- Crude steel output up 2% y-o-y, sales surge 15%

- EBITDA rises 21% y-o-y but declines 23% q-o-q

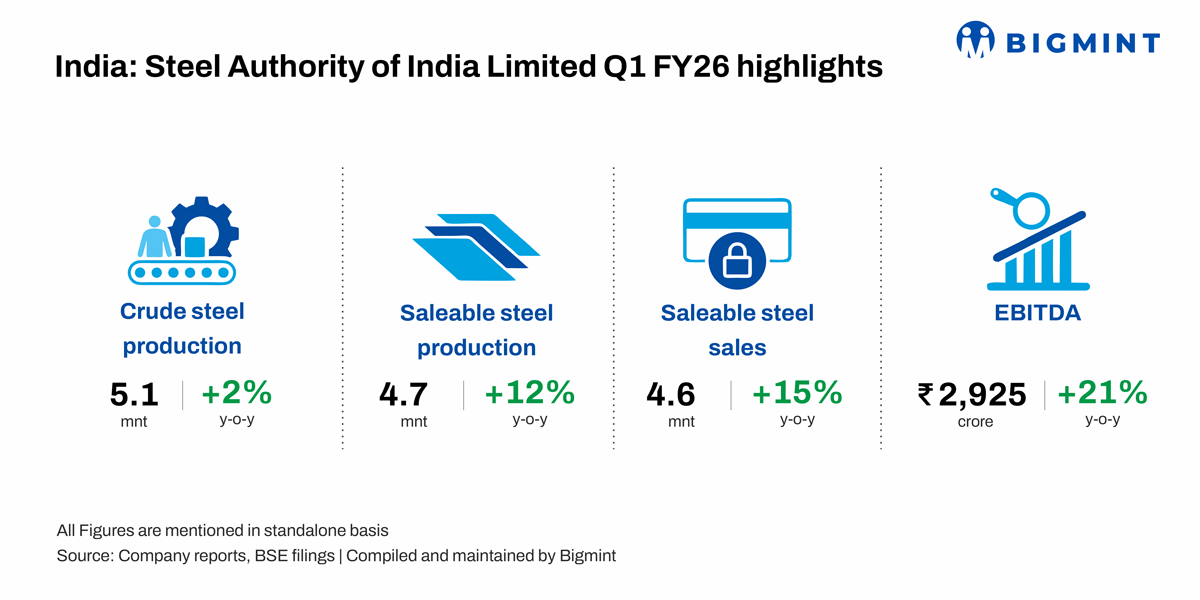

Steel Authority of India Limited (SAIL), the country’s largest public sector steel producer, posted robust operational and financial performance for the first quarter of fiscal year 2026 (Q1FY’26). The company achieved notable y-o-y growth across sales, production, and profitability, while maintaining strong momentum in its capacity expansion programme.

Key performance highlights – Q1FY’26

Capex progress accelerates: SAIL invested INR 1,642 crore towards capital expenditure in Q1FY’26, surpassing its internal target for the quarter. The company reiterated its full-year capex guidance of INR 7,500 crore, with a major share allocated to the 4.5 million tonne per annum (MTPA) expansion project at IISCO Steel Plant (ISP), Burnpur. Management expects capex deployment to further ramp up from FY’27 as project execution advances.

Solid growth y-o-y in production, sales

Crude steel output inches up y-o-y: Crude steel production increased 2% y-o-y to 5.1 million tonnes (mnt), from 5.0 mnt in Q1FY’25. Sequentially, output remained stable versus Q4FY’25.

Saleable steel production rises y-o-y: Saleable steel production increased 12% y-o-y to 4.7 mnt, compared to 4.2 mnt a year earlier.

Sales volumes surge y-o-y: Sales in Q1FY’26 reached 4.6 mnt, marking a 15% y-o-y surge over the 4.0 mnt registered in Q1FY’25. On a q-o-q basis, sales were down 14% from a record 5.3 mnt in Q4FY’25, reflecting typical seasonal weakness and inventory reduction by channel partners.

Optimistic guidance maintained: For FY’26, SAIL has set a sales volume target of 18.5 mnt, which includes approximately 0.37 mnt from the marketing of NMDC Steel’s products.

Financial, cost performance

EBITDA rises y-o-y: Stood at INR 2,925 crore, up 21% y-o-y from INR 2,420 crore in Q1FY’25. However, EBITDA declined 23% q-o-q due to an exceptional inventory valuation loss and lower price realisations.

Coking coal costs fall q-o-q: Average blended coking coal costs eased 10% to INR 15,918/tonne (t) in Q1FY’26 from INR 17,653/t in Q4FY’25. Imported coking coal averaged INR 17,600/t during the quarter. Management expects coal prices to remain broadly stable in the upcoming quarter.

Net sales realisation (NSR) increases q-o-q: The net sales realisation (NSR) for flat products rose to INR 50,400/t in Q1FY’26, compared to INR 47,300/t in Q4FY’25. For long products, NSR climbed up to INR 54,500/t from INR 53,300/t sequentially. Preliminary July data indicates a seasonal dip, but management expects a recovery in pricing from September.

Management commentary, outlook

SAIL’s management has acknowledged the impact of seasonal monsoon-related slowdowns and one-off inventory valuation adjustments on sequential results but emphasised the company’s ongoing operational strength and strong demand outlook. The expansion strategy is on track to raise the company’s crude steel capacity to 35 mnt by 2030, with phased investments and project execution expected to accelerate in the coming years.

Industry implications

SAIL’s robust y-o-y growth and capital discipline in Q1FY’26 reaffirm its position as a leading integrated steel producer in India. With capex execution outpacing targets and demand drivers resilient, the company appears well-placed to deliver its near-term and long-term expansion plans.

Leave a Reply