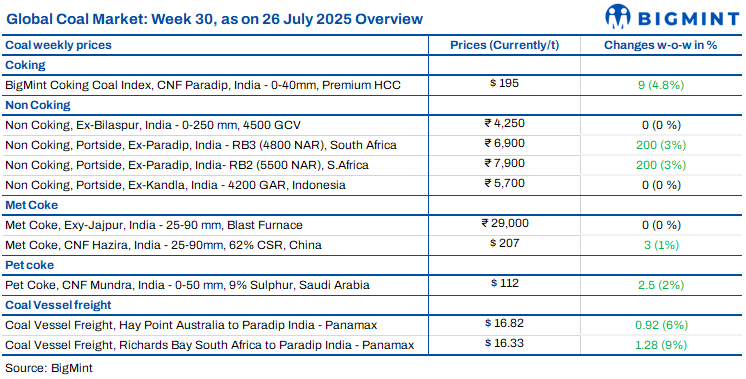

India’s coal market saw divergent movements this week. Domestic 5000 GCV coal prices rose on improved buying by sponge iron producers, while other grades stayed flat amid sluggish demand. South African coal prices inched up on supply issues, but weak portside buying capped gains. Indonesian coal prices held steady, supported by rising freights. Overall sentiment stayed cautious due to monsoon disruptions and limited industrial activity.

Indonesian portside thermal coal prices stable

Indonesian portside coal prices in India stayed largely steady this week. 5000 GAR held at INR 7,150/t at Kandla and INR 7,050/t at Vizag, while 4200 GAR remained at INR 5,700/t and INR 5,600/t, respectively. Only 3400 GAR at Navlakhi saw a minor INR 50/t uptick. Despite weak industrial demand and monsoonal delays, trading sentiment remained firm. Supramax freights rose $1.47/dmt w-o-w to $15.58/dmt due to low water levels in Kalimantan, which affected vessel loading. Power plant stocks dropped to 55.19 mnt, with 13 plants facing critically low coal. Globally, Indonesian coal prices edged up slightly, but cautious buying prevailed. Portside prices may stay stable near term. Demand could improve post-monsoon, but logistics and power sector inefficiencies will limit a sharp rebound.

South African coal offers rise but buyers cautious

South African portside thermal coal offers in India rose again this week, with RB2 (5500 NAR) assessed at INR 7,800/t and RB3 (4800 NAR) at INR 6,800/t exw-Gangavaram – both up INR 150/t w-o-w. The increase stemmed from extended maintenance at RBCT and key rail link outages. However, demand remained tepid as buyers resisted firm offers. Portside stocks rose slightly to 16.13 mnt. Deals were limited, with Paradip and Mangalore seeing RB2 trades at INR 7,800/t and INR 7,850/t, respectively. Meanwhile, sponge iron buying picked up, pushing C-DRI prices ex-Rourkela up INR 1,200/t to INR 26,000/t. Outlook stays firm for prices, though Indian demand may not rebound soon.

Sponge iron demand boosts 5000 GCV coal prices

Domestic 5000 GCV coal prices increased by INR 150/t w-o-w to INR 4,850/t exw-Bilaspur, while 4500 GCV held steady at INR 4,250/t. The rise was supported by a surge in sponge iron demand, with P-DRI prices jumping INR 1,700-1,800/t w-o-w. However, overall coal demand remained weak as SECL’s switch to end-user-only sales curtailed trader participation and kept spot market activity muted.

BigMint’s coking coal index rises on global cues

BigMint’s PHCC index rose by $9/t w-o-w to $195/t CNF Paradip on 25 July, supported by a Panamax booking at similar levels for Aug shipment. Though Indian demand stayed low amid price uncertainty, sellers held back on hopes of further gains. Meanwhile, rising Chinese spot buying and firmer futures added to the positive sentiment.

India’s met coke market firm amid thin imports

India’s met coke market shows stability as import activity stays limited due to pending approval of import quotas under the QR system. Prices stayed flat across Jajpur and Gandhidham at INR 29,000-29,100/t on steady demand and lack of fresh cargoes. Meanwhile, strong pig iron auctions – with SAIL and NMDC reporting gains of INR 250-350/t – reflect healthy downstream sentiment. Global cues were supportive as Australian PHCC edged up $3/t w-o-w and Chinese producers announced a second round of met coke price hikes. Chinese coking coal futures rose sharply, backed by tight supply and active spot trade. Though domestic met coke trade is currently muted, rising pig iron prices and quota clarity could revive import activity and support further price movement.

Imported pet coke offers rise w-o-w amid costlier freight, muted demand

Imported pet coke offers in India increased by $2-3/t w-o-w, largely due to higher freight costs triggered by monsoon-related disruptions. US-origin offers were assessed at $113-115/t CFR, while Saudi-origin stood at $112-114/t. Despite stable fundamentals, demand stayed weak as buyers avoided offers above $116-118/t. The off-season slowdown and freight-led price firmness restricted active trade, with buyers showing resistance to current elevated offer levels.

Dry bulk coal freights rise to 1-year high

Dry bulk coal shipping rates rose w-o-w, nearing a 1-year high as per BigMint’s 24 July 2025 update. Australia-India Panamax freights rose to $16.82/dmt and South Africa-India to $16.33/dmt, mainly due to port delays and weather disruptions. Supramax rates from Indonesia to Navlakhi jumped to $15.58/dmt amid low water levels. Despite weak industrial demand and slow fixtures, the Baltic Dry Index hit 2,120, led by Capesize gains. Meanwhile, DCE coking coal futures surged to a 5-month high of RMB 1,735/t ($242/t), supported by inspection news. Looking ahead, freights are likely to stay firm amid vessel shortages, monsoon-led port issues, and rising activity in South America and grain trades.

Leave a Reply