron ore exports edged down by 2.8% w-o-w in Week 32 to 1.38 mnt from 1.42 mnt. Shipments from Sept-Iles totalled 0.78 mnt and from Milne Inlet 0.47 mnt, with both ports operating smoothly. However, vessel scheduling gaps resulted in some idle time between loadings, slightly slowing export movement.

This week, Belgium was the leading importer with 0.48 mnt, followed by Italy and the US with 0.18 mnt each.

The Iron Ore Company of Canada (IOC) contributed 0.52 mnt, continuing steady deliveries of premium DR-grade ore, which is attracting niche demand from steelmakers aiming to lower carbon emissions in their production processes.

South Africa’s iron ore exports rose 8.85% w-o-w in Week 32 to 1.23 mnt from 1.13 mnt, as improved berth availability at Saldanha Bay (1.02 mnt) helped clear earlier congestion, while Richards Bay contributed a smaller volume (0.21 mnt).

Exporters took advantage of the operational improvement to move backlogged cargoes into the market. China remained the largest buyer, importing 0.45 mnt — more than half of South Africa’s total — supported by stable freights and competitive landed prices.

India’s iron ore exports rose modestly by 9.5% w-o-w to 0.23 mnt in Week 32 from 0.21 mnt, driven mainly by opportunistic sales of low-grade Fe 57-58% fines, especially from eastern ports, to Chinese traders seeking to blend them with higher-grade Australian material.

However, overall exports stayed low because global prices were weak, and a lot of India’s production was being used inside the country instead of being shipped abroad.

Chile’s exports stood at 0.31 mnt in Week 32, down 20.5% from 0.39 mnt in the previous week, as loading activity at northern ports slowed following a brief surge in shipments last week.

Peru’s exports halved to 0.22 mnt in Week 32 from 0.44 mnt in the previous week, as production in the Marcona region slowed and vessel nominations for Asian buyers declined.

Dry bulk iron ore freights dip w-o-w on limited fixtures

Iron ore dry bulk freights softened across most routes, as fixture activity remained limited and sentiment was weak. Subdued activity was seen across major routes such as Australia-China and Brazil-China. However, overall market sentiment remained weak amid continued steel production cuts, macroeconomic pressures, and cautious procurement behaviour.

Outlook

In the near term, iron ore exports are expected to stay subdued as Chinese mills continue cautious, hand-to-mouth buying amid weak steel margins and uncertain downstream demand. Australian volumes may recover slightly once weather and maintenance disruptions ease, while Brazil’s record output faces logistical constraints.

Leave a Reply