- Domestic coke prices may rise in short term

- Coking coal, Chinese met coke prices rise w-o-w

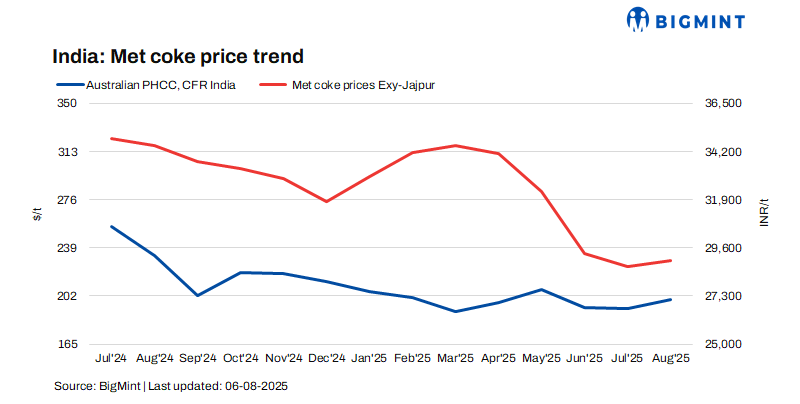

India’s metallurgical coke (met coke) market witnessed marginal price movement in the week ended 6 August 2025, with improved trading activity offering price support across key trading hubs. The market outlook remains cautiously optimistic, backed by rising raw material costs and Chinese met coke price hikes.

Prices steady amid tight supply and import delays

In eastern India, met coke prices remained unchanged week-on-week (w-o-w). BigMint assessed BF-grade (25-90 mm) met coke at INR 29,000/tonne (ex-Jajpur). In western India, prices saw a minor uptick of INR 200/t, with ex-works Gandhidham prices recorded at INR 30,000/t.

Improved buying interest supported pricing stability. Merchant cokeries in India are gradually liquidating inventories, while fresh import shipments are not expected before September, keeping domestic prices supported.

Multiple factors supporting prices

Several factors are contributing to a potential upward movement in met coke prices:

- High coking coal costs: Elevated prices for imported coking coal continue to exert cost pressure on coke producers. In the seaborne market, Australian premium hard coking coal (PHCC) prices increased by $6/t w-o-w, reaching $183/t FOB. The uptick reflects continued firm demand from Asian buyers and tight vessel availability, keeping procurement costs elevated for Indian buyers reliant on imports.

- Chinese met coke market maintains uptrend – China’s met coke market remained firm following the fifth round of domestic price hikes. Prices across key regions stayed stable, with Rizhao FOB prices rising RMB 50/t to RMB 1,370/t. Coking plants in Shanxi, Shaanxi, and Inner Mongolia continued to operate at 70-80% capacity, with low inventories and strong steel mill demand providing support. However, upside potential is capped due to thin profit margins and anticipated production curbs in northern China ahead of the military parade in early September. Such environmental measures could restrict coke supply while simultaneously affecting downstream construction activity and near-term demand.

- Exchange rate volatility: A weaker rupee is pushing up the cost of dollar-denominated imports, including coal and coke. INR is trading at 87.7 against $ versus 85.7 levels seen in early Jul’25.

- Pig iron prices almost rangebound: A recovery in downstream steel markets is also supporting met coke sentiment. BigMint assessed steel-grade pig iron prices at INR 32,700/t ex-Durgapur, down by INR 150/t w-o-w.

Outlook: Cautiously bullish

Industry sources indicated that company-wise met coke import quotas have been allotted towards the end of last week. However, import arrivals will come by September and so domestic prices are expected to firm up in the short term.

Leave a Reply