- Monsoon hinders progress of infrastructure projects

- Market subdued amid BIS certification issues

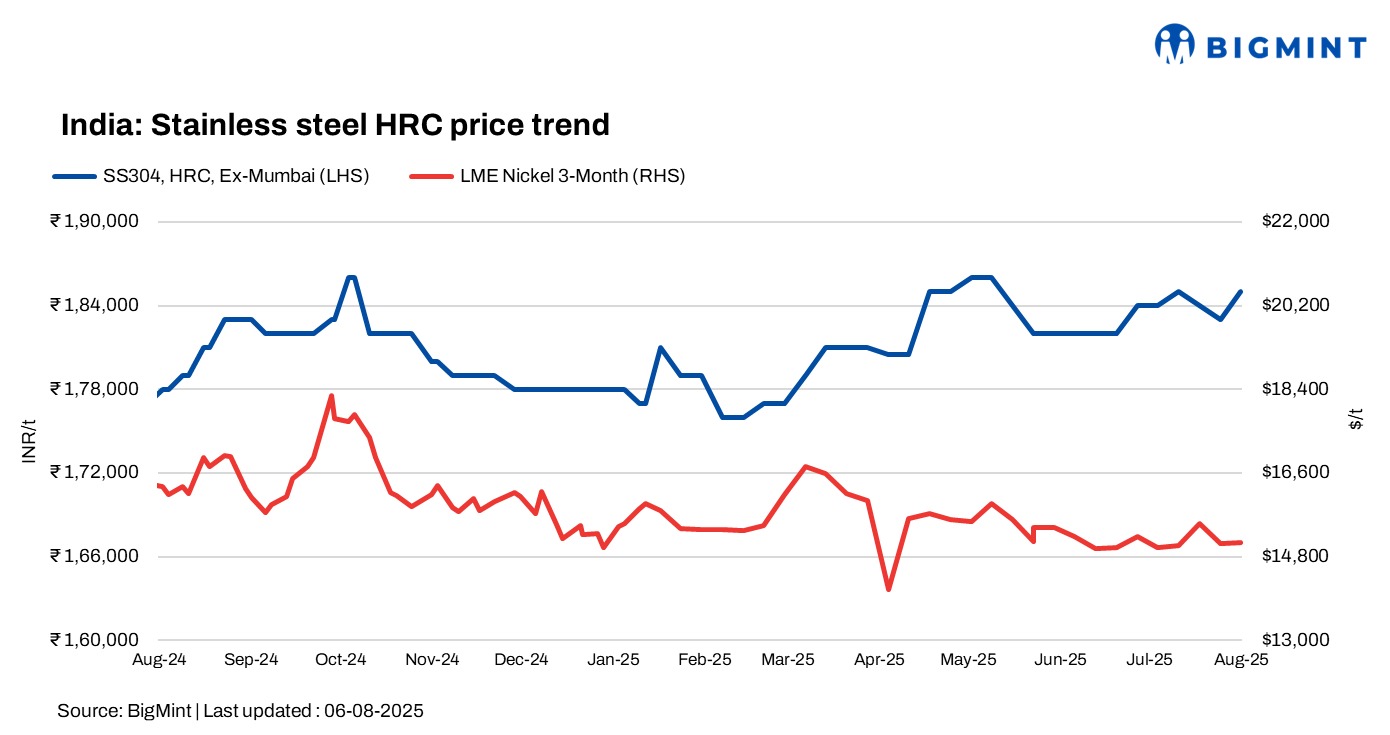

India’s stainless steel market witnessed fluctuations this week, with finished flats showing mixed price movements and longs remaining range-bound w-o-w, amid limited trading activity.

BigMint’s benchmark assessment for 304-series hot-rolled coils (HRCs) dropped marginally by INR 2,000/tonne (t) w-o-w to INR 185,000/t ex-Mumbai. Meanwhile, 304L black round bars (25-100 mm) was assessed at INR 155,000/t, down by INR 2,000/t w-o-w amid weak buying activity.

BigMint’s assessment for SS 316 HRCs stood at INR 332,000/t and for 316 cold-rolled coils (CRCs) at INR 335,000/t ex-Mumbai, up INR 2,000 /t w-o-w.

Market updates

India’s stainless steel market sentiment remains largely subdued with no notable improvement, as participants remain cautious amid the recently notified BIS certification requirements for imports and ongoing volatility in LME nickel prices.

Mills are waiting for monsoon ending and the arrival of the festive season to for domestic demand to pick up.

Expectations of a US Federal Reserve rate cut in September are based on weaker employment data, while China’s continued and expanded infrastructure stimulus has boosted regional sentiment slightly.

The strengthening of China’s stainless steel market has contributed to a continued uptick in LME nickel prices; however, persistently weak domestic demand in China points to potential short-term volatility for nickel. Indian market sources said that monsoon rains have delayed infrastructure projects, hindering a meaningful recovery in steel consumption.

Indicative FOB prices for stainless steel longs remain steady, with India’s 304 bright bars at $2,050–2,100/t and 316 bright bars at $3,300–3,600/t, while Vietnam’s 304 bright bars are quoted at $1,940–1,990/t and 316 bright bars at $3,440–3,490/t.

LME nickel range-bound, Asian NPI flat

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,100/t, range-bound w-o-w. Nickel stocks at LME-registered warehouses stood at 211,254 t, up 3% w-o-w compared to 204,912 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) remained firm w-o-w at RMB 917/t ($128/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $109/t, steady w-o-w.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,450/t ($1,873/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were firm at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices stayed largely rangebound last week, going down slightly by INR 35,000/t ($399/t) as compared to the assessment on 30 July. Tight supplies in the domestic market along with good demand largely kept the prices supported.

Ferro molybdenum prices in India were INR 2,945,000/t ($33,588/t) exw-India, as per BigMint’s assessment on 6 August. Approximately 15 t of deals were reported to BigMint last week in the price range of INR 2,900,000-3,016,000/t ($33,074-34,397/t) exw.

Ferro Silicon: Indian ferro silicon (70%) prices experienced a drop of INR 2,400/t ($27/t) on 4 August in comparison with the assessment on 28 July. Prices moved down following Bhutan’s price announcement of INR 95,000/t ($1,082/t) exw for this month and resumption of operations of plants in Meghalaya.

Ferro silicon prices in India were INR 95,000/t ($1,082/t) exw-Guwahati, as per BigMints assessment on 4 July. In Bhutan, prices came down by INR 3,400/t ($39/t) w-o-w to INR 95,000/t ($1,082/t) exw. Around 650 t of deals were reported in both the regions last week within the range INR 95,000-98,000/t ($1,082-1,116/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,500/t ($1,145/t) exw-Jajpur, range-bound w-o-w.

Ferrous scrap: India’s imported scrap market stayed subdued w-o-w, with limited buying interest and muted trade activity. European-origin shredded was heard workable at around $365/t, while no firm offers were reported for US-origin shredded.

Australian HMS 80:20 was heard at $335-340/t CFR. Market participants described sentiment as “quite ok,” with hopes of improved activity ahead of the pre-festive demand period. However, prices eased after a brief uptrend in recent days as the US Dollar strengthened, and no deals were reported at higher levels.

Outlook

Market participants remain cautious due to elevated raw material costs and volatile LME prices. However, finished stainless steel demand is anticipated to improve following the end of monsoons and the arrival of the festive season, potentially supporting a more positive market trend in the coming months.

Leave a Reply