- Mills may hike HRC prices in Aug’25

- Rebar prices on recovery path in key markets

- Firm iron ore prices to keep steel tags supported

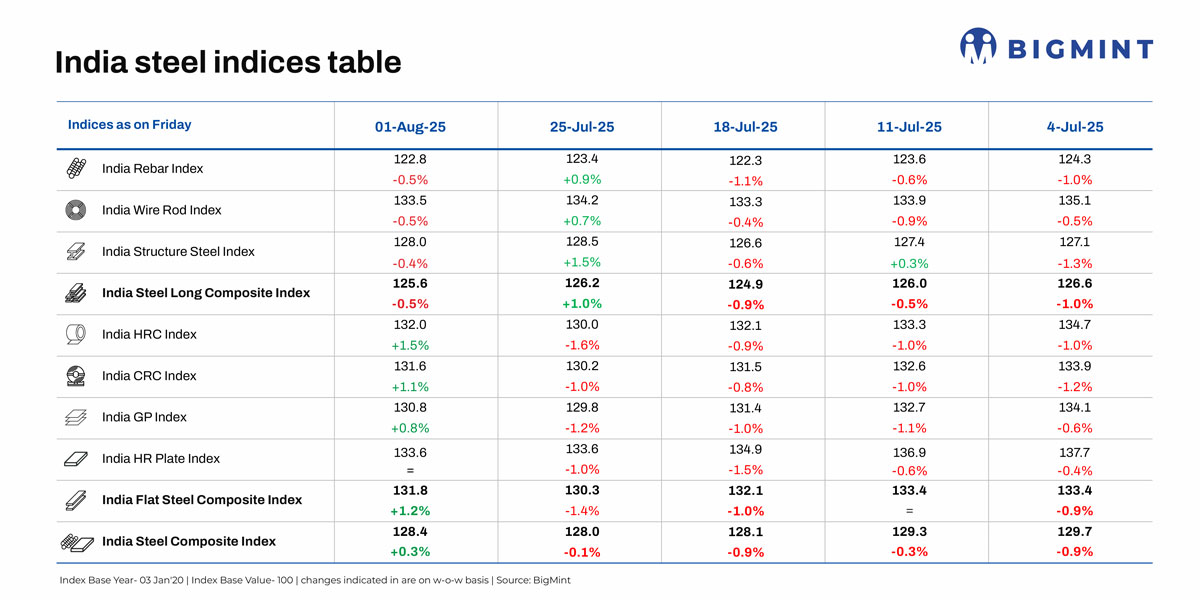

Morning Brief: BigMint’s flagship India steel composite index edged up by 0.3% w-o-w on 1 August 2025 after remaining in the red throughout July. The gradual recovery in domestic steel prices in end-July boosted the index. However, the recovery is still quite nascent; after a decline of over 2 percentage points in July, the index has climbed up by just 0.3%.

The uptick in flat steel prices pushed up the flats composite index by 1.2% w-o-w but the long steel index edged down by 0.5% on prevailing seasonal slowdown. However, long steel prices are on the brink of recovery in early-August.

Analysis of price movements

IF rebar prices show mixed trends: Induction furnace (IF) rebar (which has a market share of roughly 65-70%) prices showed mixed trends w-o-w across key Indian markets. Following decent bookings in the previous week, trade activity slowed as buyers resisted higher prices. Mills largely maintained list prices while offering limited trade discounts to clear inventory. Semi-finished steel prices declined w-o-w, with inventory levels ranging between 10-15 days across regions.

However, prices increased in key markets such as Mumbai amid healthy bookings due to rebar prices bottoming out in July.

BF rebar trade prices up: Trade-level BF rebar prices increased by INR 500/t ($6/t) w-o-w to INR 48,000/t ($549/t) exy-Mumbai, as per BigMint’s assessment on 1 August. Prices are exclusive of GST at 18%. Certain mills raised list prices in late-July, and market participants expect steelmakers to announce further hikes for August.

In the projects segment, prices increased w-o-w as mills sold strong volumes last month, with prices bottoming out in late-July. The BF-IF rebar price gap narrowed in many major markets. The narrowing price spread was one of the major reasons for the hike in BF rebar trade prices this week.

HRC trade prices rise in some markets: Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends w-o-w as some markets reported a rise of up to INR 1,000/t w-o-w to INR 48,900-50,700/t ($565-586/t). Moreover, cold-rolled coil (CRC) prices rose by up to INR 700/t w-o-w to INR 55,000-59,000/t in a few regions.

HRC prices, after peaking at INR 52,700/t in April, have corrected to around INR 48,500/t, a decline of approximately INR 4,000/t. Currently, steel manufacturers are signalling a potential price support of INR 1,000-1,500/t in August.

This anticipated price adjustment is primarily driven by rising raw material costs. An upward price momentum in global raw material markets has further bolstered this outlook. Also, scheduled maintenance shutdowns at select mills in the coming months are expected to temporarily reduce supply, thereby supporting a price uptick.

Outlook

Domestic steel prices are set to recover further with domestic iron ore prices rising in Odisha and NMDC revising August prices upward by INR 400-450/t. Coking coal prices, too, are stable and may rise slightly with sentiments in the Chinese market improving.

Particularly, the upward trend in Chinese HRC prices could create opportunities for domestic mills, strengthening their position in both export and domestic markets. However, rising imports in July indicated that despite regulatory measures it might be difficult to contain imports if global steel demand and production deteriorate in the coming quarters.

On the other hand, domestic construction steel prices are set for further increases, as the potential uptrend in IF rebar prices in key regions provide a boost to BF-origin prices. Also, the gradual receding of monsoon in different parts of the country and the spurt in construction activity are expected to keep rebar prices supported.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply