- Raw material prices see upward momentum

- India’s rebar output in Q1FY’26 up 11% y-o-y

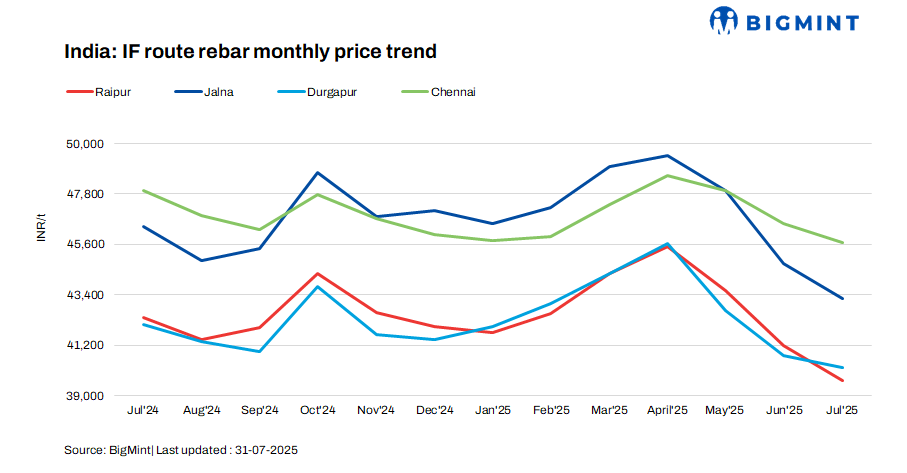

India’s induction furnace (IF) rebar prices witnessed mixed movements in July 2025, varying by INR 100-1,900/tonne (t) m-o-m across regions, as per BigMint’s assessment. The fluctuation was primarily driven by improved demand and support from raw material prices.

The most significant price rise was recorded in the western region, an increase of INR 1,300/t and INR 1,000/t in the Ahmedabad and Mumbai markets, respectively. Meanwhile, in the eastern region, Durgapur saw a reduction of INR 300/t.

In central India, Raipur, a key production hub, reported a slight increase of INR 300/t m-o-m. Markets in northern India also witnessed a rise, with Muzaffarnagar noticing a rise of INR 700/t and Delhi INR 400/t.

In south India, mixed trends prevailed: Hyderabad and Chennai recorded declines of INR 1,000/t and INR 500/t m-o-m, respectively, while Bengaluru saw an increase of INR 1,000/t.

The market maintained a moderate sentiment overall, with sluggish buying during the first half of the month. However, trading activity improved in the latter half as manufacturers secured moderate bookings, supported by better spot market demand at lower price levels. Demand from both project and retail segments strengthened. Rising raw material prices further lifted market confidence and provided momentum to finished steel prices.

To stimulate sales and manage inventories, manufacturers reduced offers and extended trade discounts. Inventory levels dropped from 15–17 days earlier to around 12-15 days in July, as buyers booked sufficient material, indicating improved demand in the finished market.

As per JPC data, India’s total rebar production through the IF and BF routes stood at 13.2 million tonnes (mnt) in the first quarter of FY’26, marking a significant 11% rise from around 11.8 mnt in the same period of FY’25, indicating continued growth momentum.

Factors impacting market

Raw material prices rise m-o-m: The rise in finished steel prices was largely driven by higher prices of key raw materials—steel billets and sponge iron—used in IF-route production. Strong buying interest and active trade activity across several markets prompted manufacturers to raise prices. Using Raipur as a benchmark, billet prices rose by INR 400/t m-o-m to INR 37,400/t exw, while sponge iron (PDRI FeM 80% ±1) saw a sharper rise of INR 2,200/t m-o-m, settling at INR 24,600/t exw (prices from 30 June to 31 July 2025).

Additionally, BigMint’s Odisha iron ore fines index (Fe 62%) rose by INR 200/t m-o-m to around INR 5,100/t in July 2025. Iron ore prices rose due to production and dispatch disruptions from heavy rainfall, with the shortage further supported by active east coast exports.

Demand strengthens: Buyers gained confidence to procure material after rebar prices bottomed out in most regions. Demand from both retail and project segments improved as buyers anticipated further raw material price increases. Upward momentum in global raw material markets also bolstered this outlook. Additionally, scheduled maintenance shutdowns at select mills in previous months temporarily reduced supply, supporting a price uptick.

BF-route bar prices drop m-o-m: Trade-level BF rebar prices dropped by INR 3,700/t m-o-m to an average of INR 48,800/t exy-Mumbai amid sluggish demand in July 2025. Weak market sentiment, cautious buying, and monsoon-related disruptions kept buyers on the sidelines. However, some mills increased prices in late July, lending support to trade-level prices in the final week. In the projects segment, prices declined by INR 4,200/t m-o-m to an average of INR 47,400/t FOR Mumbai in July 2025.

Outlook

Domestic steel prices are expected to recover further with rising raw material prices. Gradual receding of the monsoon in various parts of the country and the anticipated pickup in construction activity are also likely to support rebar prices in the near term.

Leave a Reply