- Charterers turn cautious as freights rise

- Baltic dry bulk index touches 1-year high

Dry bulk coal freights to India recorded a notable increase this week, with rates on key routes reaching a one-year high. Panamax rates firmed up w-o-w on the Australia-India and South Africa-India lanes, while Supramax ones on the Indonesia-India corridor edged higher.

However, rising freights, coupled with ongoing rainfall across parts of India, dampened thermal coal demand, slowing vessel booking activity. Most market participants remained on the sidelines, anticipating a correction in offers or a decline in port inventories before initiating fresh restocking.

India’s portside thermal coal inventories remained largely unchanged at 15.60 million tonnes (mnt) during week 29 of 2025, as minor variations in port-wise arrivals and offtake kept overall stocks stable.

Sources noted that charterers maintained a cautious stance amid elevated freights in the Pacific basin for Panamax and Supramax vessels. Despite a tight balance between tonnage availability and cargo demand — with prompt cargoes still fetching a premium — expectations for further upside in the basin remained limited. “There is a noticeable gap between high vessel time charter rates and the lower freights being quoted by charterers,” a source informed BigMint.

Meanwhile, freight derivatives (FFAs) edged lower during Asian trading hours, while bunker fuel prices remained flat on a weekly basis, prompting concerns among market participants.

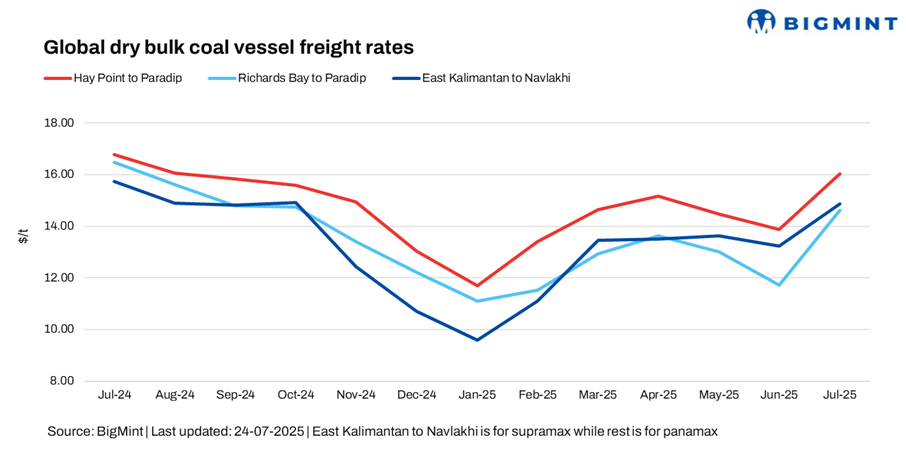

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India increased by $0.92/dry metric tonne (dmt) w-o-w, with BigMint’s latest assessment placing the Hay Point-Paradip route at $16.82/dmt. Monsoon rains continued to impact several regions of India, disrupting port operations, delaying cargo handling, and tightening vessel turnaround times. The weather-related interruptions led to congestion at select ports, limited loading/discharging windows, and contributed to higher freights — particularly for coastal movements. Indian buyers, especially blast furnace operators, remained cautious, and some fixtures faced rescheduling or delays due to reduced operational efficiency at terminals.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay)–India (Paradip) route rose by $1.28/dmt w-o-w to $16.33/dmt, despite subdued market activity. The increase was largely driven by logistical constraints and the ongoing 20-25 day maintenance at the Richards Bay Coal Terminal (RBCT), which has limited vessel loadings and tightened supply.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan)–India (Navlakhi) route rose by $1.47/dmt w-o-w, reaching $15.58/dmt. The uptick was attributed to logistical challenges faced by miners in Kalimantan, stemming from declining water levels that impacted vessel movement, according to sources.

Meanwhile, in India, weak industrial demand, balanced stock levels, and monsoon-related logistical disruptions kept coal market activity muted, with prices holding firm amid limited trading.

Market highlights

- Baltic dry bulk index hits over 1-year peak: The Baltic Exchange’s dry bulk index, the main sea freight metric, climbed up to its highest level in over a year on 24 July 2025, buoyed by a sharp rise in Capesize rates. The composite index, which reflects freights across Capesize, Panamax, and Supramax segments, advanced 85 points to 2,120 – marking its strongest performance since July 2024. Capesize vessels led the uptrend, with the corresponding index surging 278 points to 3,339. On the other hand, the Panamax index saw a marginal decline of 4 points to 1,905. The Supramax index also eased, falling 16 points to 1,313.

- DCE coking coal futures hit 5-month high: Coking coal futures on the Dalian Commodity Exchange (DCE) rose by RMB 33.5/t ($5/t) d-o-d to RMB 1,735/t ($242/t) on 24 July 2025, marking a five-month high. The sustained price rally followed confirmation by state media regarding the authenticity of government documents ordering inspections across eight key coal production hubs in China. Market reports indicated that the surge was driven by speculation surrounding these inspections, based on a document allegedly issued by the National Energy Administration (NEA), though its authenticity remains unverified.

Outlook

In the near term, dry bulk coal freights are expected to remain firm to slightly bullish, supported by tighter vessel availability due to increased activity from regions such as the East Coast of South America (ECSA) and vessel reallocation towards seasonal grain shipments.

Although demand from core sectors such as cement and power remains muted amid the ongoing monsoon, steady portside inventories and weather-related delays are likely to constrain vessel supply. As a result, Panamax rates on routes such as Australia-India and South Africa-India could see moderate upward movement, while Supramax rates on the Indonesia-India corridor are projected to hold steady or edge higher.

Leave a Reply