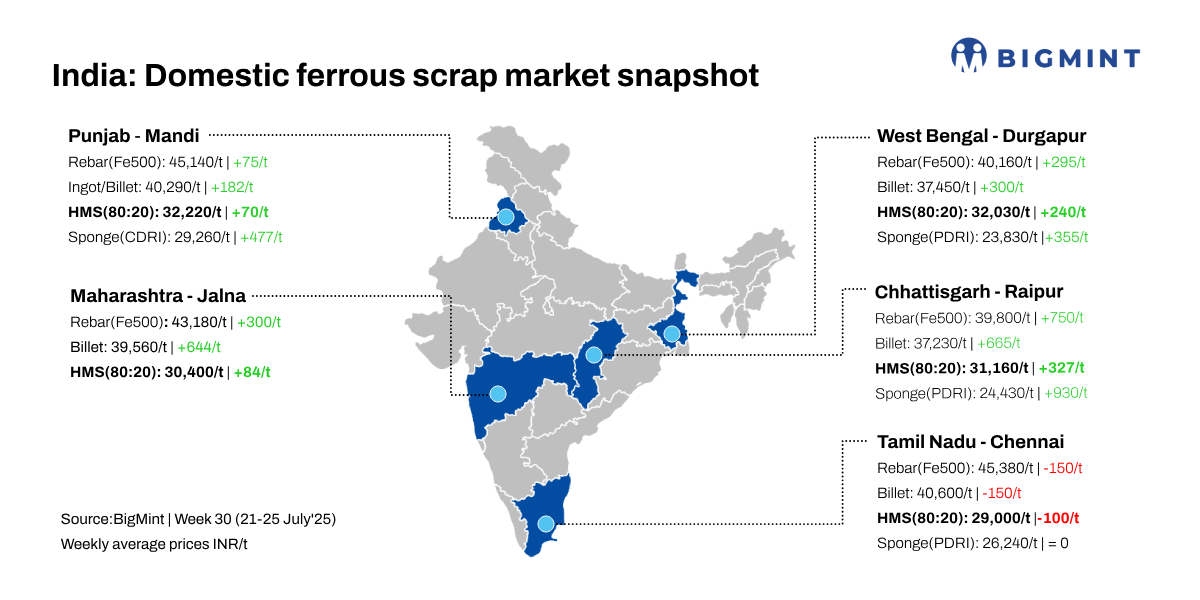

- Scrap demand picks up mid-week

- Finished steel offtake remains slow

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, increased by INR 400/tonne (t) d-o-d to INR 35,900/t DAP on 25 July 2025.

Scrap prices in the Mandi region saw a sharp rise of INR 400-500/t d-o-d, with a marginal w-o-w gain of INR 100-200/t. The market witnessed moderate demand this week, picking up slightly over the last three working days. However, finished steel demand remained sluggish, with mills waiting for a stronger market push. Meanwhile, sponge iron prices continued their upward trajectory, adding to production costs for steelmakers.

Imported scrap buying gained momentum at the Indian west coast, with fresh deals concluded amid steady demand from secondary steel producers.

1,000 t of UK-origin HMS (80:20) were booked at $330/t CFR. Additionally, 500 t of HMS (90:10) from New Zealand were bought at $345/t CFR West Coast.

A mill owner informed BigMint, “Ingot prices in Mandi are expected to stay range-bound between INR 40,400-41,000/t in the coming week. Despite a slight price uptick this week, steelmakers remain cautious, citing weak finished steel demand and low trading volumes.”

Another mill owner stated, “After hitting a four-year low, scrap and semi-finished steel prices showed signs of recovery this week. Rising raw material costs supported a price uptick in both semi-finished and finished steel products. The threat of billet imports from nearby states to Mandi has also eased.”

Raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh surged by INR 400/t d-o-d to INR 29,800/t DAP. On a w-o-w basis, prices rose by INR 480/t, supported by steady demand.

In Ludhiana, steel-grade pig iron prices rose by INR 300/t d-o-d to INR 35,800/t DAP. W-o-w gains stood at INR 155/t, reflecting mild market improvement.

Steel market trends

In the Mandi Gobindgarh market, semi-finished steel prices jumped by INR 350/t d-o-d to close at INR 40,800/t DAP, with a w-o-w rise of INR 180/t. Across major hubs, steel ingot prices surged by INR 300-700/t d-o-d, with Ahmedabad recording the most significant increase, reflecting strengthened market sentiment.

Rebar (Fe 500) prices in Mandi Gobindgarh rose by INR 300/t today to INR 45,500/t ex-works. While w-o-w prices remained mostly stable, market activity showed improvement over the past few days compared to the previous week, indicating a cautiously optimistic buying trend in the region.

Overview of Mumbai market

Rebar (Fe 500, IF route) prices in Mumbai rose by INR 200/t d-o-d to INR 43,700/t exw, driven by firmer finished steel and raw material prices. Buying interest remained moderate. HMS 80:20 held steady at INR 30,700/t DAP. The scrap-to-billet conversion spread stood at INR 9,700/t, supporting healthy margins for secondary mills and boosting market sentiment.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $330-332/t, which equates to approximately INR 30,915/t (including freight). HMS (80:20) prices in Mumbai remained stable at INR 30,700/t DAP today. Indicative prices of shredded from Europe stood at $360/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,700/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply