- Suppliers lift offers amid better demand in local markets

- Liquidity crunch, monsoon rains exert downward pressure

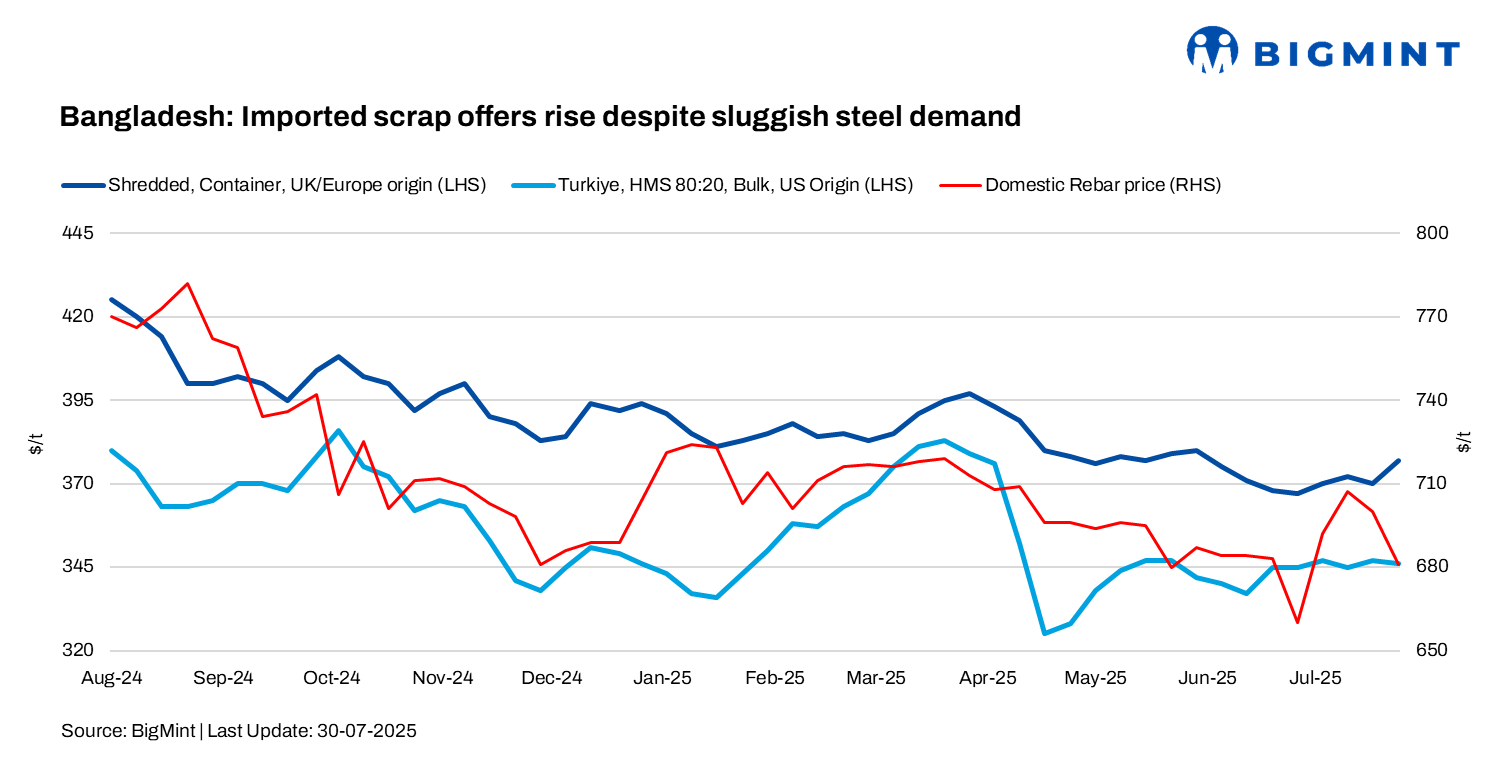

Bangladesh’s imported scrap prices increased by $5-7/tonne (t) w-o-w, despite market activity in Bangladesh’s steel sector remaining sluggish.

The moderate price hike could be attributed to higher offers from suppliers, especially as UK/EU- and US-based suppliers witnessed better demand in their local markets.

The bullish momentum in the Pakistani market may also be another driver. Although significant volumes have not been booked, current trade activity supported suppliers’ higher offers.

Notably, most transactions were on credit in the last couple of days. The severe liquidity crunch in the market — with sluggish clearing of payments — hindered deal closures.

Persistent banking issues, such as with obtaining letters of credit (LCs), also strained trade activity. Traders expressed frustration over uncooperative banking practices, describing the approach of financial institutions as exploitative.

BigMint’s weekly assessments

- European-origin HMS (80:20) prices inched up by $4/t w-o-w to $356/t.

- European-origin containerised shredded was up $7/t w-o-w at $377/t.

- Japanese-origin H2 bulk prices stood at $342/t, up by $2/t w-o-w.

- US-sourced HMS (80:20) bulk prices stood at $353/t, up by $2/t w-o-w.

Market sentiment

A mill-side participant noted that activity has weakened following nearly three weeks of continuous monsoon rains, while unresolved issues from the previous government continued to delay infrastructure and public projects, keeping overall market sentiment under pressure.

Latest container offers (CFR Chattogram) for Australian HMS 1 were heard at around $355/t. Indicative offers for Malaysian busheling were at $380-385/t, while Hong Kong PNS was heard at $385-390/t.

US bulk offers to Chattogram were heard in the range of $368-372/t, with some shippers quoting up to $375/t. Australian bulk shredded was indicated at $366-370/t, though buying interest remained weak.

In bulk, Japan H2 was offered at $340-345/t, while bids were at $335/t. Moreover, HS at $366-370/t.

Domestic market

In the domestic market, melting scrap (HMS 80:20) was assessed at BDT 51,000/t ($416/t), billets at BDT 68,000/t ($553/t), and PNS scrap at BDT 52,000/t ($423/t). Local scrap prices appear to have reached the bottom after recent declines.

Recent deals

- PNS from Hong Kong (oversize material) – 1,000 t sold at $388/t CFR Chhattogram.

- PNS from Singapore – 3,500 t sold at $378-382/t range CFR Chhattogram.

- PNS from Malaysia – 2,000 t sold at $382/t CFR Chhattogram.

Outlook

The market is expected to recover gradually after the monsoon, supported by improved liquidity and political clarity, though real demand revival will depend on infrastructure progress and stable financing conditions.

Leave a Reply