- Steel production drops 3% in H1CY’25

- Steel exports continue to head north

- Auto sector shines, with production, sales up 12%

Morning Brief: The struggles of China’s steel industry are no secret, and the first half of CY’25 reflects a bleak picture, marked by global and domestic headwinds.

BigMint goes behind the scenes.

Crude steel production declines y-o-y: China recorded a modest 3% drop in crude steel output in H1CY25, widening from the 1.7% dip seen in 5MCY’25 due to a particularly pronounced contraction of 9% y-o-y in June.

Several factors contributed to the decline, with the protracted property crisis being foremost. Flailing under persistent demand weakness, the government also mandated production cuts in March. This move aimed to address aggressive, damaging market competition, which had led to sinking profits and a sustained downtrend in prices.

The impact of these was felt in the moderate y-o-y drops in crude steel output in May-June, which brought down the H1 total.

Parallelly, pig iron production was 0.8% lower y-o-y in January-June.

Steel exports remain relentless: Chinese steel exports spiked by a strong 9.2% y-o-y in H1CY’25, as the uncertainty regarding US import tariffs led traders to front-load shipments. Additionally, soft domestic demand forced producers to ramp up overseas shipments to recoup costs.

Although rising trade protectionism had been expected to moderate export momentum, China found workarounds around these, by shipping products not under the scope of these trade defences. To illustrate, billet exports witnessed a manifold surge due to anti-dumping duties or other safeguards imposed on finished products such as hot-rolled coils (HRCs).

Moreover, Chinese traders also diversified their export destinations.

China’s steel imports fell 16.4% y-o-y in January-June, possibly due to a slump in manufacturing activity.

Iron ore imports falter on trade uncertainties: China’s iron ore imports also dwindled amid trade uncertainties, sparked off by Trump’s tariff war; the continued downturn in steel demand; and strategic sourcing from ample portside inventories.

Weather disruptions also impacted Australian shipments to China, while Indian exporters refrained from shipments due to unviable pricing.

However, imports reached an intra-year high in June, as iron ore prices plunged due to lacklustre demand during the steel off-season and major miners in Australia rushed to meet annual targets.

Coal production climbs up, imports slide: H1CY’25 witnessed a 5.4% y-o-y uptick in the amount of coal churned out by China.

However, demand was weak, as (1) thermal power generation dropped by 4% y-o-y in H1CY’25 and renewables gained ground and (2) steel consumption slowed down, and coking coal inventories remained high.

This led to a supply glut, which resulted in an 11.1% y-o-y drop in coal imports in H1CY’25.

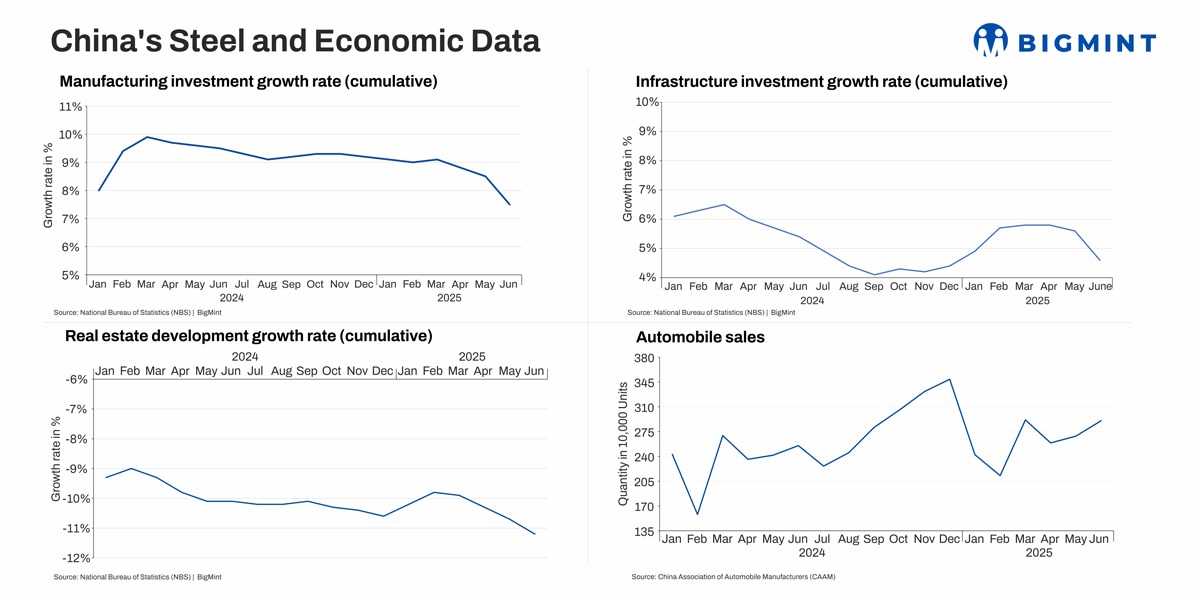

Manufacturing growth shows mixed trends: Data presents a contrasting picture of China’s manufacturing growth. While equipment manufacturing rose 10.2% y-o-y and high-tech manufacturing jumped 9.5% in this year’s first half, the manufacturing investment growth rate receded to 8.7% against 9.4% in the year-ago period.

The automotive segment remained a bright spot. Production was higher by a robust 12.5% y-o-y to 15.6 million units, while sales increased 11.5% and exports were up by 10.4% y-o-y. New energy vehicles (NEVs) led the climb, as both production and sales registered growth of over 40% y-o-y, while exports shot up by 75%.

However, the sector has been beset by aggressive price wars and financial stress due to overcapacity.

The official manufacturing purchasing managers’ index (PMI) also remained in contraction territory in the last three months of H1CY’25, amid trade war-related uncertainties, slack domestic demand, limited consumer expenditure, and deflationary trends.

Growth stunted in realty, infra segments: Both the real estate and infrastructure segments witnessed poor growth in H1CY’25. The infrastructure investment growth rate fell to 5.4% from 6% in the first half of the previous year, while property investment declined 11.2% y-o-y. Meanwhile, the decline in the real estate development growth rate deepened to 10.4% compared to 9.6% previously.

Property sales by floor area dropped 3.5% y-o-y in January-June, and new construction starts slumped by 20% y-o-y, though the latter saw slight m-o-m improvements in May and June. The housing area sold slipped by 8%, while the government’s revenue from land sales fell 6.5%, indicating lower inclination among developers to procure land.

In tandem, cement production, a key indicator for construction activity, fell 4.3% y-o-y in H1CY’25, suggesting a stagnation in construction activity.

Outlook

Recently, Beijing has advocated for an anti-involution movement, attempting to crack down on excessive competition and rampant price undercutting. This, coupled with efforts to rein in overproduction, shows that the government is determined to bring about a phase of strategic discipline in the Chinese steel industry.

As such, steel production is expected to dive further in H2. However, while this move was warranted, given that steel consumption is expected to decline in CY’25, it is uncertain whether a large-scale improvement will be possible without hefty financial stimulus or infrastructure projects from the government.

The commencement of construction on the world’s biggest hydropower dam in Tibet has certainly caused a market rally, and participants expect the move to boost iron ore imports and coal consumption. However, caution persists regarding the sustainability of this uptrend. More such infrastructure projects may help relieve the downward pressure on the industry.

China’s steel exports may also taper off if domestic demand provides adequate support or if traders are no longer able to evade safeguards. Concurrently, amid rising inventories and falling margins, auto production seems to have slowed down in H1CY’25 compared to 5MCY’25, and there is a strong chance that this deceleration will continue.

Leave a Reply