- Chinese firm plans new scrap smelter

- European traders brace for US tariff

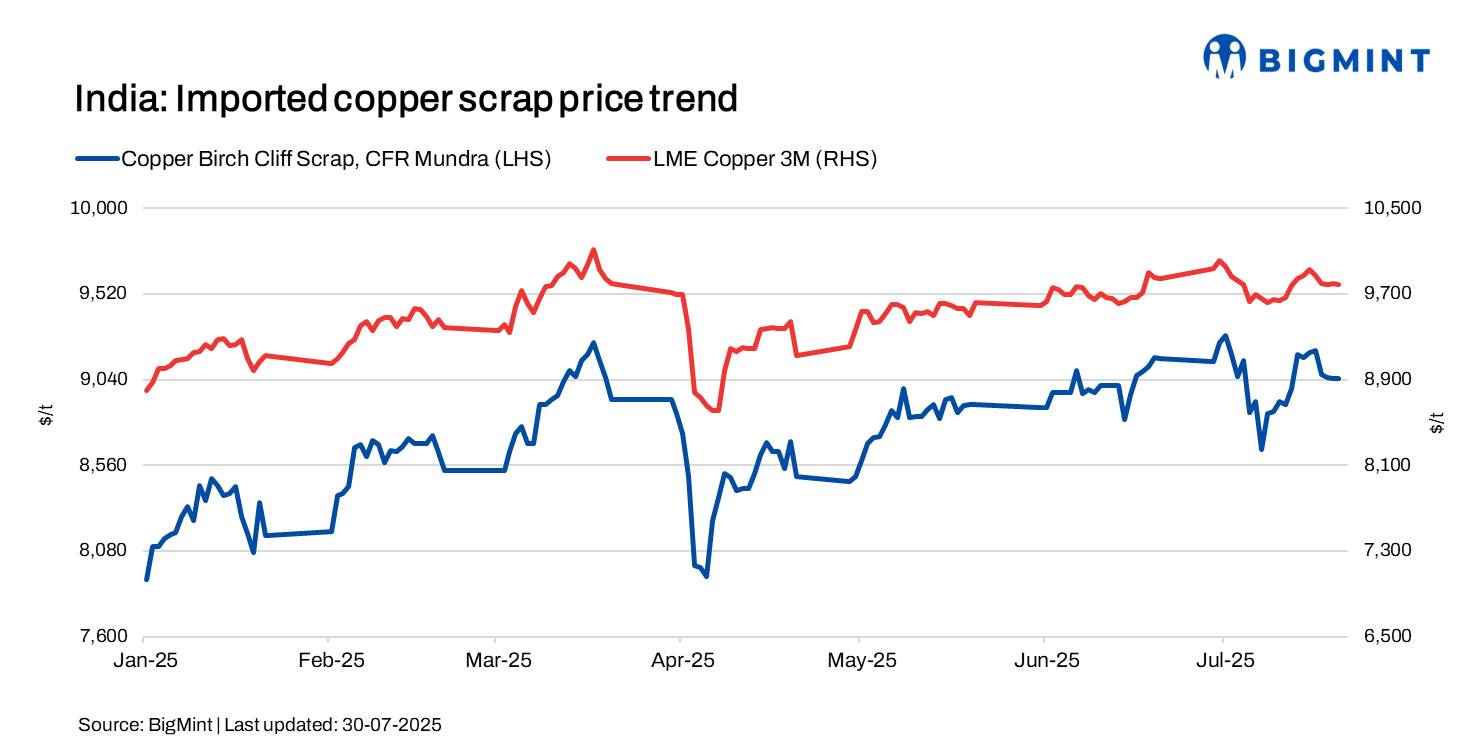

Indian imported copper scrap prices edged down w-o-w, tracking a minor 0.8% w-o-w drop in LME futures to $9,789/tonne (t), amid persistent supply constraints and uncertainty over potential US import tariffs. However, futures stayed below the three-month high of $10,005/t recorded on 3 July, adding mild pressure on domestic prices.

According to BigMint’s assessment, copper Birch cliff scrap was assessed at $9,045/t, down by 1.6% w-o-w, while USA motors mix stood at $1,170/t (both CFR Mundra), stable w-o-w.

Imported market scenario

Tight global supply of refined copper cathode has sustained strong buying interest in high-grade copper scrap, especially in India.

India’s copper scrap imports rose sharply by 25% m-o-m in June to 42,620 t, up from 34,130 t in May, according to BigMint, highlighting sustained import reliance.

Brass Honey demand was reported strong in the Jamnagar market, supported by local buying activity. Imported offers for Middle East-origin Honey Scrap with 4% attachment were heard in the 63-64% range of 3M LME. Overall sentiment remains positive, driven by steady demand and constrained refined copper availability.

On 30 July, KEC International Ltd., an RPG Group company, announced it has secured fresh orders totaling INR 1,509 crore across key sectors. These include transmission and distribution (T&D) projects in India and overseas, a transportation order in the Train Collision Avoidance System (TCAS) under Kavach, and contracts for cables and conductors supply in domestic and global markets. The company’s MD & CEO, Vimal Kejriwal, highlighted the significance of these wins in expanding their global T&D presence and strengthening Indian Railways’ safety. With this, KEC’s year-to-date order intake surpasses INR 7,000 crore.

Domestic market scenario

The domestic copper scrap market continues to trade in a rangebound manner as the ongoing monsoon season weighs on overall demand. While trading activity remains intact, it is mostly confined to smaller volumes due to weather-related disruptions.

Copper armature scrap was assessed at INR 806,000/t ex-Delhi, almost stable w-o-w. Secondary continuously cast rods (CCRs) (99.90%) were assessed at INR 856,000/t ex-Delhi, down 1.6% w-o-w. Meanwhile, primary CCR prices stood at INR 895,000/t, down by 0.5% w-o-w.

Brass Honey demand also remains firm in the Jamnagar market, supported by consistent buying interest.

European market update

The European copper scrap market saw adjustments in discounts amid shifting market dynamics, especially with traders anticipating the upcoming 50% US tariff set to take effect on 1 August. Despite these changes, copper cathode premiums remained stable, as market participants took a cautious approach and paused to gauge the future price direction.

Prices for key copper scrap grades such as Berry and Candy declined slightly, now trading at 97.5-98.5% of the LME cash price, compared to 97.75-98.75% on 22 July. Most spot activity was concentrated around the 98% mark.

Meanwhile, Millberry copper scrap maintained its value at 99-100% of LME cash, reflecting continued demand for high-purity material. Birch cliff scrap prices also held steady in the range of 91-93.5% of LME cash.

Previously, limited availability of copper cathodes pushed the market to depend more heavily on high-grade copper scrap. However, with a drop in shipments to the US, local supply in Europe has improved, helping ease the earlier pressure on cathode availability.

China market overview

Chinese producer Fuye plans to set up a new secondary copper smelter in Shangrao city, Jiangxi province, with a refined copper capacity of 180,000 t/year. It will use copper scrap, ingots, and electrolytic residues, though construction and commissioning timelines remain undisclosed.

Despite China-US trade tensions, China imported 1.15 mnt of copper scrap in H1CY’25 — similar to last year — reflecting its continued role in supporting domestic supply.

Outlook

India’s copper scrap market is likely to stay firm in the near term, supported by a sharp 25% rise in imports, strong substitution demand amid tight refined copper supply, and steady buying interest for high-grade scrap like Millberry and Candy Berry. Despite monsoon-related disruptions limiting spot availability, prices remain supported by higher LME levels and active trading in key hubs. Demand for Brass Honey and CCRs remains strong, and post-monsoon recovery in logistics could further boost market activity. Overall sentiment stays positive, with tight supply and firm demand expected to keep prices elevated.

Leave a Reply