- Logistics disruptions occur, trade stays weak

- Chinese, Indonesian NPI prices remain stable

India’s stainless steel market witnessed bearish activity this week, with finished flats showing mixed price movements and longs witnessing a slight decline w-o-w, amid limited trading activity.

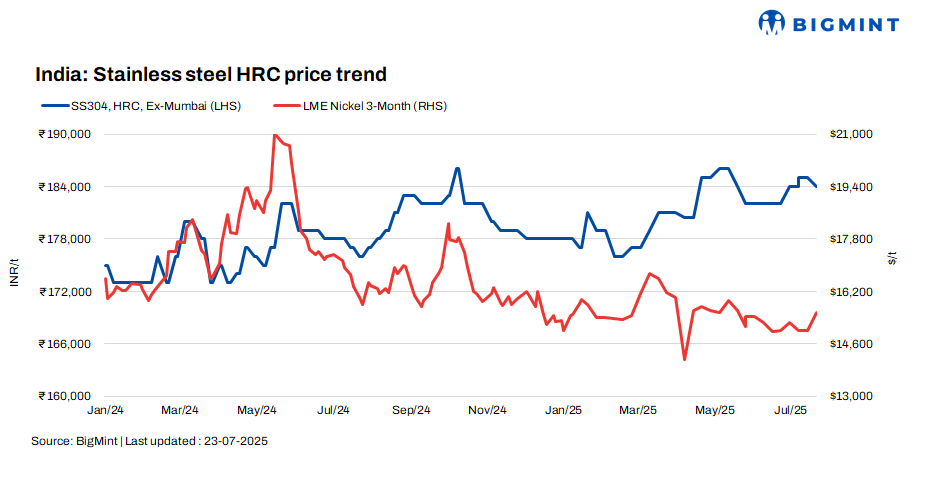

BigMint’s benchmark assessment for 304 series hot-rolled coils (HRCs) dropped marginally by INR 1,000/t w-o-w to INR 184,000/t ex-Mumbai. Meanwhile, 304L black round bars (25-100 mm) dipped to INR 156,000/t w-o-w, reflecting cautious buyer sentiment and thin transactional volumes.

BigMint’s assessment for SS 316 HRCs stood at INR 330,000/t, down by INR 1,000/t w-o-w, and for 316 cold-rolled coils (CRCs) at INR 334,000/t ex-Mumbai, steady w-o-w.

Market updates

Finished flats prices recorded fluctuations. As per a source, “Despite a recent uptrend in Chinese stainless steel flat prices, demand in India stayed moderate, as buyers remained cautious due to ongoing BIS certification.”

The longs market remained largely range-bound, as western regions faced persistent rainfall, which disrupted logistical operations and daily market routines, dampening trade momentum. Market participants highlighted subdued buying interest, as adverse weather conditions led to delays in movement and dispatch.

LME nickel rise, Asian NPI flat w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,560/t, up by 3% w-o-w. Nickel stocks in LME-registered warehouses stood at 206,580 t, up by 3,960 t compared to 202,620 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) remained firm w-o-w at RMB 917/t ($128/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $109/t, steady w-o-w.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,450/t ($1,873/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were firm at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices climbed up by INR 50,000/t ($579/t) compared to the last assessment on 16 July 2025. The uptick was largely due to constrained supply and higher oxide prices.

Ferro molybdenum prices rose to INR 2,900,000/t ($33,561/t) exw-India, as per BigMint’s assessment on 22 July. Deals for around 28 t were concluded last week, within the price range of INR 2,780,000-2,920,000/t ($32,172-33,793/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 99,500/t ($1,158/t) exw-Jajpur, range-bound w-o-w.

Vedanta-Ferro Alloys Corporation (FACOR) will conduct an auction for high-carbon ferro chrome (10-150 mm) on 23 Jul’25. The minimum allowed bid quantity for all lots is 25-300 t. At the previous auction on 2 July, the larger lot of 10-150 mm fetched an H1 price of INR 99,200/t ($1,150/t) exw. BigMint assessed ferro chrome (HC 60%, Si: 4%,10-150 mm) prices at INR 99,600/t ($1,156/t) exw-Jajpur on 18 July.

Ferro silicon: Indian ferro silicon (70%) prices inched down by INR 1,100/t ($13/t) in comparison with the last assessment on 14 July 2025. Despite firm offers from sellers, the market lacked momentum due to muted buyer interest

Ferro silicon prices were at INR 85,700/t ($992/t) exw-Guwahati, as per BigMint’s assessment on 21 July. In Bhutan, prices moved down by INR 700/t ($8/t) w-o-w to INR 86,300/t ($1,000/t) exw.

Ferrous scrap: India’s imported scrap market remained sluggish this week, weighed down by muted steel demand, monsoon-related logistical hurdles, and buyer hesitation. Mills largely refrained from fresh bookings, preferring cost-effective domestic scrap and sponge iron, which saw significantly higher intake. Shredded offers from the UK/EU and Australia hovered at $365-370/t CFR, but bids remained firm below $355-360/t, limiting trades. HMS 80:20 offers stood at $330-335/t CFR, though buyer interest was weak. Overall, limited deals were observed, as sellers struggled to secure workable prices. Without a major supply crunch or steel market rebound, import appetite is likely to stay subdued in the near term.

Outlook

The stainless steel market is expected to remain muted till July-end, with demand likely to rise from August as mills begin booking ahead of the upcoming festive season.

Leave a Reply