- Weather disruptions hamper Australian export operations

- Canadian exports rise amid Glencore’s strategic acquisition

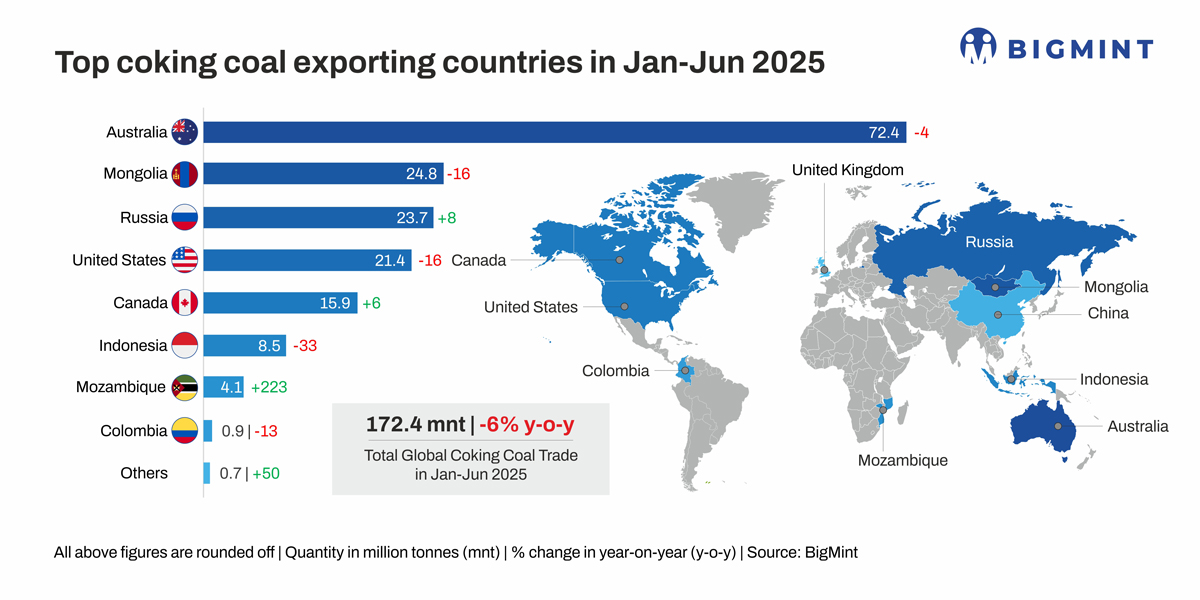

Global coking coal trade volumes declined by 6% to 172.4 million tonnes (mnt) in the first half of CY’25 against 182.6 mnt in H1CY’24, as per provisional data maintained with BigMint. This drop was driven by a combination of softer steel production, growing domestic coal availability, and shifting trade flows.

Major importers such as China and India curtailed seaborne purchases, influenced by weak downstream steel demand, higher domestic or overland coal supply, and changing trade policies, including tariffs and import controls.

According to the World Steel Association (WSA), global crude steel output fell 2.2% y-o-y to 934 million tonnes (mnt) in H1CY’25. Economic slowdowns, particularly in advanced Asian economies, coupled with subdued construction activity in China and persistent inflationary pressures in Europe, collectively weighed on steel production and, consequently, coking coal demand.

Australia’s exports contract due to lower demand, weather disruptions

Australia, the world’s largest exporter of coking coal, saw a 4% y-o-y drop in shipments to 72.4 mnt during H1CY’25. Key buyers such as India and Japan cut their purchases by 14% each, amid weaker steel demand and import diversification. Additionally, adverse weather conditions, including heavy rainfall in North Queensland, significantly disrupted coal logistics, with exports from major Queensland ports plunging 35% y-o-y in February.

India diversifies import sources, coal blends

Although India’s total imports remained stable y-o-y at 30.86 mnt in H1CY’25, shipments from Australia dropped sharply, by 14% to 15.3 mnt, as steelmakers continued to diversify their coking coal sources following the price volatility of recent years.

Imports from Russia surged 51% to 5.3 mnt due to competitive pricing amid sanctions, leading to reduced reliance on Australian premium hard coking coal (PHCC). Indian mills also intensified efforts to explore alternative blends of semi-hard and mid- to low-volatile coal to optimise blast furnace performance and reduce costs. Several mills have also invested in overseas coal assets to ensure supply security in a volatile market.

Japan’s steel sector faces demand headwinds

Japan’s total coking coal imports fell 14.4% y-o-y to 22 mnt in H1CY’25 from 25.7 mnt. Notably, Japan’s crude steel production declined by 5% y-o-y in H1CY’25, reflecting tepid domestic and export demand. Additionally, concerns over US tariff policies further dampened confidence in Japan’s export-reliant steel industry, contributing to reduced coking coal demand.

China prioritises domestic supply, overland imports

China’s coking coal imports fell 8% y-o-y to 52.83 mnt in H1CY’25, as higher domestic output reduced reliance on seaborne supplies. Raw coal production grew 5.4% y-o-y to 2.4 billion tonnes, while coke production rose 3% to 249.41 mnt during the same period.

China also reduced its imports from Mongolia and Russia, by 16% and 2% to 24.8 mnt and 14.8 mnt, respectively.

Russia expands presence in Asian markets

Russia boosted its coking coal exports by 10% y-o-y to 23.7 mnt in H1CY’25, mainly due to increased shipments to India. India and China together accounted for 92% of Russia’s met coal exports in CY’24. Enhanced eastern logistics infrastructure is helping to counterbalance mine closures and elevated transport costs, enabling Russian coal to remain competitive in Asian markets.

US exports decline amid tariff barriers and cost challenges

US coking coal exports dropped 16% y-o-y in H1CY’25, largely due to reduced shipments to China following the announcement of a 15% import tariff. Although the US is trying to redirect supply toward developing Asian economies, high mining costs and surging freights pose significant hurdles. Broader macroeconomic concerns and geopolitical uncertainty also weighed on demand for US coal.

Canadian shipments increase on strategic expansion

In contrast to global trends, Canadian coking coal exports rose 6% y-o-y to 15.9 mnt in H1CY’25. The sector received a boost following Glencore’s acquisition of Elk Valley Resources, a move expected to support higher future exports through increased production and efficiency.

Outlook

Global coking coal trade is expected to remain subdued in the near term amid continued weakness in steel production and cautious buyer sentiment. However, potential recovery in industrial activity and infrastructure investments across emerging Asian economies could offer limited upside.

Australia may continue to face export headwinds due to declining demand from traditional buyers and climate-related disruptions. Conversely, Russia and Mongolia are likely to strengthen their positions as key suppliers to Asia, while India and China pursue long-term diversification strategies. In this context, trade flows are expected to remain fluid, with volatility persisting unless global steel fundamentals show sustained improvement.

Listen to industry experts and gain insights on “Coking Coal & Met Coke: Demand Shifts and Import Challenges in a Transitioning Steel Industry” at the BigMint India Ferrous Week, to be held over 19-21 August 2025 at JW Marriott, Kolkata.

Leave a Reply