- Fixtures drop w-o-w on sluggish market sentiments

- Baltic dry bulk index weakens d-o-d

Dry bulk iron ore freight rates extended gains across major routes this week, except the India-China corridor. However, vessel hiring activity slowed across both the Pacific and Atlantic basins compared to the previous week, dampening overall sentiment in the dry bulk freight market.

The Capesize market managed to remain firm this week, though reported fixtures were limited. Outside the Pacific, fresh iron ore cargoes were scarce, with Rio Tinto being the only major miner actively seeking tonnage during Asian trading hours.

In contrast, the Supramax market saw a negative trend, particularly on the India-China route. “Last week, the market held strong despite higher bunker prices and tighter tonnage supply in the East Coast India region. However, with a decline in cargo availability and softening bunker prices, the market is once again under pressure,” a source told Bigmint.

Another source noted regarding the India-China route, “While the market has started to soften, owners are still maintaining firm rate expectations. Some charterers have managed to fix below $12/DMT, but these were mostly for prompt vessels. A further decline in rates may take some time to materialize.”

However, owners are holding out for higher daily time charter (TC) rates to charter out their vessels, while charterers continue to offer lower freight rates. Meanwhile, amid a sharp drop in freight derivative rates toward the end of Asian trading hours, market confidence took a hit. The Forward Freight Agreement (FFA) market also saw a notable decline this week, which is likely to add further downward pressure on freight rates in the near term.

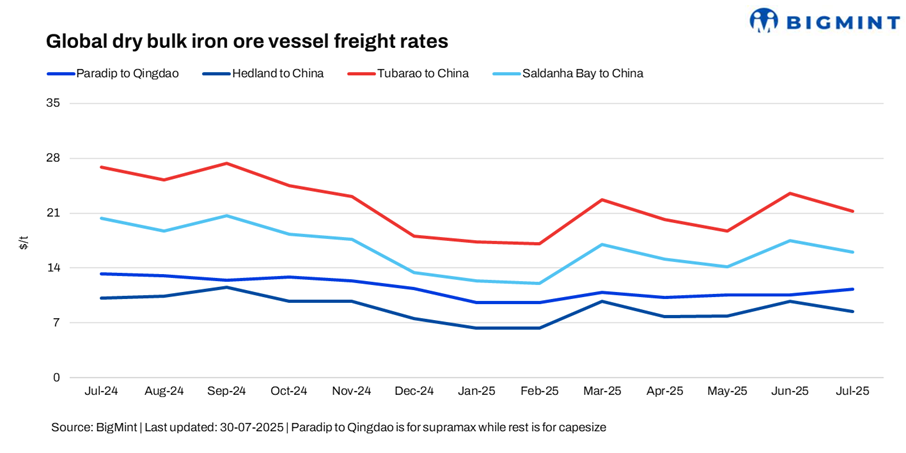

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freight rates for Supramax vessels from the Indian Ocean to China dropped to $11.50/dry metric tonne (DMT), down by $0.68/DMT w-o-w. “Unfortunately, the monsoon continues to play a significant role, contributing to the current softening of the market”, added a source. Indian BF-route players reported weak market sentiment, with cautious buying and monsoon-related disruptions keeping buyers on the sidelines. While most participants remain uncertain about a near-term price rebound, some believe the market may have bottomed out, indicating limited downside from current levels.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freight rates for iron ore shipments from Western Australia to China rose to $10/DMT, marking a w-o-w increase of $0.45/DMT. However, sources largely described the market as “quiet”, noting that trading activity remained sluggish and cargo volumes appeared relatively limited.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freight rates for Brazil-to-China shipments rose significantly by $0.85/DMT w-o-w, settling at $24/DMT. There was a lack of activity in the Atlantic basin throughout the week, with no reported fixtures concluded.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freight rates from Saldanha Bay to Qingdao also inched up by $0.55/DMT w-o-w, settling at $18/DMT. The rise was attributed to persistent logistical issues at South African ports, which have disrupted operations and led to reduced vessel availability.

Market highlights:

- Baltic index drops d-o-d, weak demand across vessel segments: The Baltic Exchange’s main sea freight index, which tracks rates for dry bulk carriers, declined d-o-d on 30 July 2025, driven by weaker demand across all vessel segments. The overall index dropped d-o-d by 114 points to 1,995, with the capesize index falling 290 points to 3,186 on a daily basis. Meanwhile, the supramax index also slipped d-o-d by 10 points to 1,271.

- China’s iron ore spot prices drop $3/t w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $102/tonne (t) CFR China on 30 July 2025, down $3/t/t w-o-w. The decline came ahead of the upcoming Politburo meeting, with trading activity centered around medium-grade fines. Market participants are now closely watching for potential new stimulus measures. Additionally, iron ore prices at Chinese ports fell, reflecting a pullback from last week’s improved market sentiment.

- DCE iron ore futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract decreased by RMB 25.5/t ($3.5/t) w-o-w to RMB 789/t ($109.9/t) on 30 July.

Outlook

The dry bulk iron ore freight market faces a softening outlook in the near term, driven by weak demand, seasonal disruptions, and limited trading activity. While some regional supply tightness persists, overall sentiment remains cautious as players await clearer signals on Chinese stimulus and post-monsoon demand recovery. In line with the broader trend, a source noted, “Yes, the market is softening and is expected to decline further.”

Leave a Reply