- SA thermal coal prices rise, Indonesian tags stable

- Domestic coal prices rise amid limited availability

This week, India’s coal market sentiment remained mixed. Imported coal offers rose sharply due to soaring freights, especially for South African cargoes, but actual buying remained limited amid cost resistance. Portside stocks fell slightly as vessel arrivals dropped.

Domestic coal prices edged up despite weak demand, supported by reduced auctions and monsoon-led mining slowdowns. Sponge iron buying eased, adding to a subdued tone. Meanwhile, dry bulk freights cooled this week, on most routes except Indonesia-India.

Overall, market participants remain cautious, awaiting post-monsoon demand clarity and stabilisation in freight dynamics.

South African coal offers soar at ports; Vizag leads rally

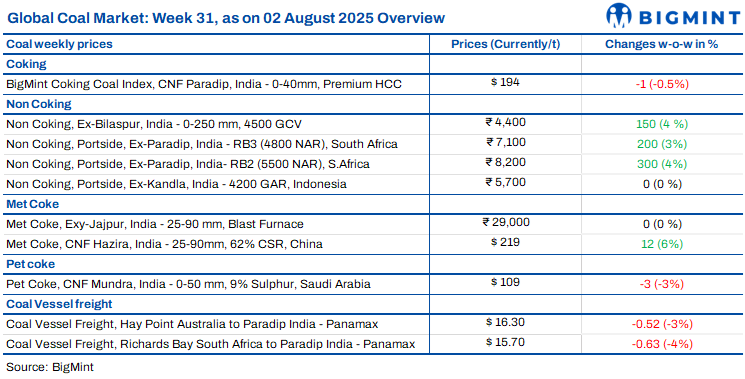

South African thermal coal offers surged at Indian ports this week amid rising freights last week and tight supply. Offers for RB2 rose to INR 8,500/tonne (t) across major eastern India ports this week, but trades were not heard at these levels. RB2 was assessed at INR 8,100/t and RB3 at INR 7,050/t exw-Gangavaram, up INR 300/t and INR 250/t w-o-w. Vizag saw sharper d-o-d hikes of INR 650/t (RB2) and INR 350/t (RB3), driven by Panamax freight rise and low August availability. Sponge buyers started booking for September amid a firm price outlook.

Indonesian coal prices stable as freight costs stay firm

Indian portside prices of Indonesian thermal coal were flat despite sluggish demand and high stocks. While buyers remained cautious, rising freight costs and fewer vessel arrivals during the monsoon kept prices supported. BigMint assessed 5000 GAR steady at INR 7,150/t at Kandla and INR 7,050/t at Vizag, with 3400 GAR at Navlakhi inching up INR 50/t to INR 4,400/t. Previously, freights had risen to $16.14/dmt on key routes. Power plant coal stocks dipped to 54.33 mnt, though supplies remained adequate overall. Prices may stay range-bound, with monsoon impact and Chinese supply trends shaping the outlook post-August.

Domestic coal prices rise despite weak buying interest

Domestic coal prices moved up this week despite a lacklustre market. BigMint assessed 5000 GCV at INR 5,000/t and 4500 GCV at INR 4,400/t exw-Bilaspur – both up INR 150/t w-o-w. SECL’s lower e-auction frequency during the monsoon reduced market availability, lending support to prices. However, demand from traders and industries remained muted as most buyers waited for clearer signals on post-monsoon recovery.

BigMint’s coking coal index dips on weak bids

BigMint’s PHCC index slipped $1/t w-o-w to $194/t CNF Paradip as of 1 August. Bids remained below $195/t, while offers from Australian suppliers held at $197-200/t CFR, causing limited trade. A recent FOB deal for Goonyella was heard at $188.82/t. Canadian offers hovered lower at $182-185/t CFR. With no confirmed trade in the index window, cautious sentiment continues amid widening bid-offer gaps.

Met coke prices stable amid strong pig iron, low imports

India’s met coke prices remained steady this week with better trade activity. BF-grade met coke held at INR 29,000/t in Jajpur and INR 29,800/t in Gandhidham. Import arrivals were paused, as quota approvals under the quantitative restriction (QR) system remained pending. Rising pig iron prices, up INR 400/t w-o-w to INR 32,900/t in Durgapur, supported sentiment. Meanwhile, Chinese met coke prices continued rising, with a fourth straight hike, driven by firm demand and low coke stocks.

Imported pet coke offers ease, demand stays sluggish

Imported pet coke offers in India slipped by $3/t w-o-w but mostly held above $110/t. US-origin cargoes were heard at $110-120/t CFR, while Saudi-origin offers stood at $109-111/t. One offer was heard at $113/t. Although buyers showed interest at these levels, actual trades remained few due to weak demand, monsoon disruptions, and cautious buying across the market.

Nayara, MRPL raise pet coke prices for Aug’25

Nayara Energy and MRPL have increased pet coke prices for August, reflecting firm demand. Nayara raised its prices by INR 300/t m-o-m to INR 13,730/t, 5.1% higher y-o-y, maintaining a market edge as RIL continued with internal consumption of its production. MRPL hiked prices by INR 120/t, setting road supply at INR 10,690/t and rake/barge at INR 10,390/t. The INR 300/t differential accounts for handling costs. While Nayara led on absolute pricing, MRPL’s rates maintained consistency, driven by stable cement-sector demand and disciplined supply in southern markets. Both refiners’ hikes signal continued pricing support despite the monsoon season.

Coal freights ease w-o-w; outlook stays weak

Coal shipping rates to India dipped this week on the Australia-India and South Africa-India routes amid slow Pacific trade and reduced bookings, although the Indonesia-India Supramax route saw a slight rise due to loading issues. Port congestion and monsoon delays added to sluggish movement. With inventories falling 5.3% w-o-w to 14.77 mnt, freights remained under pressure. Demand is expected to stay weak through August unless industrial buying recovers.

Leave a Reply