- Middle East, Africa top importers, overtake SE Asia

- Domestic demand woes, efforts to duck tariffs drive exports

- Export offers drop to multi-year lows, boosting shipments

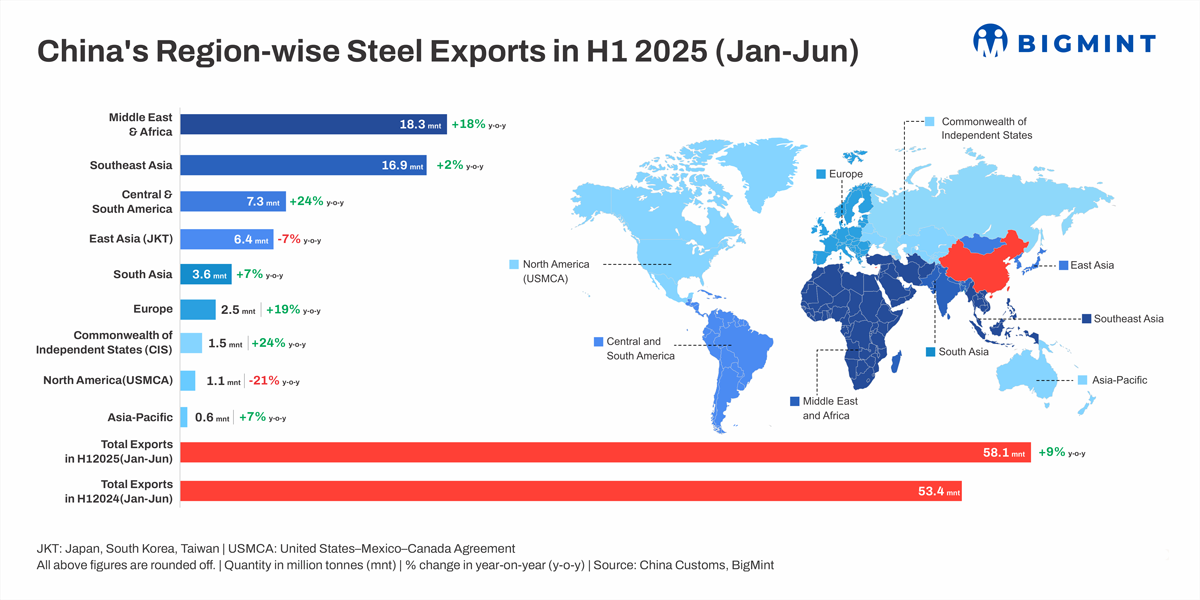

Morning Brief: China’s steel exports recorded a healthy uptick of 9% y-o-y in January-June 2025 (H1CY’25) to 58.1 million tonnes (mnt), as per data available with BigMint.

Volumes increased steadily amid continued frontloading of shipments and competitive prices offered by exporters. Rising trade protectionism by importing regions failed to stem exports, instead prompting product-wise and geographical diversification.

BigMint goes behind the scenes.

The Middle East and Africa became Chinese exporters’ top destination for steel shipments in H1CY’25, overtaking Southeast Asia. Exports to the region surged by 18% y-o-y, with Nigeria and Tanzania recording spikes of 108% and 60% to 0.99 mnt and 0.68 mnt, respectively.

The leading importers — UAE and Saudi Arabia — also witnessed moderate growth, of 11% and 17% to 2.85 mnt and 2.56 mnt, respectively. Export growth to these two countries was supported by China’s competitive pricing, with Saudi Arabia also witnessing strong demand from infrastructure activity.

Turkiye, however, witnessed a slight 3% drop due to an anti-dumping duty imposed late last year.

Volumes to Southeast Asia logged a minor 2% growth to 16.88 mnt, with a 25% drop in Vietnam’s volumes (4.80 mnt) — due to the anti-dumping duty on flats — offset by a 20% y-o-y uptick in Thailand (3.01 mnt). The Philippines, Malaysia, and Indonesia also received moderately higher arrivals, despite the latter two countries having imposed import tariffs.

Central and South America appear to be emerging as a hotspot of activity for Chinese exporters. Shipments to the region surged 24% y-o-y to 7.3 mnt. Brazil received the highest volume, but exports were up by a mere 1% y-o-y. Exports to Brazil plunged 51% m-o-m in June, likely due to the initiation of an anti-dumping investigation into Chinese steel imports.

Peru and Chile also saw double-digit growth of 37% and 23% y-o-y, to 1.13 mnt and 0.87 mnt, respectively.

Exports to East Asia dropped 7% y-o-y to 6.42 mnt, fuelled by anti-dumping duties by South Korea and Taiwan. Imports by South Korea slid by 15% (3.75 mnt) and by Taiwan 29% (0.68 mnt). Concurrently, Hong Kong overtook Taiwan to become the second-largest importer of Chinese steel, with a sharp 67% uptick in volumes.

Conversely, South Asia recorded a 7% y-o-y rise in arrivals to 3.58 mnt, led by 35% growth in exports to Pakistan (1.65 mnt). India was able to reduce its imports by 24% with the help of a safeguard duty, which has been able to erode China’s price advantage.

Meanwhile, exports to Europe and CIS nations climbed up by 19% and 24% y-o-y in H1CY’25.

Factors driving China’s steel exports in Jan-Jun’25

Flagging demand, overcapacity woes trouble domestic market: Domestic consumption, which has severely diminished following the property market collapse, remained weak, pushing steelmakers to turn to overseas markets to offload surplus supply. Notably, the official manufacturing purchasing managers’ index (PMI) was in the contraction zone over April-June, while new construction starts slumped by 20% y-o-y in January-June.

Tariff tensions push exporters to frontload shipments: Intense market volatility prompted Chinese exporters to frontload shipments to avoid the impact of any potential tariff hikes by Trump. Moreover, the US reciprocal tariffs could also significantly disadvantage China’s trading partners, and this fear may also have led to higher procurement by importers.

China edges out competitors with competitive pricing: China’s nearly unbeatable export offers allowed it to edge out competitors in regions such as the Middle East. Indian mills have withheld hot-rolled coil (HRC) offers to the region, citing unviable prices.

China’s HRC export offers also hit a five-year low of $445/tonne (t) FOB Rizhao in June, falling by over $20/t from January. The H1 average stood at $461 FOB Rizhao, in comparison to Japan’s $456/t FOB Tokyo (recorded till May), South Korea’s $499/t FOB Seoul, and Russia’s $474/t FOB Black Sea.

Outlook

Industry sentiment seems to be mixed on whether China’s steel exports will decline in H2CY’25. While some sources have forecasted a sustained uptrend, others believe that a slowdown is more likely. For example, Chinese consultancy firm Mysteel Global projects a contraction of 5 mnt y-o-y in H2, with CY’25 exports totalling 110.6 mnt, down by 460,000 t y-o-y.

Mysteel attributes the marginal decline to a persistent weakening in global manufacturing activity, as well as growing trade tensions. Additionally, China’s intense frontloading of shipments in early 2025 may have taken the edge off prospective demand, with the slowdown growing more evident from September.

China’s crude steel production may also drop further as China takes steps to combat industry-damaging market competition and advance in decarbonisation goals. Coupled with regular stimulus packages, this may help narrow the demand-supply gap and lead to lower urgency to export.

Nonetheless, given that China has consistently defied expectations of a potential moderation in export volumes, it may be too early to make definitive projections.

Leave a Reply