- Buyers favour domestic scrap over imports

- Ample supply limits further gains for dross

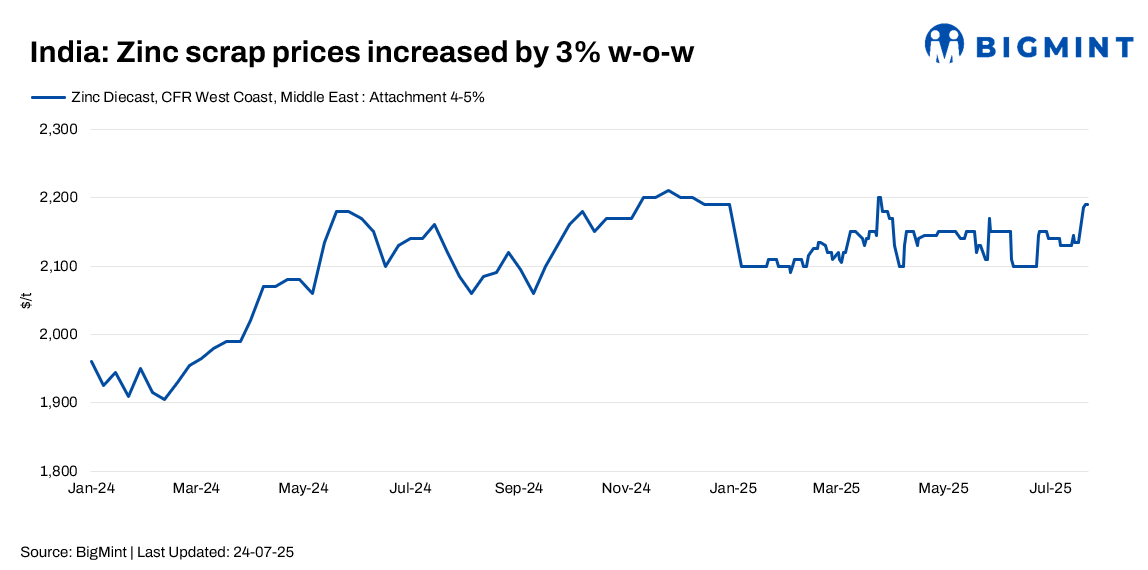

India’s zinc scrap and dross prices recorded a slight w-o-w increase, tracking gains in global zinc benchmarks and steady domestic demand. BigMint assessed zinc diecast scrap (Middle East origin) at $2,190/tonne (t) CFR west coast India, up $55/t w-o-w.

At the time of reporting, London Metal Exchange (LME) zinc prices stood at $2,871/t, up $161/t from last week’s $2,710/t.

Zinc dross was assessed at INR 223,000/t ex-Delhi, up by INR 3,000/t w-o-w, as per a buyer who indicated that supply availability was adequate, which helped cap further upside.

Market highlights

Demand from zinc oxide manufacturers and secondary smelters showed marginal improvement this week. However, price gains remained limited due to stable dross supply and cautious downstream procurement.

Zinc oxide (99% Zn) continued to be assessed at INR 214,000-215,000/t ex-Delhi, with offers unchanged w-o-w.

According to one importer, more market participants are shifting towards domestic sourcing for zinc scrap, citing better prices compared to imported lots.

In north India, big-sized zinc scrap (Tukdi, 97% Zn) was offered at INR 222,000/t ex-Delhi, rising by INR 5,000/t w-o-w. Meanwhile, mid-sized Tukdi (97-98% Zn) remained largely stable, with buying interest heard in the INR 198,000-202,000/t range.

Tightness in both domestic and international zinc scrap availability continues. Buyers noted a widening gap between offers and bids, with limited willingness to take fresh positions at higher prices.

Outlook

Zinc scrap prices are expected to stay firm to slightly bullish in the near term, supported by recent LME gains and ongoing scrap supply constraints. However, cautious buyer sentiment and fluctuating offer-bid spreads may limit aggressive upside. Domestic sourcing is likely to remain active, especially as import economics remain less favourable.

Leave a Reply