- India’s ADC12 imports plunge sharp 87% in H1

- BIS-certified ADC12 supply may stabilise Aug prices

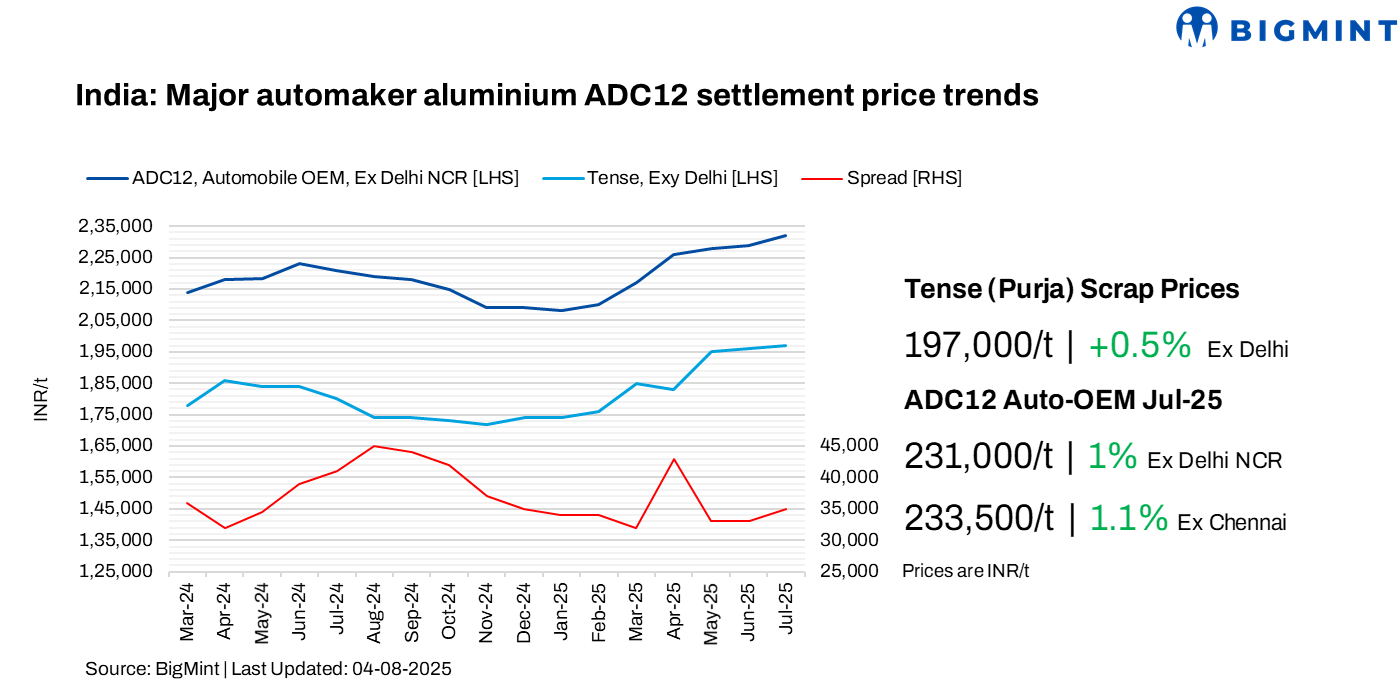

India’s secondary aluminium market witnessed a slight rise in alloy ingot prices through July 2025, supported by strong demand from die-casting and auto component manufacturers, along with elevated input costs.

According to BigMint’s assessments, the average automobile OEM ADC12 prices rose by up to INR 2,500/t m-o-m to INR 231,000/t in Delhi and INR 233,500/t in Chennai. The scrap-to-semi-finished spread held steady in the INR 33,000-34,000/t range, reflecting the consistently high cost of sourcing raw materials.

Additionally, a major Indian automaker has raised its ADC12 settlement prices by INR 850/t m-o-m to INR 229,750/t for August 2025, levels last seen in March 2022. The increase is driven by strong imported aluminium scrap prices and lower aluminium alloy imports. Consequently, the scrap-to-ADC12 spread in July 2025 stands largely stable at INR 32,000-33,000/t due to firm scrap prices.

August offers high, but buyer resistance grows

Despite sellers quoting high ADC12 prices of INR 234,000-235,000/t, OEMs began pushing back. North India-based buyers targeted INR 228,000-230,000/t, while southern buyers negotiated at around INR 232,000-233,000/t.

The scrap-to-ADC12 spread in early August stood steady at INR 33,000-34,000/t due to lower bids from buyers but firm Tense scrap costs in Delhi and Chennai amid shortages.

An alloy producer based in the north observed, “If we look at international scrap prices, ADC12 should be around INR 233,000-234,000/t, but the market is still hovering near INR 230,000/t in the northern region.”

Raw material trends

In July, both imported and domestic aluminium scrap prices rose amid persistent raw material shortages. LME aluminium surged over 4%, crossing $2,600/t, driven by tariff uncertainties and shifting Chinese market dynamics. China’s industry ministry introduced growth-boosting measures for key sectors, supporting industrial metal demand. June aluminium output dropped 3.23% m-o-m but rose 3.4% y-o-y to 3.81 mnt, with H1CY’25 production up 3.3% to 22.38 mnt. Higher LME levels lifted aluminium scrap offer prices.

US-origin Tense rose by $50/t m-o-m to $2,040/t, while UK-origin Wheels increased by $65/t to $2,585/t. Similarly, domestic Tense prices saw an INR 1,000/t m-o-m increase, with BigMint’s July-end assessment at INR 197,000/t in Delhi and INR 200,000/t in Chennai.

Meanwhile, silicon 553 prices from China rose $90/t m-o-m to $1,455/t CFR Mundra amid supply cuts.

Tracking India’s scrap, ingot import flow in H1CY’25

In H1CY’25, India’s aluminium scrap imports increased by 9% y-o-y, reaching 883,960 t up from 809,077 t in H1CY’24. Taint Tabor remained the most imported scrap grade, which saw a gain of 13% y-o-y reaching 201,287 t from 178,282 t. The US continued as the leading supplier, exporting 164,733 t to India reflecting a 14% decrease from H1CY’24 primarily due to the strong domestic demand for scrap in the US.

India’s ADC12 alloy market witnessed a dramatic contraction in imports during the first half of 2025 (H1CY’25), with inbound volumes plunging by 87% y-o-y. Total ADC12 imports stood at just 1,511 t, down sharply from 11,811 t in H1CY’24.

Auto sector performance

India’s vehicle sales declined 5.1% y-o-y to 6.07 million units in Q1 FY’26, driven by weak domestic demand despite gains in UVs and exports. However, auto production rose slightly by 1.6% to 7.27 million units, according to SIAM.

India’s auto exports surged in Q1 FY’26, with passenger vehicle exports hitting a record 204,000 units (up 13.2% y-o-y), driven by stronger demand in the Middle East, Latin America, and parts of Asia. Two-wheeler exports rose 23.2% to 1.14 million units, while three-wheeler and CV exports jumped 34.4% and 23.4%, respectively. However, domestic CV sales dipped 0.6% to 223,000 units.

What lies ahead for August 2025 ?

ADC12 prices are expected to stabilise in August as several Malaysian producers gain BIS certification, improving import availability. Indian inquiries from the UAE have also increased, signalling diversified sourcing. However, prices may hold firm with strong domestic demand ahead of the festival season.

Leave a Reply