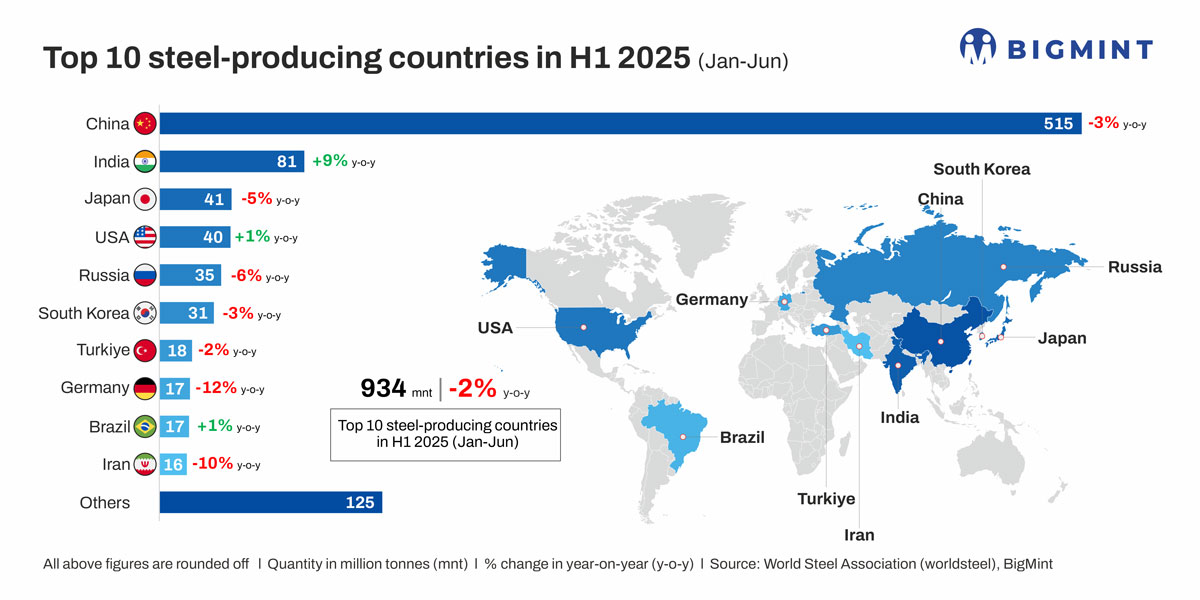

- Chinese crude steel production down 3% y-o-y to around 515 mnt

- India posts strong 9% growth in production in H1CY’25

- Advanced economies continue to battle stagnant demand, inflation

Morning Brief: Global crude steel production in the first half of the current year (January-June 2025 or H1CY’25) reached 934 million tonnes (mnt), a decrease of 2% compared with H1CY’24, as per data recently released by the World Steel Association (WSA). WSA’s data represent around 98% of global steel production, covering as many as 70 countries that report directly to it.

BigMint had reported a marginal 0.4% y-o-y decline in January-April of the current year. But crude steel production showed a steeper decline in May-June, especially June. This was largely due to the sharp 9.2% y-o-y downturn in China’s crude steel output in June. China has an outsized influence on global steel production, with a share of roughly 55% of the world total.

The downtrend in steel production worldwide could be directly traced to China entering a phase of gradual but irreversible decline in steel demand, with key steel-consuming sectors in that country showing persistent weakness.

Moreover, tariffs and trade tensions, high inflation and energy prices, and weak export prospects all contributed in equal measure to keeping global steel sector sentiments subdued in H1CY’25.

How did top steel-producing countries fare in H1CY’25?

China’s crude steel output reached 515 mnt in H1CY’25, a decrease of 3% y-o-y. As per most predictions, steel consumption in China is set for a marginal decline in CY’25 as the downtrend in the property sector and partial slowdown in infra and construction is unlikely to be wholly compensated by the growth in steel demand from the engineering goods, shipbuilding, appliances and NEV sectors.

The country’s crude steel production dropped over 9% y-o-y in June to a little over 83 mnt – the steepest decline witnessed thus far in CY’25. This was due primarily to weaker steel prices during the summer months, not to mention low end-user demand in the critical property and construction sectors.

Many mills chose to take maintenance downtimes in June due to receding margins during summer, while steel exports were also comparatively lower than the previous months.

India’s output of steel recorded a 9.2% increase y-o-y in January-June of this year, as per WSA. India happens to be the only glittering spot on an otherwise sombre global steel map due to a) unprecedented growth in infra and construction, thanks to the government’s national infrastructure pipeline, PMAY, etc.

b) rapid urbanisation and surge in auto demand, as well as general engineering, consumer appliances, Railways and Defence; and

c) rapid capacity expansion undertaken by the primary producers.

It deserves mention that India’s steel production had edged up 7% y-o-y in 4MCY’25, but showed higher growth in H1CY’25 following the imposition of a 12% safeguard duty on steel imports in mid-April, which naturally boosted the integrated mills that were in desperate need of some sort of protection through an import barrier, particularly due to very soft steel demand globally.

Japan, the third-largest global steel producer, witnessed a 5% decline in production due to demand for steel declining both domestically and internationally, with the pace of production slowing down for both the blast furnace manufacturers and electric furnace producers, according to the Japan Iron and Steel Federation (JISF).

The softening of Asian markets due to increased steel exports from China hit the Japanese steel industry as export demand dampened, thereby impacting manufacturers.

Similarly, South Korean crude steel production fell by over 3% y-o-y to 31 mnt in H1CY’25. The major reasons were domestic demand slump, typical to matured economies, diminishing cost-competitiveness of key steel producers such as POSCO, downtrend in the export market amid US tariffs and soft global demand, as well as a high level of steel exports from China.

The US recorded total production at 40 mnt in H1CY’25, up 1% y-o-y as the import tariff on steel boosted the domestic industry, and also due to the fact that market sentiments were upbeat following major acquisitions and strategic investments by key producers. The domestic steel industry is seeking to derive incentives from the IRA and other enabling policies.

However, analysts predict that US trade policies and tariff-related uncertainties are expected to affect downstream demand, with gradually mounting inflationary pressure.

Russia’s crude steel production decreased by 6% y-o-y to 35 mnt due to falling global steel prices and the decline in steel exports alongside an appreciating currency, drop in demand from domestic construction and energy sectors, and the weight of sanctions on the economy and industry.

Trade uncertainties, cost pressure due to the hike in energy prices, and competition from China amid the surge in exports of billet were the major factors impacting Turkish steel production which fell by 2% on the year to 18 mnt during the review period.

Likewise, continued downturn in the manufacturing sector in the EU, high energy prices due to the Russia-Ukraine war, and the ever-present threat of increasing steel imports, despite safeguards, affected steel production in the continent, and especially in Germany which continues to battle the costs of energy transition, while seeking to stay afloat.

Outlook

The global steel scenario is unlikely to change much in H2CY’25. However, US trade pacts (aimed at moderating the tariff burden) with major partners such as Japan, and possibly India in August will go some way in reviving sentiments in major steel-producing geographies. While India’s inherent strength will drive its steel industry, the EU may witness a marginal recovery in H2 as import volumes shrink and the auto sector gains some kind of a momentum.

But, in the last instance, everything hinges on China: if Chinese steel production in CY’25 edges down by, say, 4-5% y-o-y in H2 (considering the possibility of greater reductions in the latter half of the year due to winter environmental restrictions and government mandates to lower production in certain regions and provinces) there is every likelihood of curtailed steel exports from China amid ever-increasing global trade restrictions. However, whether that is likely to happen is anybody’s guess.

Leave a Reply