- Benchmark HRC prices down INR300/t w-o-w

- Uptrend in Chinese prices to boost domestic market

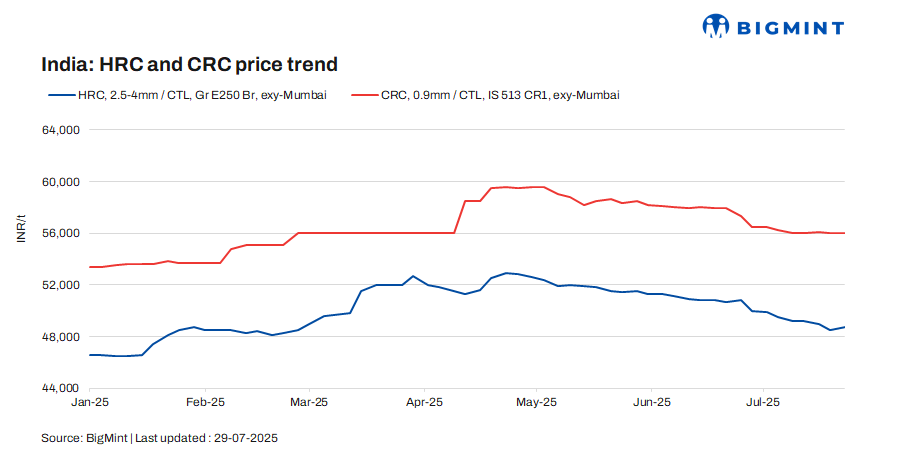

Trade-level prices of hot-rolled coils (HRCs) in India showed mix-trends w-o-w as some markets reported a rise of around INR 200-1000/tonne (t) w-o-w, while some others witnessed a drop of around INR 100-300/t to INR 48,800-50,600/t ($565-586/t). Moreover, cold-rolled coil (CRC) prices in some markets remained rangebound, while rising by INR 500-700/t w-o-w to INR 54,300-58,500/t ($621-669/t) in others.

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 300/t ($4/t) w-o-w to INR 48,700/t ($557/t) on 29 July 2025 against INR 49,000/t ($561/t) a week ago. On the other hand, CRC (IS513, Gr O, 0.9 mm/CTL) prices inched down by INR 100/t ($1/t) w-o-w to INR 56,000/t ($641/t) on Tuesday against INR 56,100/t ($642/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market updates

Indian HRC market shows mixed sentiment : HRC prices, after peaking at INR 52,700/t in April, have corrected to around INR 48,500/t—a decline of approximately INR 4,000. Currently, steel manufacturers are signalling a potential price support of INR 1,000-1,500/t in the August sales cycle. This anticipated price adjustment is primarily driven by rising raw material costs, including iron ore, pellets, sponge iron, and pig iron. Moreover, the upward price momentum in global raw material markets further bolsters this outlook. Additionally, scheduled maintenance shutdowns at select mills in the coming months are expected to temporarily reduce supply, thereby supporting price stability and potential upward movement.

Demand in the Indian HRC market remained sluggish this week. However, a market participant indicated that the “market looks positive. Expectations of price support in the upcoming month is expected”. Moreover, a source informed BigMint, “market would likely sustain only if production cuts are implemented”.

Import volumes: India’s bulk imports of HRCs touched 441,130 t as of 26 July, based on vessel line-up data. Around 243,917 t of additional cargoes are expected by the first week of August.

Export volumes: India’s bulk exports of HRCs touched 65,401 t as of 26 July, based on vessel line-up data with BigMint. Moreover, around 65,000 t of additional cargo is recorded.

BigMint’s India hot-rolled coil (HRC, S275) export index rose by $5/tonne (t) w-o-w to $540/t (FOB main port). This uptick is attributed to improvement in global market sentiment and a rise in Chinese export offers.

However, the Middle East (ME) market presents a different picture. While Chinese prices have increased w-o-w, trade activity remained limited. Additionally, Indian mills refrained from offering HRCs to the Middle East, prioritizing stronger domestic demand and facing heightened competition from global suppliers.

Outlook

The Indian HRC market is likely to expect price support in the coming month despite mixed sentiments and a wait-and-watch stance adopted by buyers, who remain cautious ahead of upcoming price announcements. However, if the upward trend in Chinese HRC prices continues, it could create opportunities for domestic mills, strengthening their position in both export and domestic markets.

Leave a Reply