- Sponge iron prices remain stable d-o-d

- Finished steel prices gain INR 200/t d-o-d

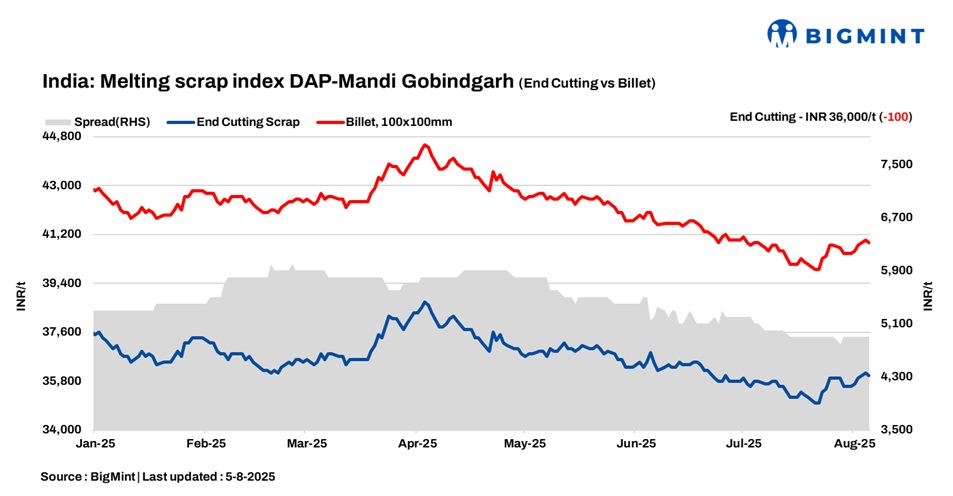

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 100/tonne (t) d-o-d to INR 36,000/t DAP on 5 August 2025. Steel scrap prices in the region saw a marginal decline of INR 100-200/t, with buyers maintaining moderate procurement levels. Recent monsoon rains have slowed scrap arrivals in several states, leading to a mild shortage in the market. Despite this, the overall shortage remains limited.

A mill owner informed, “The market is expected to remain stable, with only minor fluctuations anticipated. Mills are optimistic, hoping that Mandi Gobindgarh ingot prices will continue to hold steady in the INR 40,700-41,300/t range, supported by moderate demand. After the monsoon, demand is expected to pick up.”

Raw materials

Sponge iron (CDRI) prices in Mandi Gobindgarh held steady on 5 August, maintaining their level at INR 30,300/t DAP, reflecting a stable trend in the region’s raw material segment. Similarly, pig iron prices in Ludhiana (Punjab) showed no movement, staying firm at INR 35,800/t DAP. Overall, market sentiment remained moderate today.

Steel market trend

The semi-finished steel market in Mandi Gobindgarh saw a slight decline, with prices slipping by INR 100/t on a d-o-d basis to close at INR 40,900/t DAP. Major steel hubs across the country echoed this trend, with prices softening by INR 50–200/t as the market remained largely rangebound. Raigarh stood out with a pronounced drop of INR 250/t, attributed to subdued buying interest today.

In contrast, rebar (Fe 500) prices in Mandi Gobindgarh posted an uptick of INR 200/t, climbing to INR 46,000/t ex-works. Meanwhile, ERW pipes (patra-based) recorded a dip of INR 100/t d-o-d, now assessed at INR 44,300/t ex-works.

Overall, the finished steel segment experienced mixed demand, with minor fluctuations of INR 100-200/t seen across categories. These movements reflect the ongoing uncertainty and cautious sentiment prevailing in the steel market.

Overview of Jalna market

In the Jalna market of western India, billet, rebar, and HMS 80:20 prices remained stable, assessed at INR 40,500/t, INR 44,400/t, and INR 31,200/t respectively. Market participants report a recent improvement in finished steel demand, contributing to a positive w-o-w price trend. Moreover, mills have witnessed a better flow of raw materials, aided by the recent upward correction in prices, which has enhanced procurement confidence.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $335-$338/t, which equates to approximately INR 31,884/t (including freight). HMS (80:20) prices in Mumbai fell by INR 100/t to INR 31,400/t DAP today. Indicative prices of shredded from Europe stood at $365-$368/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,050/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply