- Chinese stocks rise amid off-season for consumption

- Nyrstar secures AUD 135 million to sustain smelters

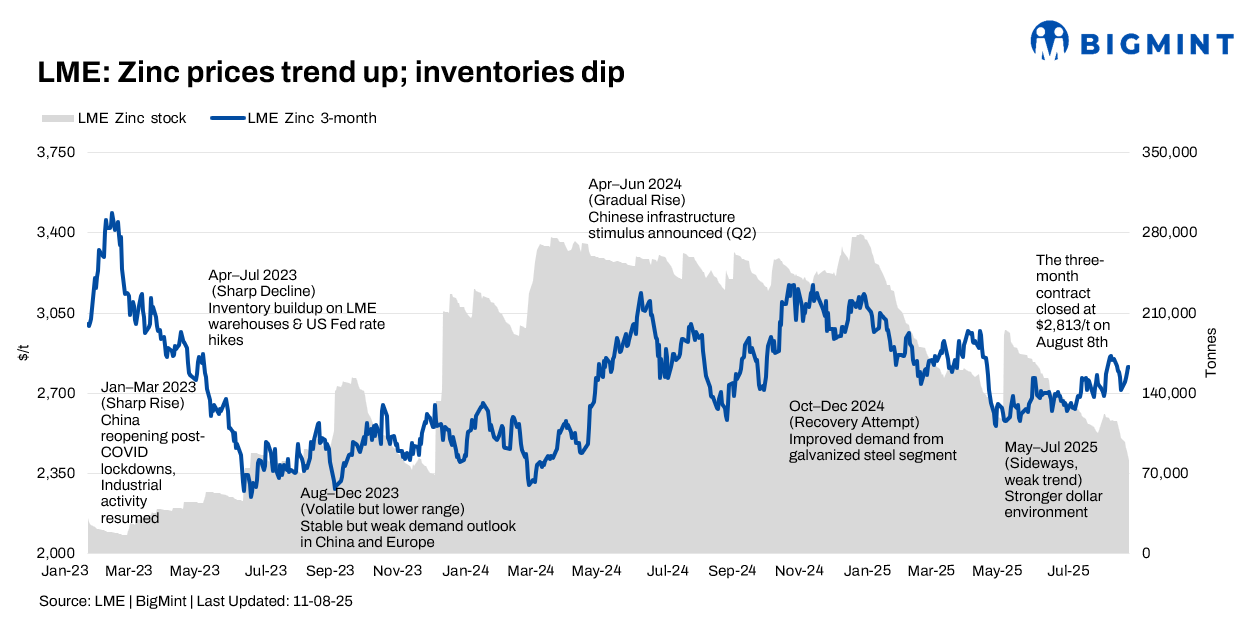

London Metal Exchange (LME) zinc prices saw an uptrend during Week 31 (4-8 August 2025), largely supported by decreasing inventories and positive macroeconomic signals from the US. However, this bullish momentum was counterbalanced by concerns about oversupply, particularly in China, and potential shifts in global trade policies.

Prices, trends

LME zinc cash-settlement prices opened the week on 4 August at $2,736.00/t and closed higher on 8 August at $2,811.00/t, marking an approximate increase of 2.74%. The three-month LME zinc contract mirrored this upward trend, closing at $2,813.50/t on 8 August against $2,749.50/t on 4 August. Prices were buoyed by optimism surrounding potential US interest rate cuts and a generally improved macro sentiment.

LME zinc inventories saw a decrease during the week. On 8 August, inventories fell to 81,500 t, a significant decrease of 3,450 t from the previous day, and a substantial drop from the 97,000 t recorded on 4 August. This decline signals tightening supply in the immediate term and could be a factor in supporting LME zinc prices.

Conversely, domestic Chinese inventories continued to increase. As of 7 August, total zinc ingot inventories across seven locations in China reached 113,200 t, an increase of 5,900 t from 4 August and 10,000 t on a w-o-w basis. This rise suggests weak domestic demand within China, possibly exacerbated by high prices and an off-season for consumption, according to Shanghai Metals Market.

MCX zinc trends

MCX zinc prices fluctuated during the week, initially experiencing a decline before rebounding. Prices declined by 1.34% to settle at INR 262,000/t on 4 August, driven by demand concerns. However, prices rebounded to 268,200/t on 7 August, supported by tightening supply conditions and a softer US dollar. Prices edged up again to settle at 268,500/t on 8 August, further bolstered by tightening supply and news of Chinese smelters cutting output. The contract was trading with a positive bias, suggesting a cautiously optimistic sentiment despite demand worries.

Nyrstar secures AUD 135 million to sustain, upgrade smelter operations

On 5 August, Nyrstar announced AUD 135 million in transitional funding from the Australian federal, South Australian, and Tasmanian governments to support its Port Pirie and Hobart smelters. The package, alongside Trafigura’s investment, will maintain operations, advance critical metals projects, and fund major upgrades, including furnace and wharf improvements.

Priority initiatives include an antimony pilot plant in Port Pirie and research into germanium, indium, and bismuth production. As Australia’s only lead refiner and largest zinc smelter, Nyrstar contributes AUD 1.7 billion annually, supporting over 8,000 jobs. Zinc output in Hobart remains 25% lower since April 2025, with no restart date confirmed.

Outlook

The outlook for zinc remains cautiously optimistic. While LME prices are finding support from declining inventories and positive global macro signals, the persistent oversupply concerns and weak Chinese demand could temper further gains. Regional demand dynamics and the SHFE/LME ratio will continue to influence market direction and sentiment in the coming weeks.

Leave a Reply