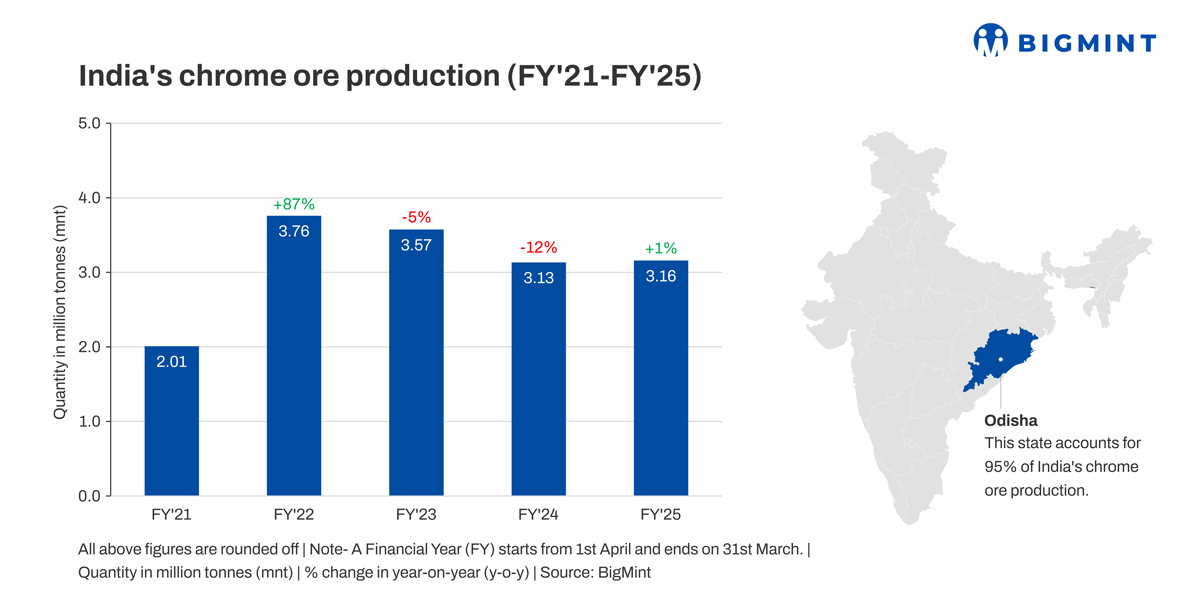

- India’s chrome ore production edges up by 1% y-o-y

- OMC’s output up 3%, Tata Steel sees sharp 39% drop

India’s chrome ore production increased slightly by 1% y-o-y to 3.16 mnt in FY’25 as against 3.13 mnt in FY’24. India has approximately 344 mnt of chrome ore reserves, mainly located in the Sukinda Valley of Odisha.

Miner-wise production trends

OMC retains leadership: Odisha Mining Corporation (OMC) remained India’s top chrome ore producer, contributing 43% of total output in FY’25. Production rose 3% y-o-y to 1.35 mnt from 1.31 mnt in FY’24, driven mainly by ramp-ups at existing mines. OMC has set a target of 1.5 mnt for FY’26 to cater to rising demand in the finished market.

As the largest chrome ore seller, OMC conducts monthly e-auctions for various grades. However, the average monthly auction volume declined to 64,750 t in FY’25 from 72,642 t in FY’24. Demand from domestic ferro chrome producers, who are heavily reliant on these auctions, remained strong, even though bid prices fluctuated through the year.

Tata Steel’s production drops: Tata Steel recorded a steep 39% y-o-y fall in chrome ore output, producing 0.58 mnt in FY’25 compared to 0.96 mnt in FY’24. The decline stemmed mainly from reduced volumes at its Sukinda mines.

IMFA, FACOR see growth: Indian Metals and Ferro Alloys Ltd. (IMFA) and Ferro Alloys Corporation Ltd. (FACOR) both posted an 8% y-o-y increase. FACOR’s output inched up to 0.18 mnt from 0.17 mnt, while IMFA’s rose to 0.71 mnt from 0.65 mnt. IMFA sources ore entirely from its Sukinda and Mahagiri mines for in-house smelting.

Grade-wise production dynamics

The 40-52% grade chrome ore dominated FY’25 output, surging 23% y-o-y to 1.90 mnt from 1.55 mnt in FY’24. In contrast, high-grade ore (above 52%) plunged 60% y-o-y to 0.27 mnt from 0.67 mnt, mainly due to limited availability and underground mining challenges.

Finished market overview

India’s ferro chrome production edged down slightly by 1% to 1.35 mnt in FY’25 from 1.36 mnt in FY’24. The year saw mixed performance, shaped by volatility in raw material prices, shifts in export demand, and prevailing market dynamics in the stainless steel segment.

Stainless steel output, however, grew 14% y-o-y to 3.85 mnt from 3.38 mnt, supported by higher imports of semi-finished inputs such as SS 300 series slabs, billets, and nickel pig iron (NPI). These inflows reduced dependence on scrap and ferro chrome. Additionally, increased imports of finished stainless steel products weighed on domestic raw material consumption, curbing ferro chrome capacity utilisation.

Outlook

Chrome ore miners in Odisha are actively pursuing output growth through new mines, lease extensions, and the adoption of advanced mechanised and digital mining systems for improved efficiency and safety. Many are integrating mining with processing, smelting, and beneficiation to enhance value addition.

Environmental sustainability is another priority, with investments in effluent treatment plants and eco-friendly mining practices. Miners are also working closely with policy and tender frameworks to ensure consistent supply to downstream industries.

Gain valuable perspectives from industry experts at the 5th International Ferro Alloys Conference 2025, scheduled for 2-4 September at JW Marriott, New Delhi. Featuring a “Stainless Steel & Ferro Chrome – Deep Dive” session, the conference is set to explore emerging trends and the future outlook for various ferro alloy markets.

Leave a Reply