- HRC, rebar prices continue downward trend

- Iron ore in Odisha firm on seasonal supply worries

- Mills announce price hike for Aug’25, sentiment recovers

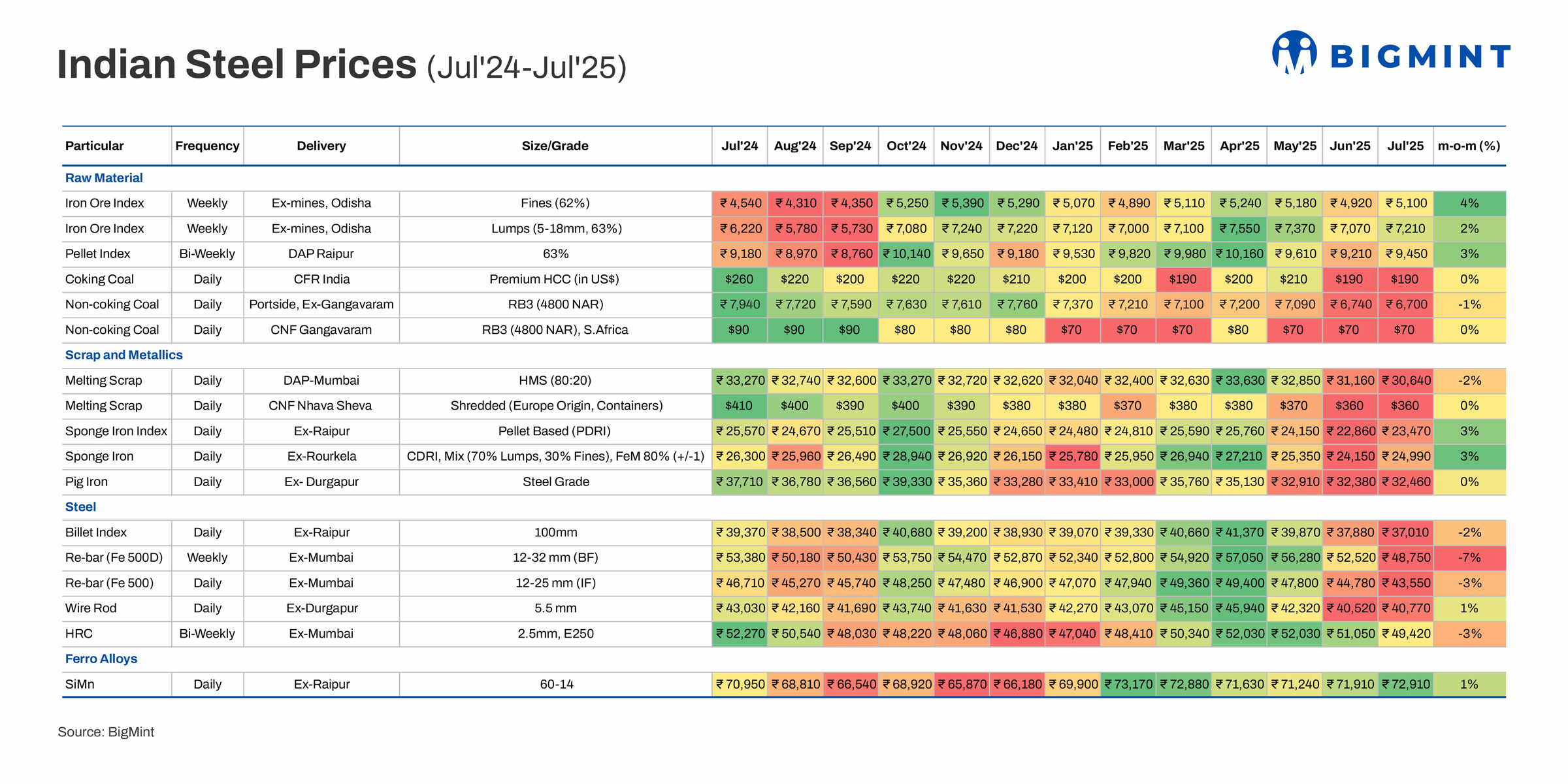

Morning Brief: The domestic steel market continued to remain under pressure in July 2025, with steel prices drifting lower m-o-m while prices of steelmaking raw materials stayed firm, thereby eating into producer margins. Entire July saw steel prices eroding – in sync with the general deterioration in market conditions; however, a late recovery in prices augurs well for the domestic market.

While steel demand has been robust, growing at around 8-9% y-o-y, prices in the domestic market started weakening since May as the positive vibes created by the imposition of the 12% provisional safeguard on steel imports started petering out. The uptick in HR coil and plate imports in July has reignited the debate on the duty being too little, too late.

Price movements in Jul’25

Iron ore: While BigMint’s Odisha iron ore lump index registered a 2% increase m-o-m, the fines index increased 4%. This was largely due to OMC’s auction in which nearly the entire material was sold and bids received were higher by INR 150-175/t m-o-m. Also, rake dispatches in Odisha were impacted in Barbil due to heavy monsoons. These factors supported prices.

Pellets: BigMint’s pellet index registered a 3% uptick in July. Key regions such as Raipur saw a 50% surge in traded volumes due to buyers preferring pellets, which offer better performance and handling advantages during the monsoon season. Due to excessive rainfall, iron ore lump availability and handling were challenging, which made pellets the preferred choice.

Coking coal: Prices of this key steelmaking ingredient remained unchanged m-o-m as steel market sentiments remained subdued. The index remained at the three-month low level in July which it had dropped to in June. This was due to bearish steel market sentiment, cost-effective offers from Canada, and decline in domestic met coke prices. Cautious sentiment continues amid widening bid-offer gaps.

Non-coking coal: South African RB3 coal portside prices fell by 1% m-o-m in July on rising stocks and weak sponge iron market sentiments. However, the uptick in steel prices toward the end of the month supported imported coal prices. This kept seaborne prices unchanged m-o-m. However, coal offers at ports have surged in the beginning of August on rising Panamax freights and tightening availability.

Ferrous scrap: India’s domestic ferrous scrap market hit its lowest point in over four years in July, with prices across Mandi Gobindgarh, Chennai and Jalna declining. Traders attributed the decline to sluggish steel market conditions, greater availability of alternative feedstock like sponge iron, deteriorating raw materials-to-finished steel price spreads, and ongoing liquidity constraints affecting the secondary steel sector.

Sponge iron: Prices showed a 3% recovery in July compared with June after languishing at over 4.5 lows since May. Although longs and semis prices remained subdued amid the monsoon season and export trade to neighbouring regions also remained muted, firm raw material prices supported the marginal recovery in DRI prices.

Pig iron: Pig iron prices remained stable m-o-m after declining in June due to weak demand from the finished steel segment and rising inventories with producers which forced them to offer discounts to clear stocks. However, prices in SAIL and NMDC auctions edged up towards the latter half of July, thereby supporting market sentiments.

Silico manganese: Domestic silico manganese (60-14) prices inched up marginally by 1% m-o-m in in Raipur as key smelters responded to oversupply by strategically curbing production, prompting localised price recoveries. MOIL, too, announced a price revision in manganese ore, effective 1 July. The company implemented a modest 2% increase in prices of ferro grades – both above and below Mn 44% content.

Billet: Sluggish finished steel offtake dampened trade momentum in billets, with prices diving 2% m-o-m, slower than the 5% decrease in June. Lower raw material tags also failed to provide cost support, and overall, market confidence was poor, given a slowdown in construction activity due to monsoon.

Rebar: The primary mills cut rebar prices by up to INR 1,000/t ($12/t) for early-July deliveries as against prices prevailing in end-June. Rebar inventories at Tier-1 mills increased sharply in early-July owing to sluggish sales in June, as volatility in prices and subdued demand posed challenges for mills in securing new orders.

Weak construction demand, monsoon disruptions, and labour shortages impacted the market. Buyers adopted a wait-and-watch approach due to the prevailing disparity between bids and offers, while distributors aimed to offload previously procured high-cost inventories.

IF rebar prices dropped throughout July as order bookings remained subdued despite trade discounts and as buyers continued need-based procurement. Inventory levels stayed elevated at 12-15 days, keeping market sentiment weak.

Wire rod: Prices in Durgapur showed a modest uptick of 1% m-o-m. After sluggish inquiries in the first half of July, buying interest for wire rods picked up sharply in Raipur and Durgapur, helped by strong downstream demand from galvanised and binding wire sectors. This allowed manufacturers to sustain elevated prices amid rising raw material costs.

HRC: The Tier-1 mills rolled over list prices for July sales. While most mills officially maintained the same prices, market participants suggested that some price support in the form of a reduction of INR 1,000-2,000/t ($12-23/t) was possibly offered. Actual transactional prices continued to soften in the spot market as buyers pushed back against prevailing levels.

Heavy rainfall in different part of the country impacted trade, leading to a downturn in demand across most sectors. Inventory with distributors remained elevated, reflecting slow offtake. Buyers preferred to wait and watch, expecting further correction in prices. Delayed payments and tight liquidity conditions also hampered purchases.

Outlook

Leading Indian steel manufacturers have officially raised the list prices of HRC and CRC by INR 1,000-2,000/t for August sales as compared to the net sales price in end-July. BigMint’s India hot-rolled coil (HRC, S275) export index rose by $5/t w-o-w to $540/t (FOB main port), supported by improved global market sentiment and higher Chinese export offers. Chinese HRC export offers rose by $12/t w-o-w last week.

India’s largest merchant iron ore mining company, NMDC, increased list prices of iron ore fines and lump by INR 400-450 for August on improved buying interest and premium bids in recent auctions. These factors are expected to keep prices supported.

On 1 August, trade-level blast furnace-rebar prices increased w-o-w across major Indian markets. Some mills had raised list prices in late-July, and market participants expect steelmakers to announce further hikes for August. This has lent support to trade prices, improving sentiments in the segment.

IF rebar prices, too, increased by INR 900/t ($10/t) w-o-w on 1 August. Mills largely maintained list prices while offering limited trade discounts to clear inventory. Market participants expect a slight uptick in prices in the coming days.

Leave a Reply