- Shipowners’ firm stance pushes rates higher

- Baltic Capesize index leads the surge

Dry bulk iron ore freight rates continued their upward trend, supported by sustained bullish sentiment in the market. Vessel hiring activity remained broadly steady compared to the previous week, while freight rates on key routes – including India-China, Australia-China, Brazil-China, and South Africa-China – posted w-o-w gains. Notably, freight rates on the India-China route surged to their highest level in over six and a half months, data maintained with BigMint shows.

The Capesize market witnessed a strong and sustained rally this week, supported by firm sentiment and positive momentum across both the Pacific and Atlantic basins. The upward movement was fueled by solid demand from major miners, increased operator activity, and a gradually tightening tonnage list, as several vessels were diverted to handle agricultural cargoes. Market participants also pointed to a rise in enquiries from miners and traders, along with higher rate indications from shipowners, all contributing to the continued upward pressure on freight rates across key export regions.

“Market sentiment remains strong, with vessel time charter (TC) rates continuing to outpace the freight levels being offered by charterers”, mentioned a source to BigMint.

Another source told BigMint, “Although compared to last week, the market has softened slightly and is currently flat, with limited movement at the higher levels. However, a number of iron ore cargoes are emerging from the East Coast of India, driven by the recent uptick in iron ore prices.”

However, owners are holding out for higher daily time charter (TC) rates to charter out their vessels, while charterers continue to offer lower freight rates. At the same time, the Forward Freight Agreement (FFA) market witnessed a notable decline this week, which is expected to exert additional pressure on freight rates in the near term.

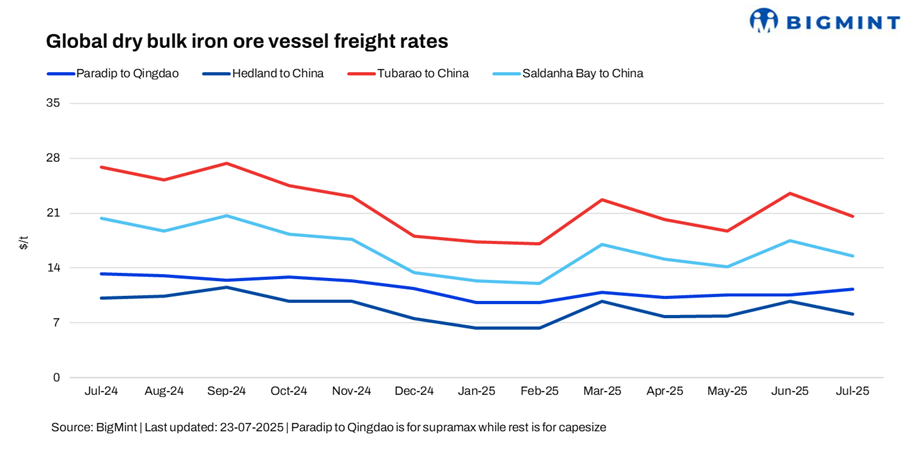

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freight rates for Supramax vessels from the Indian Ocean to China rose to $12.18/dry metric tonne (DMT), up by $0.48/DMT w-o-w. The rise was further supported by positive sentiment in the Indian low-grade iron ore export market, coupled with a w-o-w increase in global iron ore prices and gains in DCE iron ore futures during the week.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freight rates for iron ore shipments from Western Australia to China rose to $9.55/DMT, marking a w-o-w increase of $1.15/DMT. The uptick was fueled by active chartering from major Australian miners, including Rio Tinto and BHP, who booked vessels for Qingdao with laycans scheduled from early to mid-August 2025. This surge in activity notably tightened available tonnage, according to sources quoted by BigMint.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freight rates for Brazil-to-China shipments rose significantly by $2.25/DMT w-o-w, settling at $23.15/DMT. Around two fixtures were reported on the Tubarao-Qingdao route, concluded at rates ranging from $22-22.98/DMT for mid to late August 2025 laycans.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freight rates from Saldanha Bay to Qingdao also increased by $1.95/DMT w-o-w, settling at $17.45/DMT. The rise was attributed to persistent logistical issues at South African ports, which have disrupted operations and led to reduced vessel availability.

Market highlights:

- Baltic index extends gains amid strength across vessel segments: The Baltic Exchange’s main sea freight index maintained its strong momentum, driven by broad-based gains across most vessel segments. On 22 July 2025, the Baltic Dry Index – which tracks freight rates for Capesize, Panamax, and Supramax vessels – rose by 19 points to reach 2,035. The Capesize segment led the rally with a sharp 80 point increase to 3,061. In contrast, the Supramax index declined by 17 points, settling at 1,329.

- China’s iron ore spot prices remain firm w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $105/tonne (t) CFR China on 22 July 2025, up by $7/t w-o-w. Optimism around the future market outlook remained firm. However, reports indicated that physical trading activity lagged behind the more active paper market, resulting in slimmer margins for traders. Meanwhile, China’s portside prices for iron ore saw a notable increase, accompanied by gains in coking coal and coke prices.

- DCE iron ore futures climb up w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract improved by RMB 41.5/t ($6/t) w-o-w to RMB 814.5/t ($113/t) on 23 July.

Outlook

The near-term outlook for dry bulk iron ore vessel freight remains firm to slightly bullish, supported by strong iron ore prices, active chartering by major miners, and tightening vessel supply. Increased exports from Australia, Brazil, and India – driven by rising iron ore demand – are boosting Capesize activity, especially for early to mid-August laycans. Ongoing port disruptions in South Africa and monsoon delays in Asia are further constraining tonnage availability.

While physical freight markets remain steady, the Forward Freight Agreement (FFA) market has seen some softening, reflecting cautious sentiment. Nonetheless, with sustained miner demand, tightening supply, and strong pacific and atlantic movement, Capesize rates are expected to remain elevated in the near term, while Supramax may stay relatively stable.

Leave a Reply