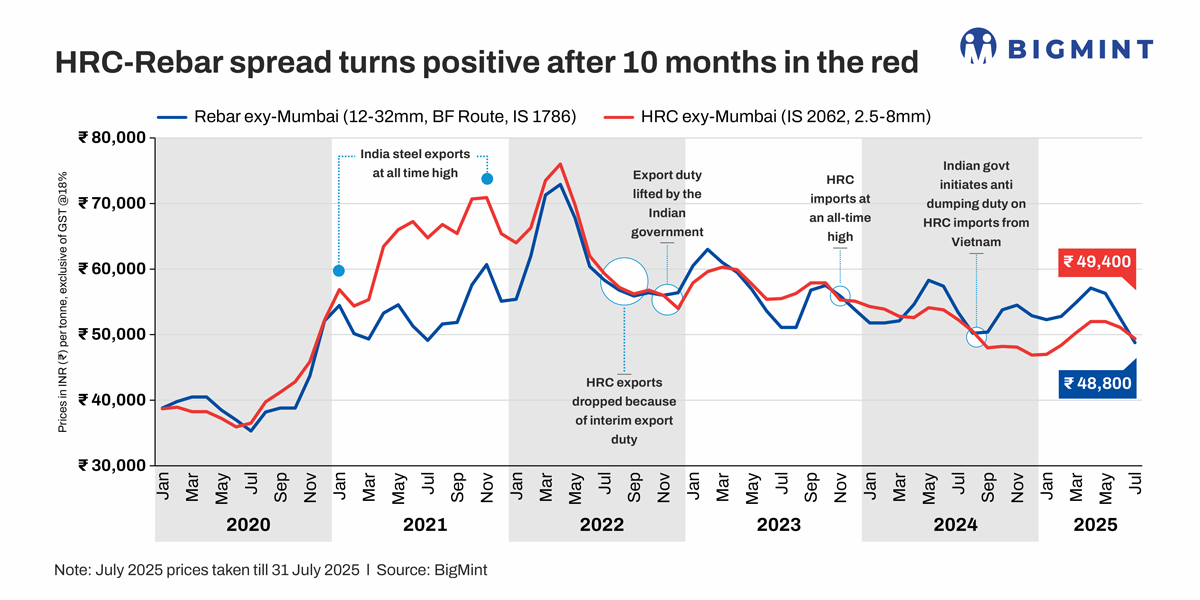

- Spread stands at INR 600/t in Jul’25

- Seasonal slowdown still impacts market

- Prices showing signs of recovery in early-Aug

Morning Brief: After remaining in reverse territory for 10 consecutive months since September 2024, the HRC-rebar spread in the domestic steel market finally turned positive in July. While domestic steel prices remained in the red in July due to monsoon-induced seasonal slowdown and global steel market downturn, prices started showing early signs of recovery towards the end of the month.

Although both HRC and reinforcement bar prices trended lower in July, the downturn in the longs segment was steeper compared to flats because of monsoon affecting construction activity in large swathes of the country. So, while prices of construction steel bar produced via the BF route drifted down by INR 3,700/t m-o-m in July, HR coils fell by INR 1,700/t. The HRC-rebar spread stood at INR 600/t in July compared to a reverse spread of INR 1,400/t in June.

Under normal market conditions, HRC commands a premium of around INR 4,000-5,000 over BF rebar. However, persistent weakness in global steel prices from end-2024 onwards has eroded domestic flat steel prices and pushed the spread into reverse zone.

Factors affecting steel prices

HRC prices under pressure: The Tier-1 mills rolled over list prices for hot-rolled coils (HRCs) and cold-rolled coils (CRCs) for July sales. While most mills officially maintained the same prices, market participants suggested that some price support in the form of a reduction of INR 1,000-2,000/t ($12-23/t) was possibly offered. Actual transactional prices continued to soften in the spot market as buyers pushed back against prevailing levels.

Heavy rainfall in different part of the country impacted trade, leading to a downturn in demand across most sectors.

A market participant told BigMint: ”The earlier optimism surrounding the potential implementation of the safeguard duty has subsided, resulting in the erosion of most of the recent price gains. Buyer enquiries have slowed while credit realisation cycles are extending beyond normal timelines, indicating liquidity pressure.”

Inventory with distributors remained elevated, reflecting slow offtake. Buyers preferred to wait and watch, expecting further correction in prices. Delayed payments and tight liquidity conditions also hampered purchases.

In the last week of the month, HRC trade prices fell by up to INR 800/t. As buyer interest continued to fade, both steel mills and traders were increasingly focused on clearing their inventories. In fact, a source pointed out that to maintain their sales volumes, some mills even considered offering support by reducing prices by INR 2,000-2,500/t, although this could not be confirmed by BigMint.

Imports edge up: India’s bulk imports of HRCs touched 361,505 t as of 19 July, based on vessel line-up data. Around 236,660 t of additional cargo are expected by the first week of August. As of 19 July, import volumes of HR plates reached 30,700 t. This marked a substantial increase compared to June and May, when imports totalled 2,469 t and 14,672 t, respectively.

Based on current vessel line-up data, an additional 2,288 t of HR plates are projected to arrive by the end of July, with another 16,500 t expected in August. High import volumes weighed on prices.

HRC export prices drop: HRC FOB export offers from India to the EU dropped $5/t m-o-m in July. However, the decline since end-April has been precipitous – around $60 – due to muted buying interest in the EU amid the summer holidays and high energy prices and inflation impacting steel production in Europe. Offers to other leading export destinations such as the Middle East remained on hold in July amid competitive prices offered by Chinese suppliers. The downturn in the export market weighed on domestic flats prices.

BF rebar prices decline: The primary mills cut rebar prices by up to INR 1,000/t ($12/t) for early-July deliveries as against prices prevailing in end-June. Rebar inventories at Tier-1 mills increased sharply in early-July owing to sluggish sales in June, as volatility in prices and subdued demand posed challenges for mills in securing new orders.

Weak construction demand, monsoon disruptions, and labour shortages impacted the market. Buyers adopted a wait-and-watch approach due to the prevailing disparity between bids and offers, while distributors aimed to offload previously procured high-cost inventories.

IF rebar prices dropped throughout July as order bookings remained subdued despite trade discounts and as buyers continued need-based procurement. Inventory levels stayed elevated at 12-15 days, keeping market sentiment weak.

Outlook

On 1 August, trade-level blast furnace-rebar prices increased w-o-w across major Indian markets. Some mills had raised list prices in late-July, and market participants expect steelmakers to announce further hikes for August. This has lent support to trade prices, improving sentiments in the segment.

IF rebar prices, too, increased by INR 900/t ($10/t) w-o-w on 1 August. Mills largely maintained list prices while offering limited trade discounts to clear inventory. Market participants expect a slight uptick in prices in the coming days.

On the other hand, HRC prices seem to have received some support from the uptick in Chinese HRC export offers. Moreover, expected production cuts in China in the latter half of the year (some estimates suggest a 4% y-o-y reduction in crude steel output in CY’25) are expected to bolster global and domestic flat steel prices. In fact, initial signs of recovery are visible, with leading producers hiking coated flats prices in the beginning of August.

In addition, maintenance shutdowns at major facilities may also support prices in August and the spread, therefore, is expected to remain in the green.

Leave a Reply