- Demand softens from stainless steel, EV sectors

- Indonesian producers continue to raise output

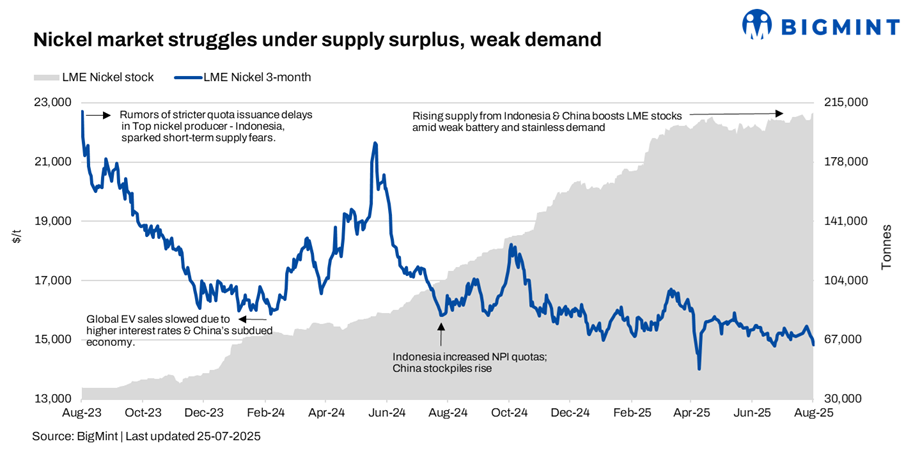

Nickel prices on the London Metal Exchange (LME) inched down by 1% from last week, with the 3‑month contract closing at $14,830/tonne (t). LME nickel stocks remained range‑bound with a slight increase to 209,082 t from 208,692 t a week earlier, driven by continued oversupply from Indonesia alongside lingering weakness in downstream demand — particularly from the stainless steel and battery sectors.

Market highlights

Indonesian output keeps global market oversupplied

Indonesia’s nickel industry continues to ramp up production, feeding a steady flow of material into global supply chains. The surplus capped any significant price upside, with many smelters still operating despite narrowing margins.

Indonesia’s official nickel production quota for 2025 is approximately 200 million tonnes (mnt) of nickel ore.

Stainless steel, battery demand remain tepid

Demand from the stainless steel sector, traditionally the largest consumer of nickel, stayed soft amid lacklustre construction and manufacturing activity in key markets. Battery‑related consumption, while expanding, has fallen short of expectations due to slower EV sales growth and a shift towards lower‑nickel chemistries.

Volatility persists on SHFE amid macroeconomic jitters

Nickel prices on the Shanghai Futures Exchange (SHFE) fluctuated throughout the week, weighed by broader economic uncertainty and a stronger US dollar. Brief rallies spurred by short covering were quickly erased as bearish sentiment dominated.

On 1 August 2025, SHFE nickel prices fluctuated between roughly $14,620-14,950/t, with the average settling near $14,785/t.

Global producers face mounting pressure

Producers outside Indonesia, including in Australia and the Philippines, face increasing cost pressure and operational challenges. Some high‑cost operations have already announced output cuts or strategic reviews as they struggle to remain profitable under current market conditions.

One of the world’s largest nickel producers, Nornickel, reduced its 2025 nickel production forecast by about 4% from the earlier guidance to 196,000-204,000 t, due to major repairs and equipment replacements. This roughly 8,000-t reduction reflects operational challenges and increased costs impacting output.

Outlook

Nickel prices are expected to stay trapped in a narrow range, with the persistent supply glut and fragile demand limiting gains. Any meaningful price recovery hinges on a sustained pick-up in stainless steel output or stronger EV-driven demand — neither of which appears imminent.

Leave a Reply