- Whitehaven posts 60% y-o-y surge in ROM coal output

- Queensland mines drive record growth in production

Whitehaven Coal Limited delivered a robust operational performance in the quarter ending June 2025, successfully meeting or exceeding its guidance across key metrics for FY’25. The company concluded the year with stronger output from both its Queensland and New South Wales assets, improved cost efficiencies, and continued development of strategic growth projects, all the while navigating a softer pricing environment.

The Australian financial year commences in July and concludes in June.

Production, sales close at top end of guidance

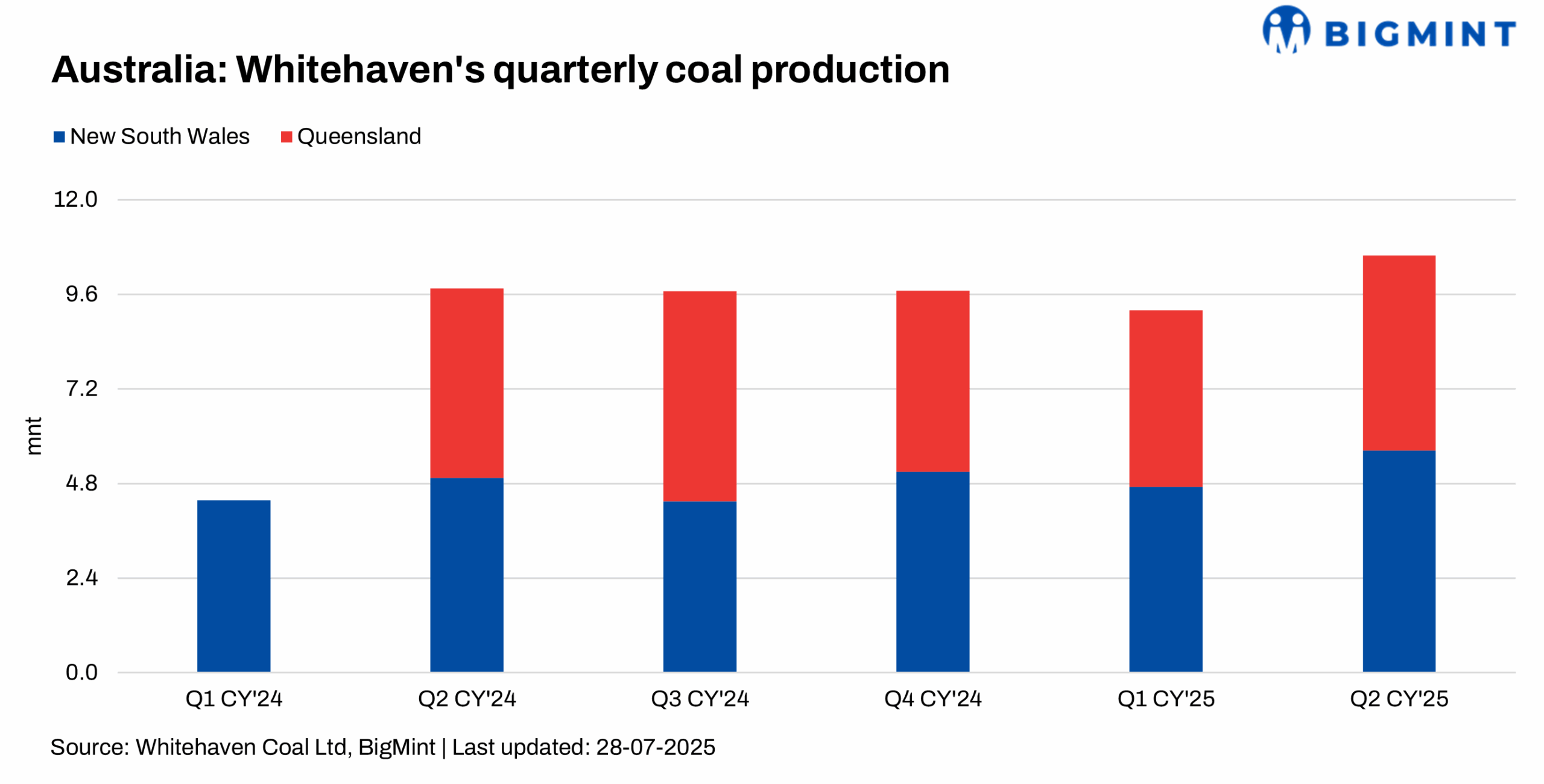

During Q2CY’25 (April-June 2025), Whitehaven achieved managed run-of-mine (ROM) coal production of 10.6 million tonnes (mnt), bringing the full-year total to 39.1 mnt, an impressive 60% increase over FY’24 and at the higher end of the FY’25 production guidance.

This growth was primarily driven by a full year of ownership and operation of the Blackwater and Daunia mines in Queensland. Equity sales of produced coal for FY’25 stood at 26.5 mnt, also at the upper end of the guidance range.

The company’s production efforts were well distributed across its portfolio, with Queensland operations contributing significantly. Queensland ROM production rose 26% to 5.6 mnt in Q2CY’25 from Q1CY’25 (January-March 2025), while New South Wales contributed 4.9 mnt, a 5% q-o-q increase. These figures underscore Whitehaven’s operational resilience and its ability to scale output efficiently.

Queensland operations outperform with record volumes

Queensland emerged as the standout performer in FY’25. The region delivered 20 mnt of ROM coal for the full year, exceeding the upper limit of guidance. This strong showing was supported by a record quarter at Blackwater, which delivered 4.1 mnt of ROM coal, its best result since Whitehaven took ownership. Daunia also posted strong gains, producing 1.5 mnt in the Q2CY’25, up 25% from the previous quarter, and 5.8 mnt for the full year. Sales volumes from Queensland also rose, closing the year at 15.8 mnt.

New South Wales maintains steady performance despite planned shutdowns

New South Wales operations also contributed solidly to Whitehaven’s full-year result. Managed ROM production reached 19.1 mnt for FY’25, in line with guidance and consistent with the previous year. Open-cut operations performed particularly well, with Maules Creek producing 11.5 mnt for the year. The mine saw a notable 31% increase in quarterly production in June, aligned with its mine plan.

Narrabri, however, faced a production dip due to an extended eight-week shutdown for a longwall move. As a result, ROM production fell to 4.3 mnt in FY’25 from 4.8 mnt in FY’24. Nonetheless, coal stock drawdowns allowed sales from Narrabri to remain steady during the period. The Gunnedah Open Cuts, which include Tarrawonga and early-stage mining at Vickery, collectively delivered 3.3 mnt in FY’25, contributing to the region’s overall stability.

Strategic projects advance amid disciplined capital management

Whitehaven maintained a strong focus on capital discipline throughout FY’25. Meanwhile, key development projects moved forward. The Narrabri Stage 3 Project, approved in March 2024, extends mine life to 2044 using existing infrastructure. A revised, lower capex plan is being finalised, with phasing aligned to market conditions and performance. An update will be provided with the FY’25 results in August.

The Winchester South Coal Mine has received draft environmental approval from Queensland’s Department of the Environment, Tourism, Science, and Innovation (DETSI), with federal Environment Protection and Biodiversity Conservation (EPBC) approval underway. Objections have been referred to the Queensland Land Court, where hearings began this week. Whitehaven also continues feasibility studies, exploring synergies with the Daunia mine.

Market conditions present challenges, but long-term outlook remains positive

Whitehaven continues to navigate a softer coal pricing environment, influenced by discounted Chinese steel exports, trade uncertainties, and fluctuating demand.

Despite these near-term headwinds, the company maintains a constructive outlook for the long-term coal market. Structural underinvestment in high-quality metallurgical coal supply, particularly from Australia, alongside growing demand from markets such as India, is expected to underpin future price support. Similarly, the global deficit in high-CV thermal coal supply, exacerbated by mine depletions and lack of new investments, should contribute to more favourable pricing over time.

Looking ahead

With FY’25 completed on a strong note, Whitehaven will release its FY’26 guidance alongside its full-year financial results on 21 August 2025. The company’s focus remains on maintaining operational momentum, executing capital priorities, and navigating market dynamics with strategic agility.

Whitehaven’s performance in FY’25 not only reflects its operational discipline and strategic clarity but also reaffirms its readiness to capitalise on long-term global trends in both metallurgical and thermal coal markets.

Leave a Reply