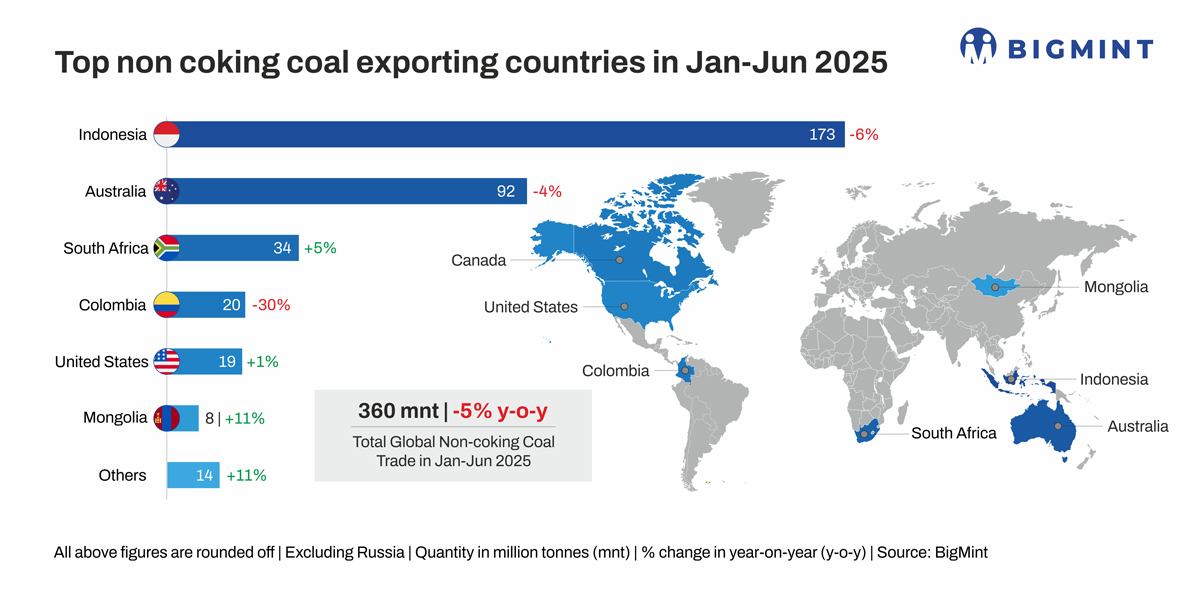

- Indonesian shipments decline 6% amid weather disruptions

- Logistics recovery, Indian demand lift South African exports

Global non-coking coal exports recorded a contraction of 5.1% y-o-y in the first half of calendar year 2025 (H1CY’25). Total shipments fell to 359.65 million tonnes (mnt) from 378.78 mnt in H1CY’24. However, key exporting nations showed sharply divergent performances.

While some countries leveraged improved logistics, favourable trade conditions, and strategic demand linkages, others faced significant headwinds stemming from regulatory changes, adverse weather, and infrastructure bottlenecks.

Indonesia: Weather disruptions, regulatory constraints weigh on exports

Indonesia, the world’s largest non-coking coal exporter, saw shipments decline by 6% y-o-y in H1CY’25 to 173 mnt from 183 mnt. The drop was mainly due to prolonged monsoonal rains disrupting mining and port operations, along with challenges arising from the new HBA benchmark, which created pricing uncertainties and impacted exporter margins.

Australia: Operational bottlenecks, demand diversion impact performance

Australia recorded a 4% decline in non-coking coal exports, shipping 92 mnt in H1CY’25 compared to 96 mnt in the previous year. The downturn was attributed to a combination of labour disruptions at major mines, scheduled maintenance at key export terminals (such as the Port of Newcastle), and limited rail haulage capacity that constrained supply chains.

Additionally, Chinese buyers increasingly shifted towards alternative suppliers such as Russia, South Africa, and Mongolia to reduce dependence on Australian coal amid geopolitical uncertainty and price competitiveness.

Colombia: Domestic disruptions, shrinking European demand drive sharp decline

Colombia registered the steepest decline among key non-coking coal exporters in H1CY’25, with shipments falling by 30% y-o-y to 20 mnt from 29 mnt in the previous year. The sharp contraction was attributed to domestic disruptions and temporary production halts. Additionally, a continued shift in European energy policy towards natural gas, renewables, and nuclear energy significantly reduced demand for Colombian coal.

South Africa: Supply chain recovery, diversified demand support growth

In contrast, South Africa emerged as one of the few exporters to register an increase in shipments, which grew 5% y-o-y to 34 mnt in H1CY’25. The rebound was largely supported by improved rail operations and port handling efficiency, especially from Transnet’s gradual restoration of coal freight capacity to Richards Bay.

Additionally, demand from Indian buyers increased significantly, as they looked to South Africa for consistent supply amid disruptions in Indonesian cargoes. Some diversion of orders from China also contributed to the rise, as buyers sought alternative low-sulphur coal for blending purposes.

Mongolia: Stable supply, strategic geographic position boost volumes

Mongolia experienced a 10.5% rise in coal exports, driven largely by stable output and logistical efficiency in delivering coal overland to northern China, its primary customer. As China continues to optimise its import portfolio to reduce reliance on maritime logistics and cut freight costs, Mongolia remains strategically positioned to benefit from this structural shift. Strengthening border trade infrastructure and the opening of additional customs clearance points further streamlined shipments.

US: Market diversification leads to modest growth

The US registered a modest 1.3% increase in non-coking coal exports, to 19.3 mnt in H1CY’25. The growth was largely due to higher shipments to Asian buyers such as South Korea and Taiwan, which were keen to diversify procurement sources amid global supply uncertainty. However, high internal freight costs, limited competitiveness against Russian and South African coal, and a cooling European market capped further growth potential.

Conclusion

The H1CY’25 global non-coking coal export performance underscores a highly dynamic and fragmented market environment. While some countries capitalised on geographic advantages, improved logistics, or strong bilateral ties, others struggled with a combination of regulatory hurdles, weather disruptions, and weakening demand from traditional markets. Going forward, exporters with agile supply chains, diversified customer bases, and policy alignment will be better positioned to weather market volatility and sustain export competitiveness.

Leave a Reply